The oil and gas industry continues to operate within a complex macroeconomic environment characterised by geopolitical uncertainties, evolving supply-demand dynamics, and shifting policy landscapes. Understanding the macroeconomic factors affecting oil and gas industry performance has become increasingly key for investors, traders, and industry stakeholders navigating the volatile energy markets of 2025. In this article, we’ll break down macroeconomic factors affecting the oil and gas industry, with insights taking from our Trading Co-Pilot.

Geopolitical tensions: The persistent price driver

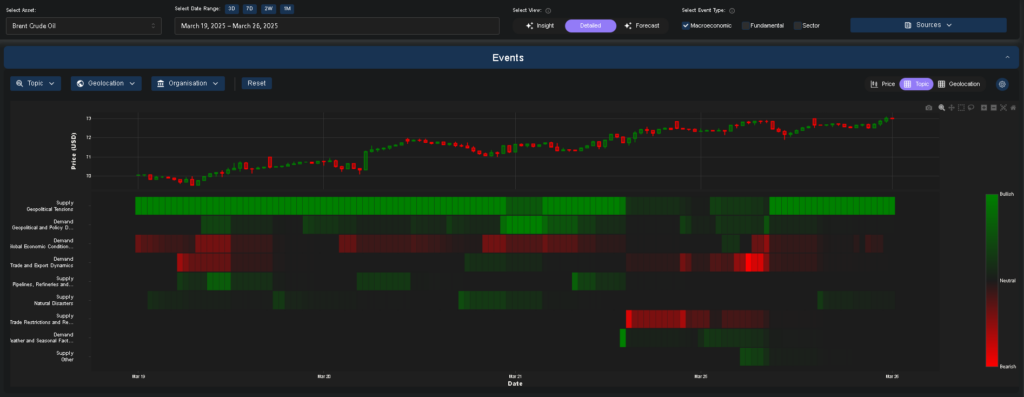

The vast majority of recent price movements in oil and gas markets can be traced to geopolitical developments. As our Trading Co-Pilot data indicates, oil prices climbed to a three-week high in late March 2025, driven by escalating tensions in multiple regions. Military operations in Gaza and Ukraine have created persistent supply concerns, while diplomatic developments such as the Russia-Ukraine ceasefire agreement regarding Black Sea navigation have introduced moments of market stabilisation.

Perhaps the key is understanding how these geopolitical events create cascading effects across the energy ecosystem. For example, on March 21, natural gas prices peaked at 44.31 but dropped retreated to 42.62, influenced by military actions in Ukraine, including a strike on the Sudzha gas metering station, which significantly impacted supply dynamics. This is a recognition that energy markets remain highly sensitive to geopolitical developments, particularly in key production and transit regions, and this is entirely correct.

Trade policies and tariffs: A new macroeconomic factor

It is an irrefutable fact that trade policies have emerged as a significant macroeconomic factor affecting oil and gas industry performance. Recently, Trump’s announcement of a 25% tariff on countries purchasing oil from Venezuela introduced significant volatility in late March.

At this point, it’s worth noting that tariffs represent a relatively new macroeconomic force in energy markets (at least, that is, in their current iteration in recent times). Traditionally, the oil and gas industry has operated within a relatively free-trade environment, with prices primarily determined by supply-demand dynamics and production costs. However, the increasing use of energy as a geopolitical tool has introduced trade policies as a significant macroeconomic factor affecting oil and gas industry operations.

Many fear that such protectionist measures could lead to retaliatory actions, creating a complex web of trade barriers that further segment global energy markets. And so here, it’s about recognising that energy markets are increasingly influenced by broader macroeconomic trade policies rather than purely energy-specific factors.

Above: Macroeconomic factors affecting oil and gas industry – Brent crude oil market sentiment taking from our Trading Co-Pilot – one week view

OPEC+ dynamics and supply management

Coming back to supply factors, OPEC+ continues to play a pivotal role in the macroeconomic factors affecting oil and gas industry pricing. Even though we know that OPEC+ influence has diminished somewhat with the rise of non-OPEC production, particularly U.S. shale, the cartel’s decisions still create significant price movements. For example, on March 21, prices were influenced by new US sanctions on Iran and OPEC+ plans to cut production, highlighting the continued importance of coordinated supply management as a macroeconomic factor affecting oil and gas industry dynamics.

However, despite these difficulties in managing global supply, OPEC+ has demonstrated remarkable resilience in adapting to changing market conditions. The key principle governing their actions remains balancing market stability with revenue maximisation for member states, a delicate equilibrium that continues to influence global energy markets.

Weather patterns and climate events

Some might say that weather patterns represent a microeconomic rather than macroeconomic factor, but the increasing frequency and severity of extreme weather events have elevated their importance to a macroeconomic level with severe weather events continuing to disrupt energy infrastructure, causing power outages and raising concerns about energy supply stability.

Indeed, even as recently as March 26, extreme weather conditions, including heavy rains and strong winds, affected production in various sectors, notably in energy and agriculture. This consistent pattern of weather-related disruptions represents a structural macroeconomic factor affecting oil and gas industry operations worldwide.

At the same time, these weather events influence both supply and demand sides of the equation. For instance, on March 25, ongoing extreme heat led to concerns over agricultural productivity and energy consumption highlighting how climate events create complex feedback loops in energy markets.

Macroeconomic factors affecting oil and gas industry – European natural gas market sentiment – one month view

Global economic growth and demand trends

Perhaps now, we had better move on to the most fundamental macroeconomic factor affecting oil and gas industry performance: global economic growth. The hard truth is that energy demand remains tightly coupled with economic activity, despite ongoing efforts to decouple growth from carbon emissions.

Our Trading Co-Pilot data shows that positive economic indicators continue to support price rallies. For example, on March 20, the market reacted positively to a strong outlook for demand in the US, supported by positive economic data, driving petrol prices higher.

Nevertheless, it’s important to note that regional economic variations create complex patterns in global energy demand. Thus, while some regions experience robust growth supporting higher energy consumption, others face economic headwinds that constrain demand growth.

Technological disruption and energy transition

You may have been aware that the Texas Senate recently passed legislation aimed at restructuring the energy market to favour gas over renewable sources, highlighting the ongoing tensions between traditional and emerging energy sources. This is a curious state of affairs for many industry observers, as technological and economic factors increasingly favour renewable energy, while policy measures attempt to maintain support for fossil fuels.

The explanation is ultimately quite simple: the energy transition represents one of the most significant macroeconomic factors affecting oil and gas industry long-term prospects, creating complex political and economic responses across different regions.

There are, of course, significant variations in how this transition is unfolding globally. Some regions are accelerating their shift away from fossil fuels, while others are doubling down on oil and gas development. In consequence, the global energy landscape is becoming increasingly fragmented, with different regions following divergent paths determined by their unique resource endowments, policy preferences, and economic structures.

Market sentiment and investor behaviour

No doubt, sentiment plays a key role in short-term price movements in energy markets. With hedge funds recently and significantly reducing their bullish positions on natural gas, this marks a notable shift in market sentiment. This type of positioning can amplify price movements independent of fundamental supply-demand dynamics.

After all, what do these sentiment shifts tell us about the broader macroeconomic factors affecting oil and gas industry performance? They often reflect evolving perceptions of risk, growth prospects, and policy direction, serving as a leading indicator of market trends.

If all that is not enough to complicate the analysis, consider that sentiment can shift rapidly based on news headlines or unexpected events. For instance, the Russia-Ukraine ceasefire agreement regarding Black Sea navigation immediately influenced market sentiment, despite having limited immediate impact on physical supply routes.

Navigating a complex interplay of factors

To sum up, the macroeconomic factors affecting oil and gas industry performance in 2025 represent a complex and evolving landscape. Geopolitical tensions, trade policies, OPEC+ dynamics, weather patterns, economic growth, energy transition, and market sentiment all interact to create a challenging environment for industry stakeholders.

Worse still, these factors don’t operate in isolation but create feedback loops and cascading effects across the energy ecosystem. Thus, a comprehensive understanding requires monitoring multiple indicators simultaneously, recognising both immediate impacts and longer-term structural shifts.

For investors and industry participants, this complexity highlights the value of sophisticated analytical tools like our Trading Co-Pilot, which processes multiple data streams to identify emerging trends and potential market movements. In the struggle against uncertainty, tools like ours provide valuable insights that can inform more effective risk management and strategic decision-making.

Harness the power of AI-driven market intelligence to navigate the complexities of today’s energy markets

Our Trading Co-Pilot delivers real-time analysis of macroeconomic factors affecting the oil and gas industry, helping you identify emerging trends and potential market movements before they become obvious. Experience how our sophisticated analytical tools can transform your approach to risk management and strategic decision-making. Simply email our team at enquiries@permutable.ai today to arrange your personalised demonstration or fill in the form below to begin your complimentary trial.