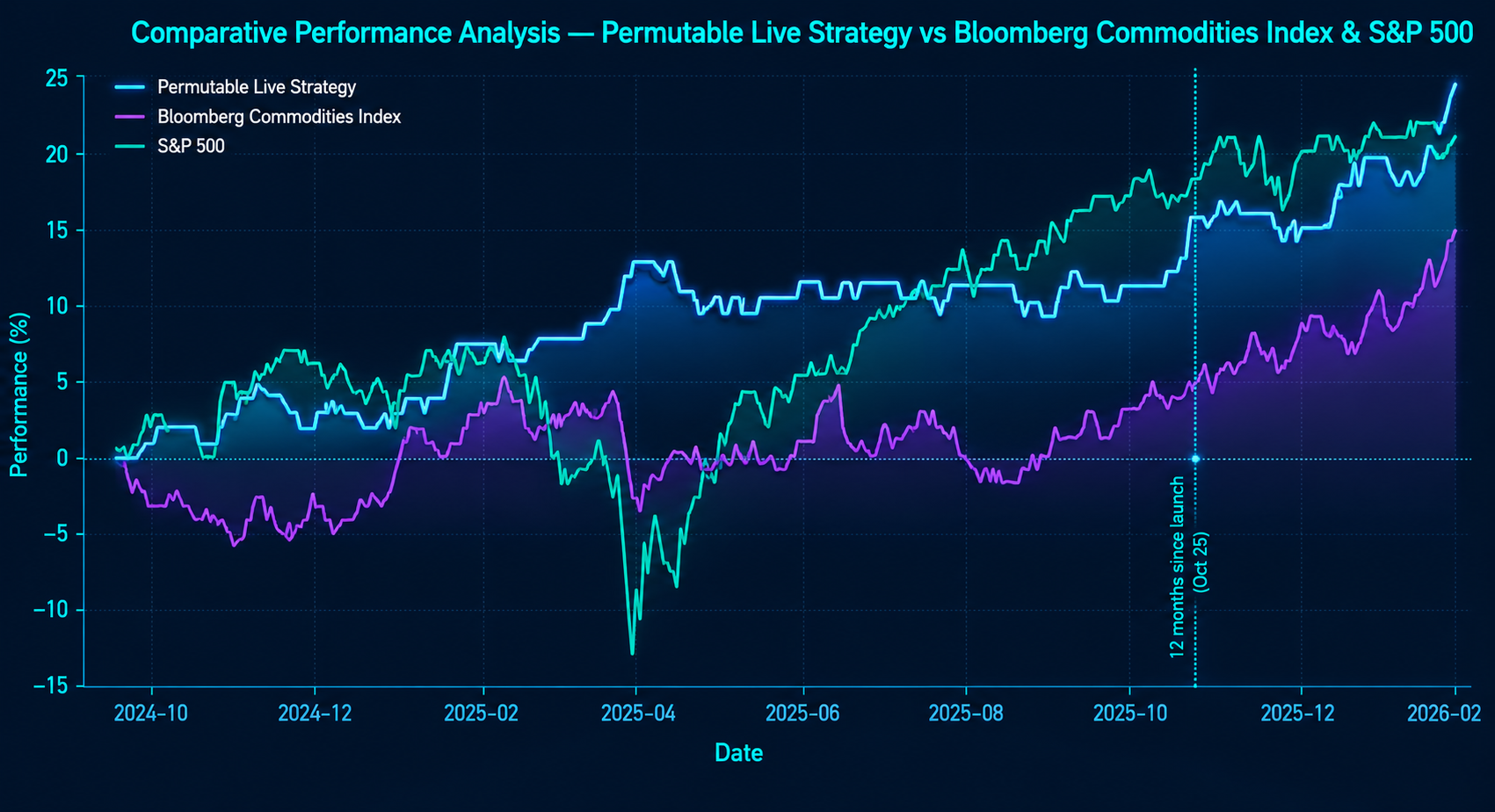

Validated sentiment alpha for systematic trading

Permutable’s proprietary market sentiment signals have been tested in live trading conditions across a 16-month commodities futures experiment, delivering 28.54% total return, 20.86% annualised return, 7.01% annualised volatility and a maximum drawdown of just -2.95%.

Built from AI-driven market intelligence and deep sentiment analysis, our signals are designed for institutional systematic traders seeking differentiated, low-beta data inputs across highly liquid global futures markets. Whether you are looking to integrate our data into your own systematic strategy, evaluate our signal performance, or explore running a book together, we would welcome a conversation.

For institutional enquiries, email enquiries@permutable.ai