This article explores the key forces shaping global industrial metal supply as we move through late 2025 – from macroeconomic pressures to the energy transition – and is aimed at investors, analysts, and professionals across the industrial metals and commodities sectors seeking deeper, data-driven insight.

The industrial metals sector is entering a pivotal new chapter. As we move through Q4 2025 and into 2026, multiple macroeconomic, regulatory, and demand-side forces are reshaping industrial metal supply, pricing dynamics, and the competitive balance across global industrial metal industries. For investors, producers, and market analysts, understanding these shifts is paramount, with the next 18 months testing how robust global supply chains really are. In this article, we explore the key themes defining the future of industrial metal supply.

Global growth concerns continue to cast a long shadow over the industrial metal landscape. Heavy infrastructure spending in emerging economies still offers upside, but developed markets are stagnating. China, the largest consumer of industrial metals, remains pivotal – any slowdown in its property or manufacturing sectors can ripple through the entire industrial metal supply chain.

Analysts suggest that 2025 represents a cyclical peak in metals demand, leaving future expansion increasingly fragile. This poses challenges for metals heavily linked to industrial use – such as copper, aluminium, nickel, and zinc – which may struggle unless substitution or fiscal stimulus steps in to sustain demand.

On the supply side, the picture is equally complex. Several major producing nations are tightening export controls or facing energy, labour, and environmental constraints that threaten industrial metal supply stability. Escalating geopolitical tensions, tariffs, and trade policy fragmentation are all influencing cross-border flows.

Energy costs remain a decisive factor. Mining and smelting are energy-intensive activities, and higher electricity prices in key regions have throttled output, creating further imbalances. Within industrial metal industries, producers are also facing pressure to meet stricter ESG and sustainability mandates – often at the expense of operational flexibility.

For critical or specialty metals such as cobalt, rare earths, and lithium, extraction and processing remain heavily concentrated in a few jurisdictions, making the industrial metal supply chain highly vulnerable to disruption and regulatory change.

Despite short-term volatility, the long-term case for transition metals remains compelling. As the world accelerates towards electrification and renewable energy, industrial metals such as copper, nickel, lithium, and aluminium will remain essential to building batteries, solar infrastructure, and modern power grids.

These sectors create strong structural demand but also increase exposure to volatility with low substitutability and regional supply concentration amplifying price swings. For participants across industrial metal industries, managing this volatility will be key to capturing value during the energy transition.

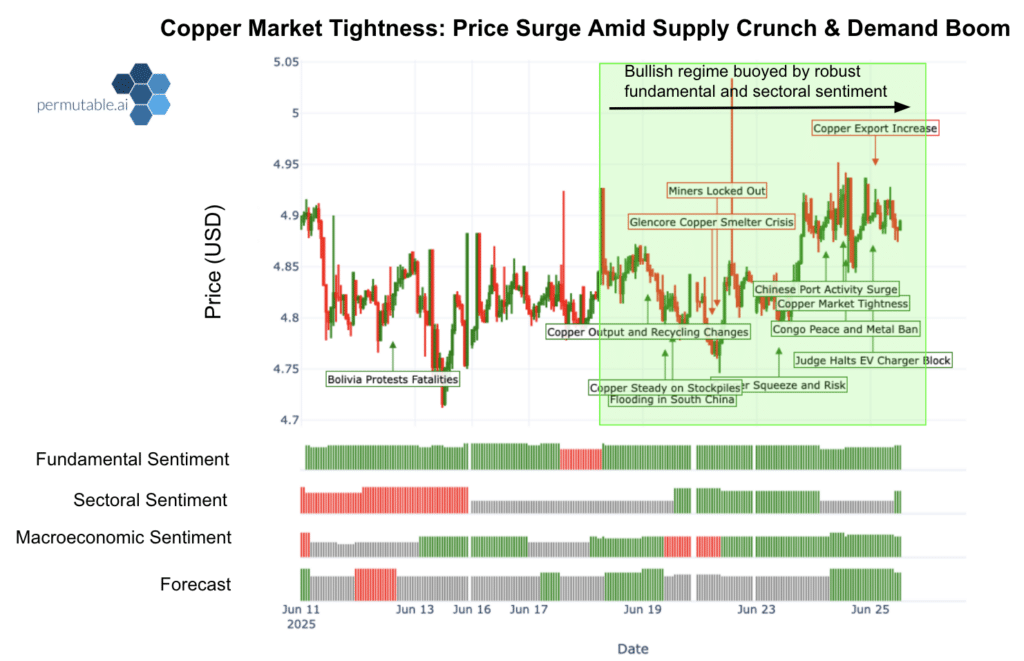

Low visible inventories, especially on exchanges like the LME, mean that any imbalance in industrial metal supply can trigger outsized price movements. Market sentiment and speculative trading increasingly influence short-term price action, sometimes overshadowing fundamentals. In this environment, data granularity and timing matter. Understanding where physical stocks are building or depleting gives traders and producers alike a competitive edge.

Not all industrial metals will follow the same trajectory.

Copper remains the most structurally supported metal thanks to its central role in electrification and grid infrastructure.

Aluminium faces tight energy margins and potential localised supply constraints.

Steel and zinc continue to reflect weak property and construction trends in key consuming regions.

Specialty metals such as nickel and rare earths remain vulnerable to investor sentiment and policy shifts.

This divergence underlines how industrial metal industries must increasingly adapt their production and trading strategies to each metal’s unique demand story.

With global industrial metal supply chains under strain and market dynamics shifting daily, traditional analysis is no longer enough. Advanced AI systems now offer a significant advantage by monitoring vast streams of data in real time – from economic releases to social sentiment and trade flows.

Our industrial metals market intelligence integrates macroeconomic indicators, shipping data, and sentiment analysis to deliver predictive insights across the full metals spectrum. These systems help market participants:

Detect early signs of regional supply stress

Map correlations between energy and industrial metal pricing

Forecast sentiment-driven market momentum

Quantify policy and regulatory risk

At Permutable, by combining human expertise with explainable AI models, we help investors and institutions turn global complexity into actionable foresight.

Policy and climate mandates: New carbon and export policies may alter industrial metal supply dynamics or create premiums for green-certified metals.

Capital discipline in mining: Cost inflation and ESG demands could delay new projects, tightening industrial metal supply further.

Inventory signals: Rapid restocking or depletion patterns may indicate early shifts in market balance.

Demand shifts: Changes in automotive or grid investment cycles could reallocate demand unexpectedly.

Trade flows: Any disruption in cross-border logistics may have a disproportionate impact on specific industrial metal industries.

As Q4 2025 gives way to 2026, the global industrial metal supply ecosystem faces both turbulence and opportunity. Structural demand from electrification and energy transition remains robust, even as cyclical headwinds persist. Success in this market will depend on foresight – the ability to integrate data, technology, and domain expertise into real-time decision-making.

For producers, traders, and investors alike, AI-driven industrial metals intelligence powered by our Trading Co-Pilot are invaluable as a foundation for navigating uncertainty and capitalising on the next evolution of industrial metals.

Request a demo of our newly launched Industrial Metals Market Intelligence and discover how data-driven foresight can help you stay ahead of global market shifts.

01 May 2026

Aluminium and copper outlook 2026: Separating scarcity from demand risk

Read more >

30 Apr 2026

Commodity shock transmission: How real-time sentiment signals reveal market moves before price adjusts

Read more >

30 Apr 2026

Weekly current precious and industrial metals sentiment: Is bullish momentum returning or fragmenting across markets?

Read more >