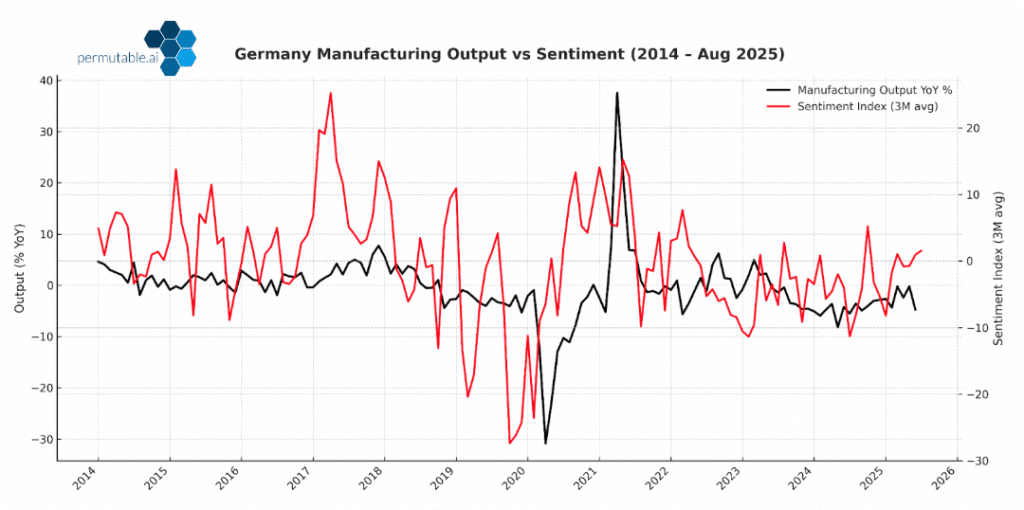

In this article, we examine the shifting dynamics of Germany’s manufacturing sector through the lens of German Manufacturing Sentiment. Over the past three years, the sector has endured one of its deepest downturns in decades, hit by energy shocks, trade frictions, and collapsing demand. Output contracted persistently, orders weakened, and investment stalled. Yet market sentiment, which often turns before the hard data, is now pointing in a different direction.

In 2025, the German Manufacturing Sentiment index has begun to stabilise. Volatility has eased, with downturns shorter, rebounds quicker, and expectations no longer set on relentless decline. This matters because market sentiment often leads activity.

When firms stop anticipating contraction, they begin to plan for stabilisation, laying the groundwork for recovery. The sector is not yet expanding, but the levelling-off of expectations marks a critical inflection point. The cycle appears to have reached a floor and the road toward recovery is starting to open.

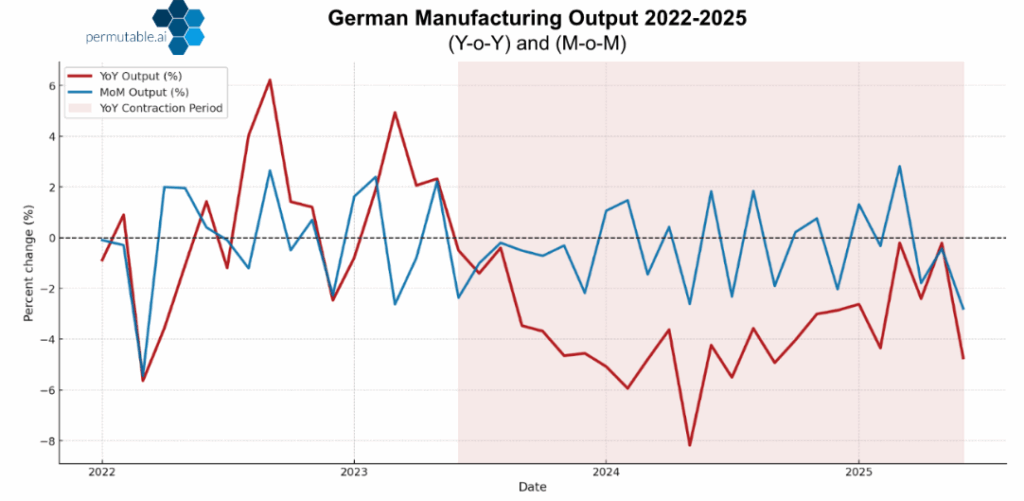

Germany’s manufacturing base has endured one of its sharpest contractions in decades. Output fell continuously for 25 months between mid-2023 and mid-2025, as firms slashed orders, cut staff, and scaled back investment. Confidence swung decisively, collapsing under energy shocks, shrinking exports, and rising cost pressures, before rebounding only briefly. Order books thinned, inventories were run down, and output fell hardest in autos and capital goods.

Recently, Germany’s manufacturing sentiment has begun to stabilise. The volatility that defined the downturn has eased: the downswings are shorter, rebounds arrive more quickly, and firms are no longer positioning for relentless slide. Expansion plans remain muted, but expectations have clearly pivoted to the upside. Because sentiment often turns before activity, this levelling-off is less about imminent growth and more about laying the foundations for normalisation.

Germany’s manufacturing data suggest the contraction has bottomed out, even if recovery remains fragile. Output is down more than -2% since the beginning of the year, yet monthly prints are showing signs of stabilisation after an early boost from front-loaded U.S. demand. Order books have softened as foreign flows gradually pick up, though a modest lift in domestic uptakes provides some offset.

The latest PMI surveys reinforce this picture. They remain below the 50 growth threshold, yet the sector’s mood has reached its most upbeat level in three years. Backlogs are no longer shrinking, pointing to a floor in activity rather than renewed growth.

Input prices have also declined, helped in part by euro appreciation, which eases cost pressures and allows lower prices to be passed on to buyers. Manufacturers remain wary, continuing the stint of trimming jobs and operating with minimal base line of inventories, measures consistent with staying afloat rather than preparing for expansion.

Against this backdrop, the recent stabilisation is significant. Production has steadied, export orders are beginning to hold up, and sentiment is no longer waning. External demand remains the sector’s beacon of light. EU markets continue to sustain flows, but U.S. tariffs and intensified Chinese competition weigh heavily on the sector.

Domestic demand is too weak to offset these pressures, reflected in the lacklustre GDP prints, having risen just 0.2% y-o-y in Q2 but contracting -0.3% q-o-q. Economists expect growth to flatline through 2025-end. Taken together, the manufacturing base and the wider German economy are showing clear signs of stabilisation, but an expansionary phase has yet to materialise.

Germany’s stabilisation comes at a pivotal moment for the eurozone. Four of the eight countries appear to be back in expansion phase, but Germany is not yet among the pack. The sector in France, Italy, and Austria remain under challenging conditions, dragging on the eurozone overall activity. As both the industrial hub of Europe and the largest importer, Germany’s eventual return to growth would provide the decisive lift the eurozone needs.

The trajectory can be seen in three phases:

In this article, we have shown that German manufacturing has stopped falling. Sentiment has stabilised, production is holding, and EU demand provides partial support. Yet stabilisation does not automatically signpost a recovery. Competitiveness strains, tariffs, and subdued growth conditions keep fragility in place.

The decisive point is what market sentiment tells us. Germany’s manufacturing sentiment is signalling that the contraction phase is coming to a halt. It does not point to imminent growth, but it marks a turning point in expectations, from staying afloat to stabilisation, from cutbacks to planning for the road ahead.

For economists and strategists, this is key. The hard data is lagged, but market sentiment signals a pivot is coming. Whether this stabilisation becomes a durable recovery will rest on a revival in demand, pricing power, and a relief from politically tied trade pressures.

To learn more about our regional macro indices and how they can support your strategy, contact us at enquiries@permutable.ai.

Read our latest Permutable Perspective monthly publication here and sign up to our weekly Permutable Insights newsletter here.

A: It tracks the tone, intensity, and breadth of market sentiment around Germany’s manufacturing sector, derived from news, surveys, and commentary. It often signals turning points before official output data confirms them.

A: As Europe’s industrial hub, Germany’s sectoral health drives eurozone growth. Shifts in sentiment provide early warning of stabilisation or renewed downturn, influencing bonds, equities, and currency markets across the region.

A: While output remains fragile and below pre-crisis levels, sentiment has stabilised, marking a shift from persistent contraction to cautious normalisation. This could indicate the start of a bottoming-out phase.

A: Sentiment indices provide forward-looking signals, capturing the expectations and mood of firms and markets before they show up in lagging indicators like output or GDP.

Analysis

29 Jul 2026

South Korea economy: the chip windfall is outrunning domestic growth

Read more >

27 Jul 2026

The tide turns on Russia inflation outlook as drone strikes spread from refineries to warehouses

Read more >

Analysis

27 Jul 2026

Saudi supply risk and import costs drive energy inflation sentiment higher

Read more >