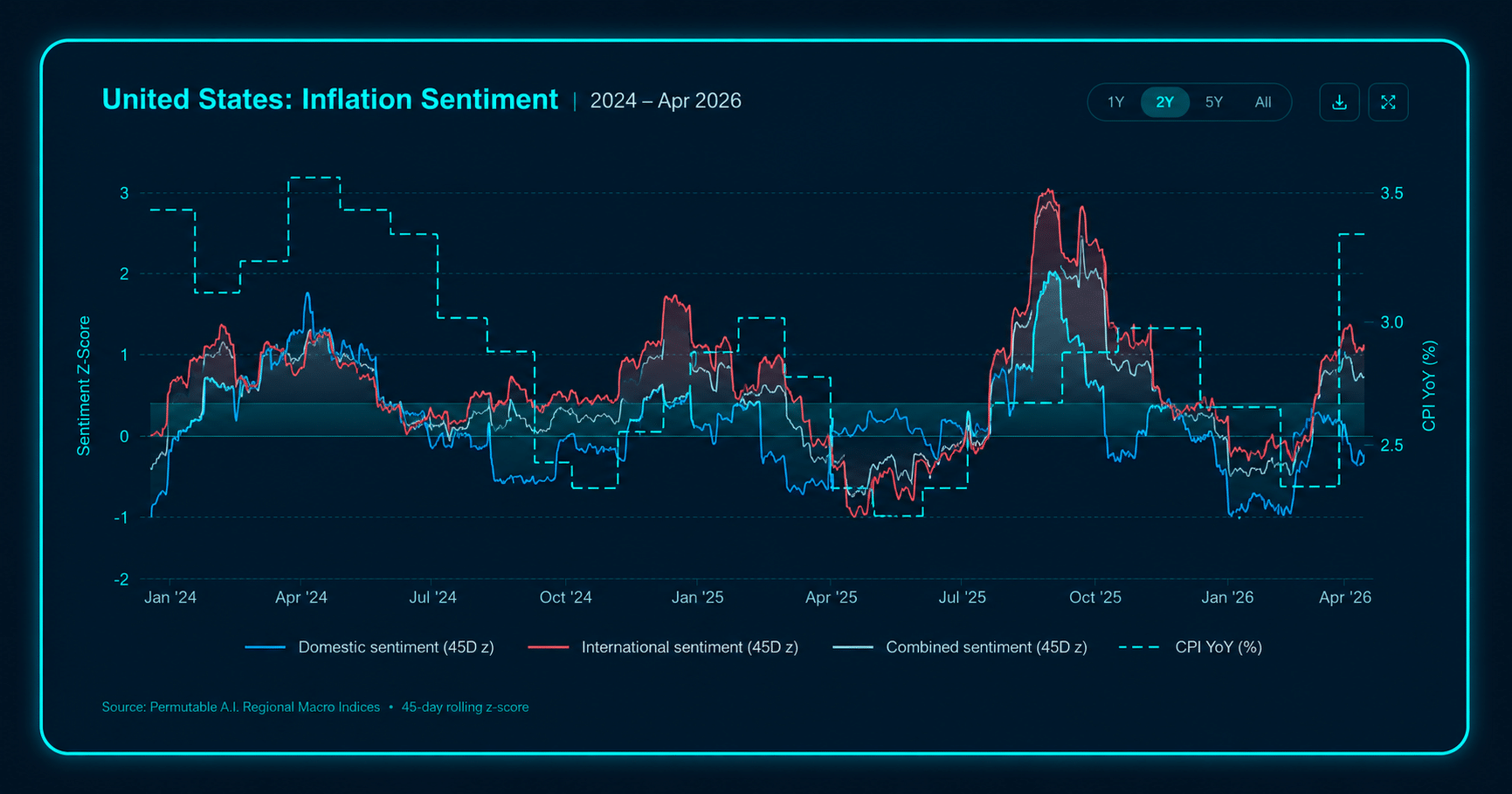

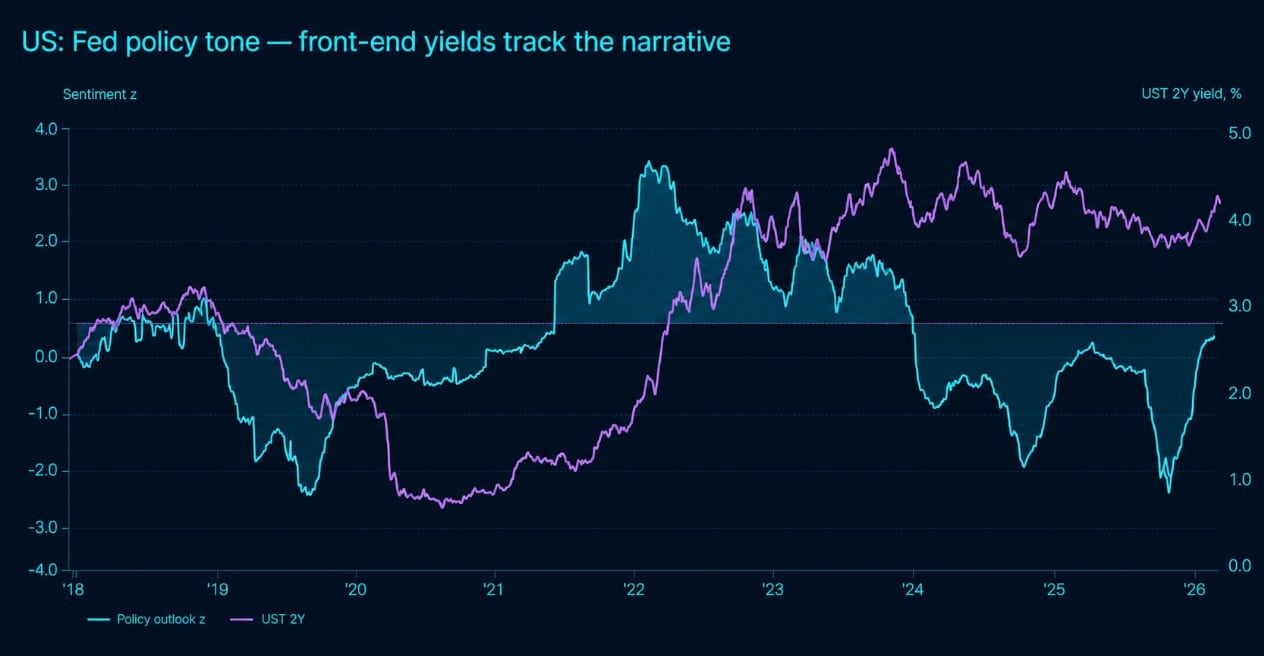

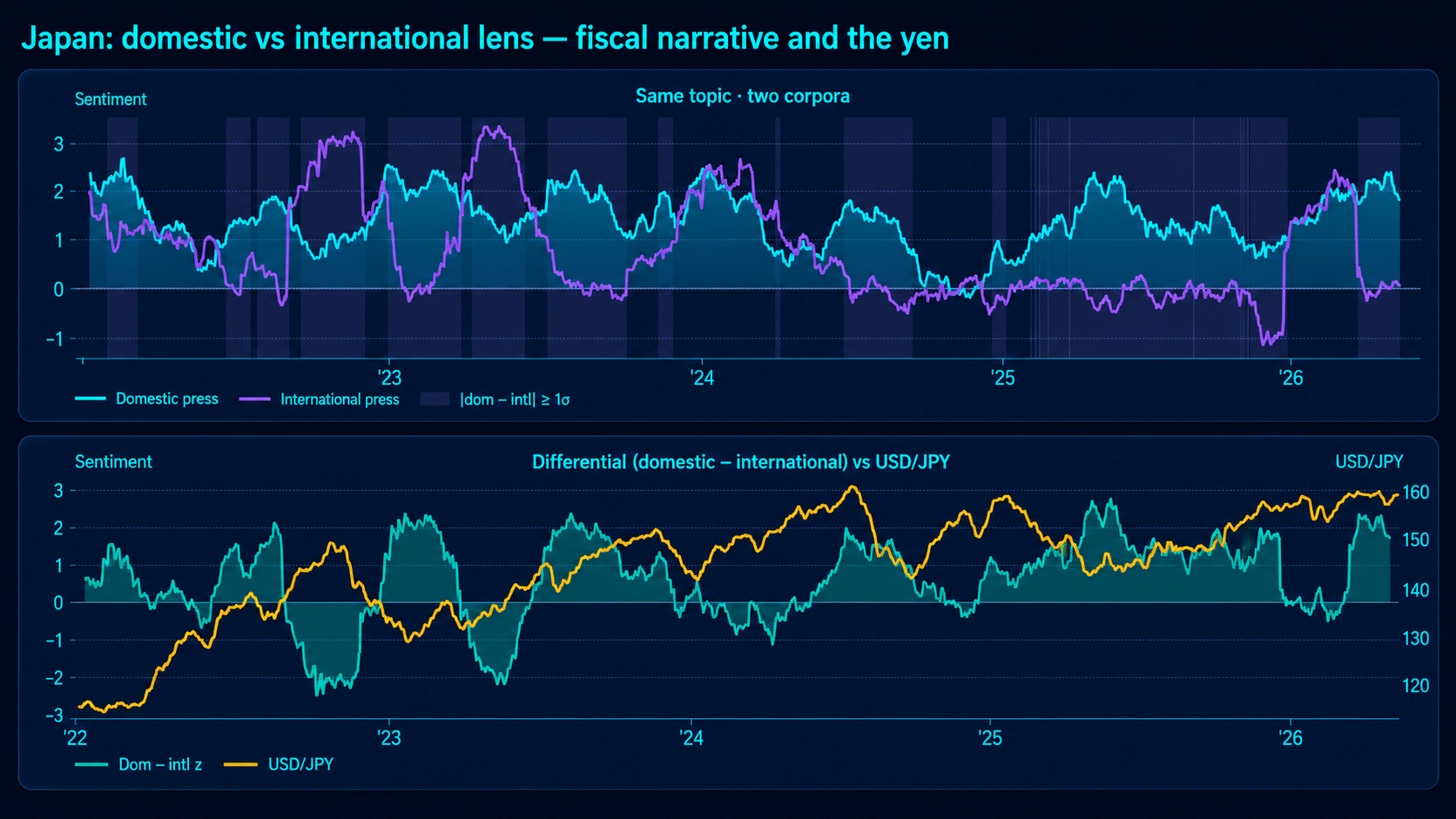

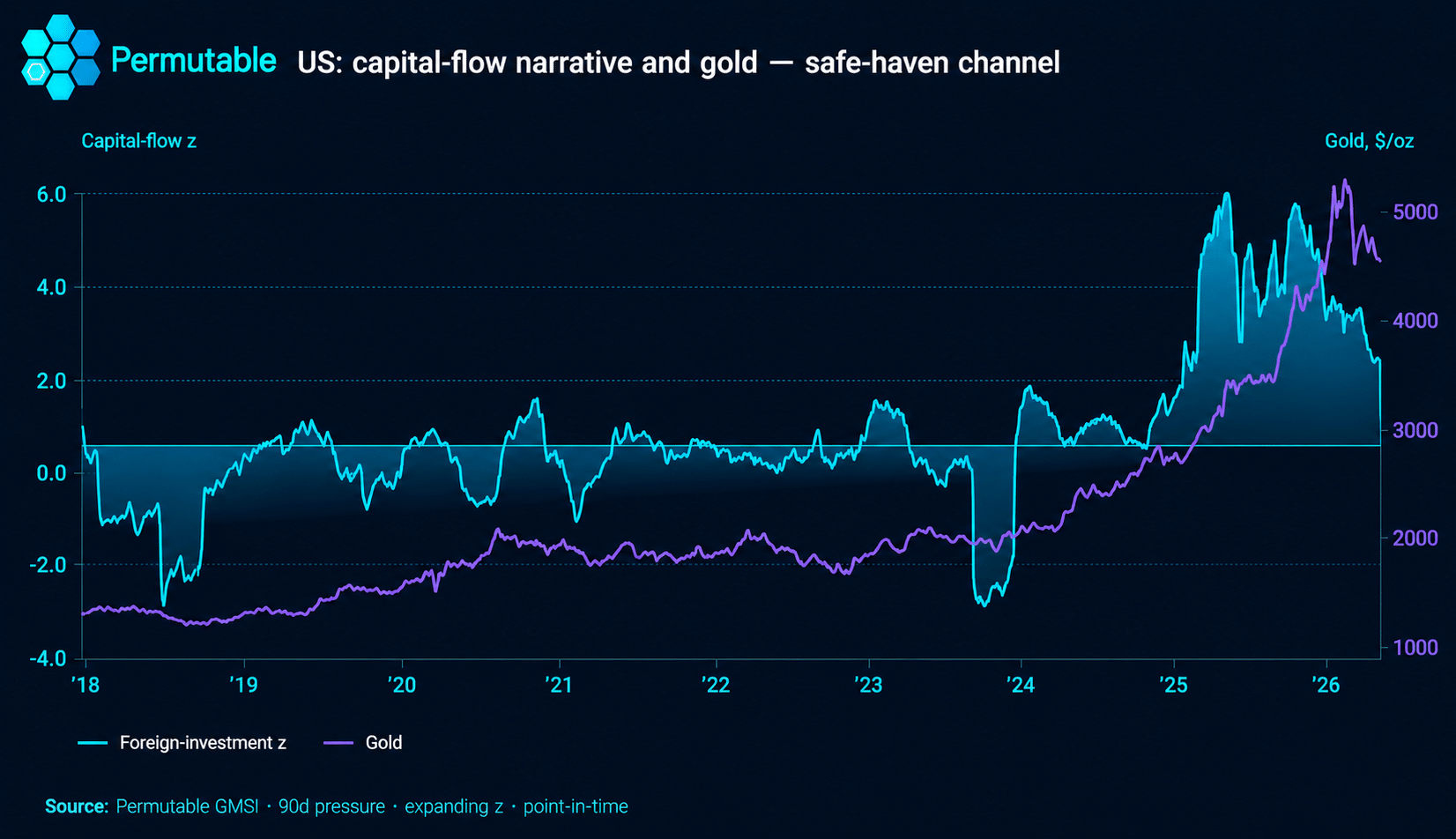

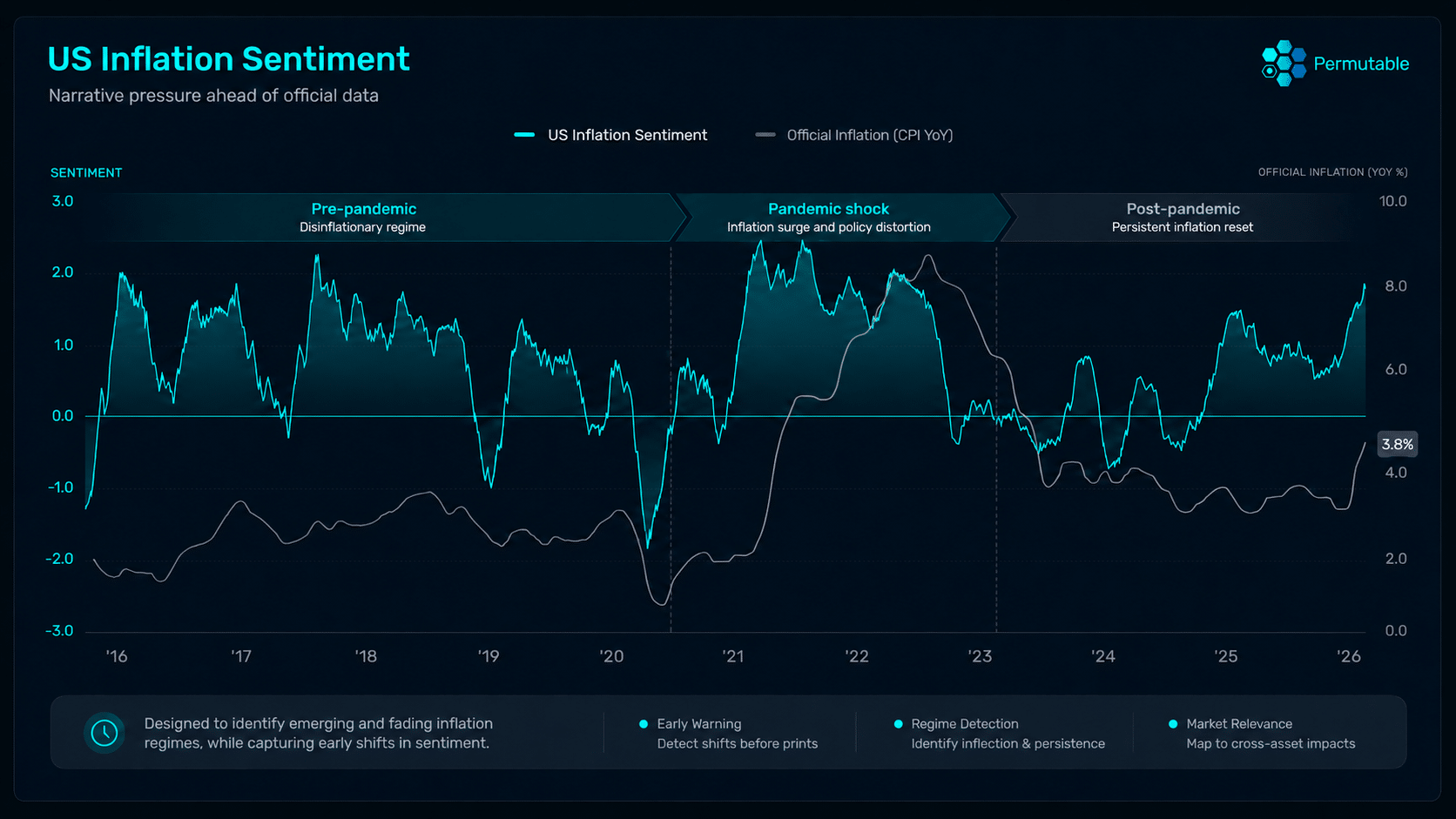

The global economy shifts before the data confirms it

Track inflation, growth, monetary policy, fiscal pressure and political risk through hourly, point-in-time macro sentiment intelligence across global economies.

Recognised at the Hedgeweek European Awards 2026 as Technology Provider of the Year: Innovation, Permutable helps institutional teams identify where macro pressure is forming, how narratives are changing and when those shifts may become relevant for rates, FX, commodities and cross-asset portfolios.

- Track inflation, growth, and policy sentiment across global economies in real time

- Detect macro regime shifts before official economic releases and market consensus

- Monitor cross-market transmission and repricing across FX, commodities, and rates