US inflation trends are proving stubborn – our Global Macro Sentiment Indices maps the pressure beneath them

09 Jun 2026

09 Jun 2026

This article examines how US inflation trends are complicating the case for a Federal Reserve rate cut in 2026. Using Permutable’s forthcoming Global Macr0 Sentiment Indices inflation sentiment series, it explores pressure across energy, services and household-facing prices. It is aimed at macro analysts, traders, investors, economists and policy watchers tracking inflation persistence and Fed policy risks.

US inflation trends are showing that disinflation remains uneven. While US inflation is below its recent peaks, Permutable’s Global Macro Sentiment Indices series suggest pressure is rebuilding across energy, services and household-facing prices, raising the bar for a Federal Reserve rate cut in 2026. The case for a Fed cut in 2026 rests on US inflation trends becoming less persistent, not merely lower than before.

Our Global Macro Sentiment Indices – which tracks market and media sentiment signals across macro themes, commodities and inflation-linked categories – shows pressure rebuilding across energy, services and household-facing prices, making the easing path less straightforward.

The difficulty for policymakers is that the latest inflation signal is moving in the wrong direction for a simple easing narrative. US-Iran escalation has pushed energy risk back into the macro picture just as underlying inflation has failed to give the Fed enough comfort. In isolation, an oil shock can be treated as temporary. But when services remain sticky and household-facing prices are still visible, energy becomes harder to ignore.

The Fed cannot solve an oil shock. Its policy problem is whether it can cut rates while that shock is leaning against the disinflation path.

For institutional investors, the key implication is that the Fed-cut trade depends less on a single soft inflation print and more on whether disinflation broadens across energy, services and household-facing prices.

That matters across rates, FX, commodities and equities. If inflation persistence remains visible in GMSI signals, expectations for policy easing may need to adjust. A higher-for-longer path would affect duration exposure, dollar positioning, commodity risk premia and equity sectors sensitive to discount rates.

The central question is no longer whether inflation is lower than it was. It is whether US inflation trends are broad enough, durable enough and benign enough to allow policymakers to ease without undermining inflation credibility.

Permutable’s Global Macro Sentiment Indices US inflation sentiment series show the policy problem forming beneath the headline.

Aggregate inflation sentiment has rebuilt into the hard-data move. Energy is the clearest acceleration. Services remain the persistence risk. Food keeps the shock visible to households. That mix matters for the 2026 policy outlook because the Fed does not need inflation to reaccelerate sharply to delay easing. It only needs insufficient evidence that US inflation trends are returning sustainably to target.

In that sense, GMSI is not simply tracking whether inflation is high or low. It is mapping where inflation pressure is becoming more visible across the categories that matter for policy, markets and household expectations.

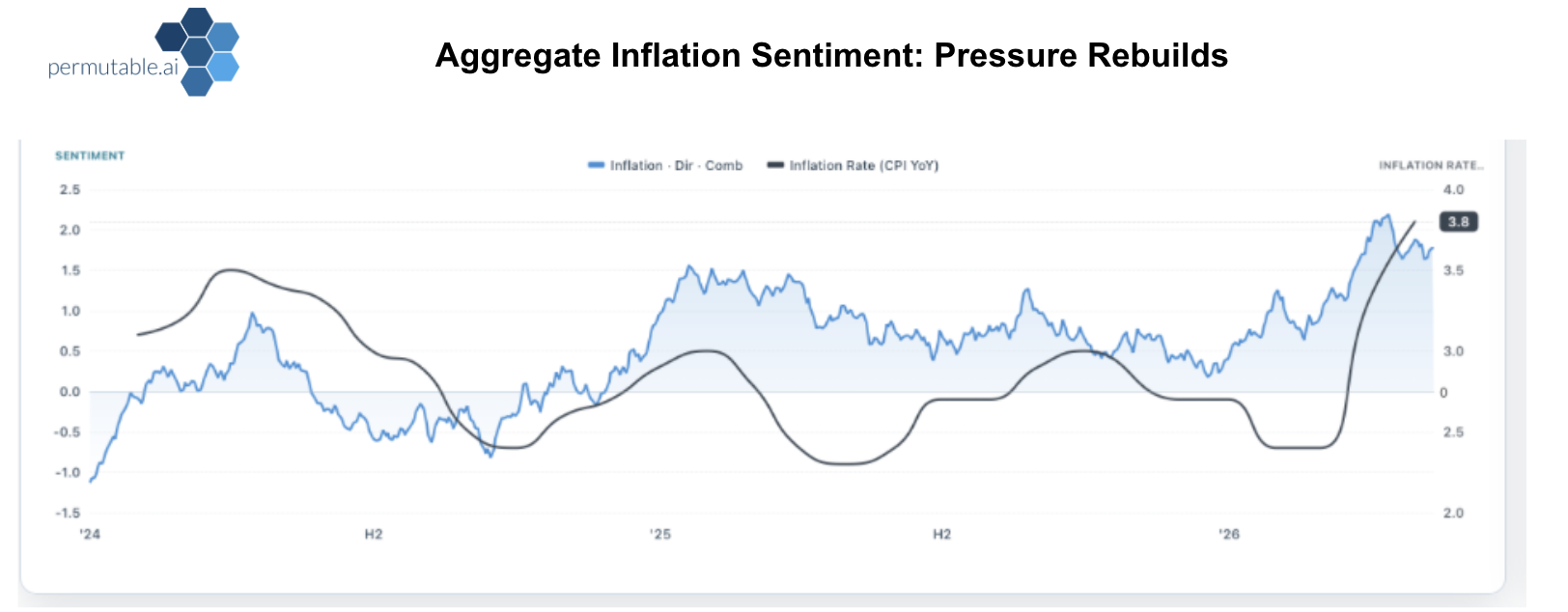

Above: Aggregate inflation sentiment, taken from Permutable’s Global Macro Sentiment Indices shows that overall inflation pressure is rebuilding into 2026, alongside a higher US CPI inflation rate. The signal highlights why the Fed’s easing path depends on broad, durable disinflation rather than a single soft inflation print.

Energy sentiment is the sharpest mover in the GMSI charts, rising as oil and Gulf supply risks move back into view. For policy, the timing is the problem. Energy is rising before the rest of the inflation basket has cooled enough. The channel runs through fuel, freight, input costs and fertiliser.

A temporary energy shock need not change the long-run inflation outlook. But it can still delay a cut if it arrives while the Fed is waiting for confirmation that disinflation is durable. For investors, this makes energy more than a commodity story. It becomes a macro timing risk, especially if oil-linked pressure feeds into breakevens, inflation expectations or central bank communication.

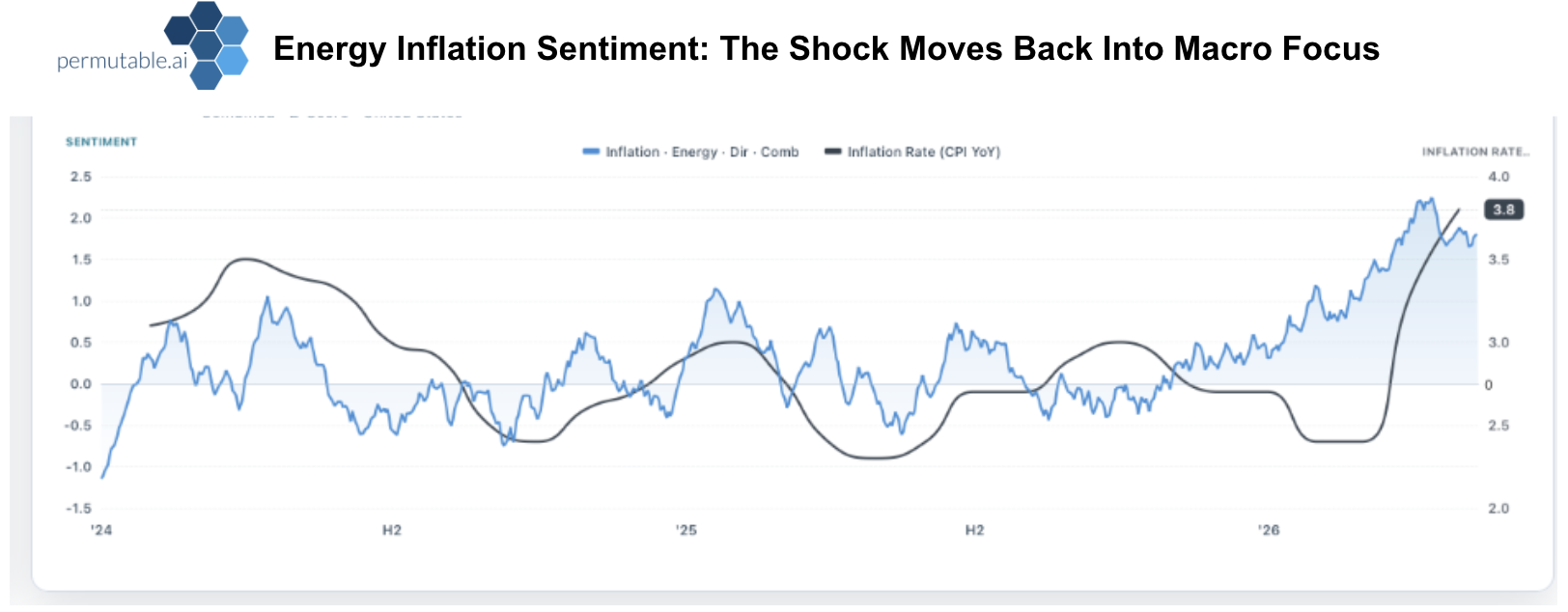

Above: Energy inflation sentiment, taken from Permutable’s Global Macro Sentiment Indices shows energy-related inflation pressure moving back into macro focus, with sentiment rising sharply into 2026 as the US CPI inflation rate also trends higher. The signal highlights why energy remains a key timing risk for the Fed’s easing path.

Services sentiment is less dramatic than energy, but more important for the Fed. Our GMSI signal points to a firmer services picture into 2026, after the 2025 softness. That is the part of inflation policymakers have least room to dismiss. Services reflect domestic price pressure, wage dynamics and persistence.

A cut in 2026 becomes easier if services soften. It becomes harder if energy rises while services remain firm. For institutional investors, services inflation is therefore the constraint on the easing narrative. Energy may provide the shock, but services determine whether the Fed can look through it.

Above: Services inflation sentiment, taken from Permutable’s Global Macro Sentiment Indices shows that services-related inflation pressure remains elevated into 2026, even as the wider inflation outlook shifts. The signal highlights why services stickiness remains a key constraint on the Fed’s ability to ease policy.

Food sentiment is not the main acceleration in our GMSI charts, but it remains positive and stable. That matters because food is where energy and fertiliser costs can move into household expectations. Voters and consumers experience inflation through petrol, food and bills, not through core measures.

For the Fed, household visibility matters because it can slow the rebuilding of inflation credibility. A shock that reaches households is harder to treat as noise as it weighs on expectations. For markets, food-linked inflation pressure can also matter because it affects consumer confidence, real-income expectations and the political backdrop for monetary policy.

http://fx https://permutable.ai/us-monetary-policy-sentiment-short-end-rates-signal/

http://fx https://permutable.ai/us-monetary-policy-sentiment-short-end-rates-signal/

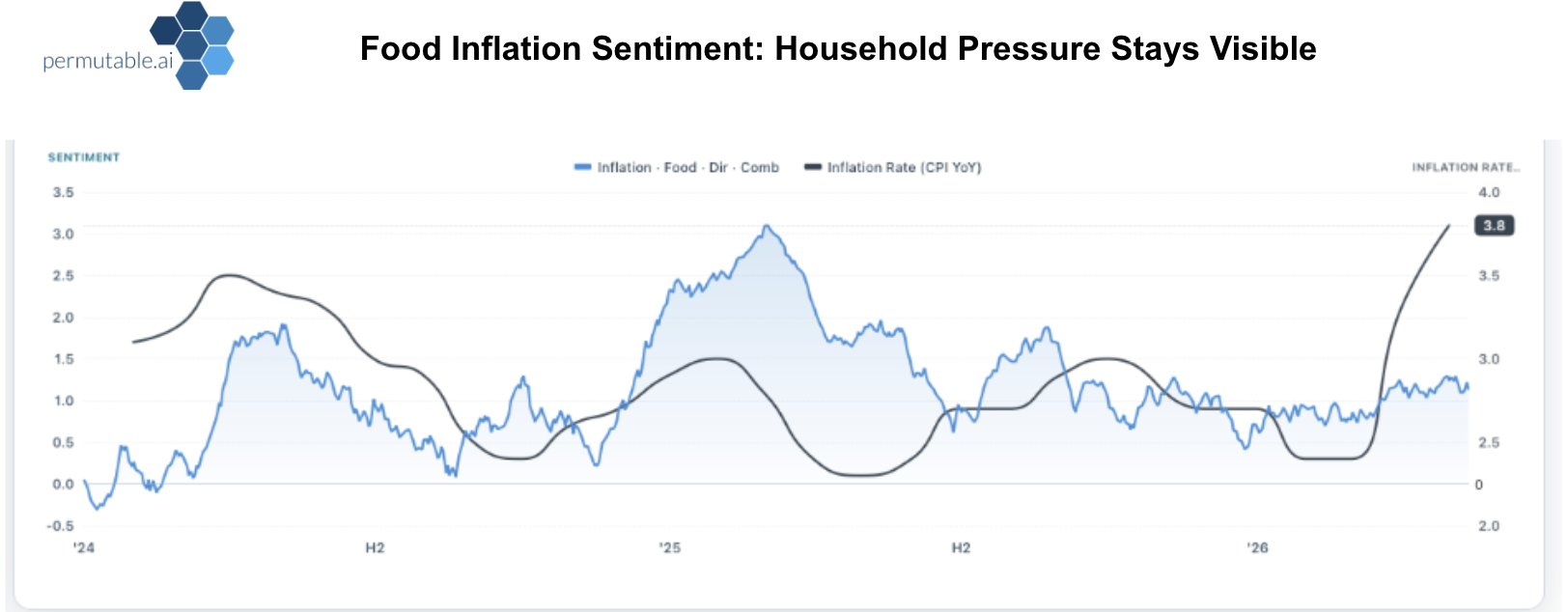

Above: Food inflation sentiment, taken from Permutable’s Global Macro Sentiment Indices shows that food-related inflation pressure remains visible into 2026, even as the wider inflation outlook shifts. The signal highlights why household-facing price pressure remains important for the Fed’s inflation credibility and easing path.

The easing story is not entirely off the table. But the threshold for a 2026 cut has risen. The Fed now needs evidence that energy pressure is fading, services inflation is cooling, and household-facing inflation is not rebuilding expectations. A soft print buys time, not permission.

The Fed can cut in 2026 if the inflation signal turns decisively lower. Permutable’s GMSI is showing why that bar has become higher: the pressure is no longer confined to one volatile component. It is rotating through energy, services and food in a way that makes the policy outlook less forgiving.

The 2026 Fed outlook is no longer just about whether inflation is lower than it was. It is about whether US inflation trends are broad enough, durable enough and able to let policymakers ease without harming growth. Oil risk may still prove temporary. But temporary shocks can still matter when they arrive at the wrong point in the cycle.

Permutable’s upcoming Global Macro Sentiment Indices have been built for teams that need macro signals they can test, monitor and integrate into their own investment, research or risk process.

Whether you are tracking inflation persistence, policy credibility, fiscal strain, political risk or supply-chain stress, Global Macro Sentiment Indices help identify where macro pressure is building, how it is spreading and when it may begin to matter for markets.

Custom macro indices

Build sentiment indices around a country, region, theme, policy cycle or risk regime, allowing teams to monitor the signals most relevant to their exposures.

Macro regime tracking

Track how inflation pressure, policy credibility, fiscal strain, political risk and supply-chain stress are evolving across countries and regions before the story is fully reflected in official data.

Constructed without future look-ahead, GMSI provides historically accurate signals suitable for research, testing and model development.

API access and integration

Available via API for direct integration into trading, research and risk management workflows, with flexible coverage and delivery options.

For discretionary teams, the value is understanding what is changing, where it began and whether it is spreading. For systematic teams, GMSI provides a structured, testable macro signal that can be integrated across asset classes.

Register your interest to receive early access to the Global Macro Sentiment Indices and upcoming product updates.

The main US inflation trends for 2026 are uneven disinflation, renewed energy pressure, persistent services inflation and continued household sensitivity to food and fuel costs. Together, these signals suggest that inflation may be lower than previous peaks but not yet benign enough to make the Fed’s easing path straightforward.

Energy matters because it affects fuel, freight, input costs and inflation expectations. The Fed may look through a temporary oil shock, but if energy pressure rises while services inflation remains firm, it becomes harder for policymakers to justify cutting rates.

Services prices are important because they tend to reflect domestic inflation pressure, wage dynamics and underlying demand. Unlike energy, services inflation is harder for policymakers to dismiss as temporary. Persistent services inflation can therefore keep the Fed cautious even if headline inflation softens.

Yes. Sticky inflation could delay a Fed rate cut in 2026 if policymakers do not see enough evidence that inflation is returning sustainably to target. The Fed does not need inflation to surge again to delay easing; it only needs the disinflation path to look insufficiently durable.

Permutable’s Global Macro Sentiment Indices helps track inflation pressure by analysing sentiment signals across macro themes, commodities and inflation-linked categories. It complements hard data by showing where market and media attention is building around inflation risks, including energy, services and household-facing prices.

Analysis

06 Aug 2026

Spotting macro regime shifts early: lessons from Japan, Turkey and Brazil

Read more >

Analysis

04 Aug 2026

Global industrial production sentiment: Canada, India and South Korea Gain as the UK, Germany and China weaken

Read more >

Analysis

30 Jul 2026

US growth and policy outlook Q2 2026: Q2 bought the Fed time. July may take it back

Read more >