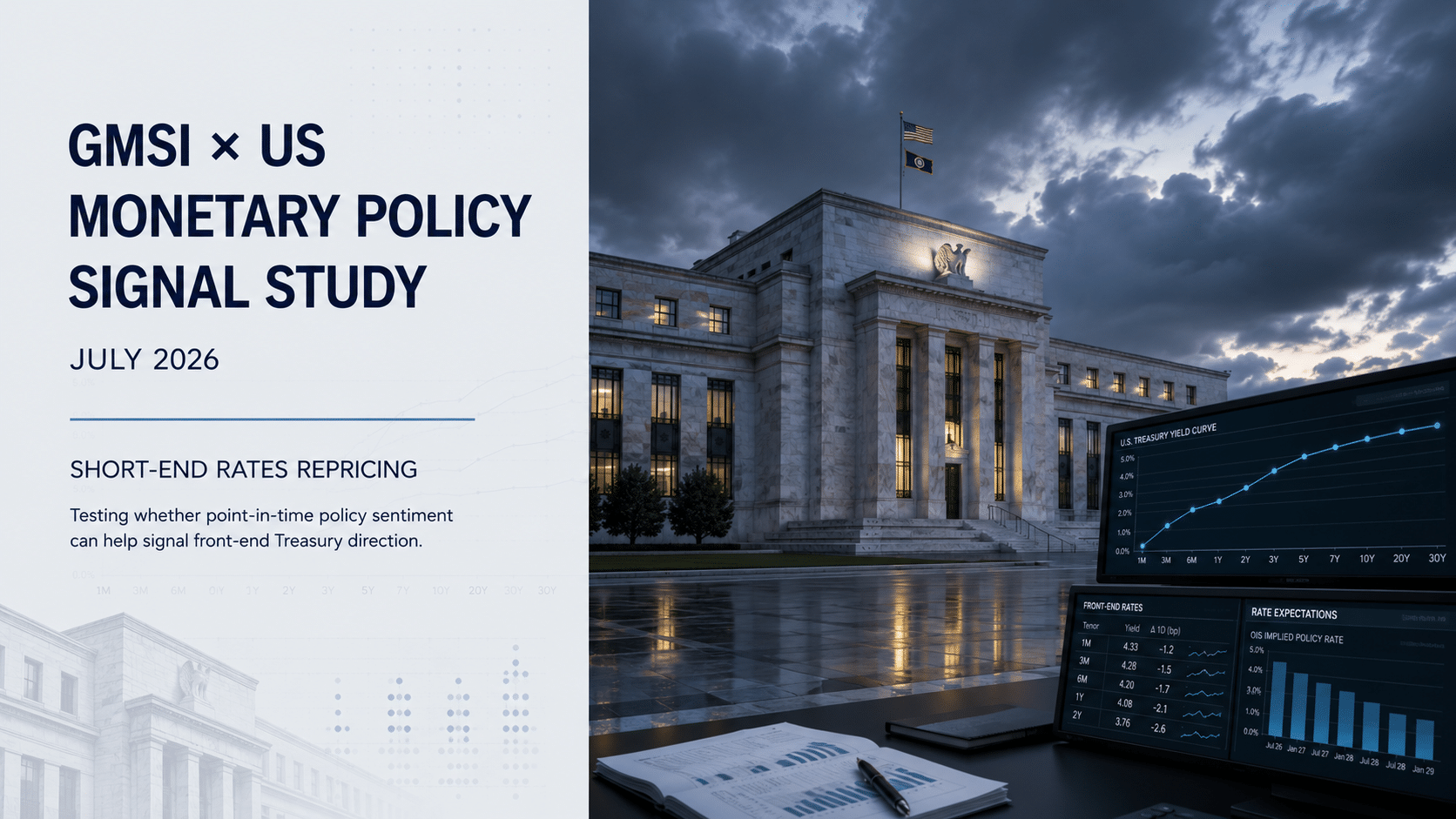

This research note examines whether Permutable’s GMSI US Monetary Policy sentiment can act as a point-in-time signal for short-end Treasury exposure. Using ICE BofA US Treasury 1-3Y Total Return Index backtests, it assesses topic-level policy signals for rates investors, fixed-income strategists, systematic macro teams and portfolio managers seeking explainable overlays for duration risk, policy regime monitoring and research validation workflows.

In this latest Permutable research note, we test whether point-in-time US monetary policy news sentiment from the Global Macro Sentiment Indices can be used as a systematic signal for short-end US Treasury exposure. The study focuses on the ICE BofA US Treasury 1-3Y Total Return Index, using policy news sentiment rather than yield proxies for both signal selection and P&L measurement.

The results suggest that granular policy topics matter. In particular, the GMSI Interest Rates signal produced the strongest single-topic evidence, with a fixed-rule out-of-sample Sharpe of 1.14 from 2019, a 7.2% gross index return and a 73% trade hit rate. A walk-forward selected strategy, using a three-year training window and one-year test window, delivered a 1.09 out-of-sample Sharpe, 6.3% gross return and positive P&L across all eight annual test folds.

For rates investors, the implication is not that sentiment should be treated as a standalone trading model. The stronger interpretation is that policy news sentiment can operate as a transparent, point-in-time overlay for quantifying the tone and persistence of monetary-policy narratives around front-end duration exposure.

Download the full research factsheet

This factsheet examines whether Permutable’s GMSI US Monetary Policy sentiment signals can provide a systematic research input for short-end rates. The study maps extreme dovish policy language to long duration exposure and extreme hawkish language to short duration exposure, using 252-trading-day rolling z-scores of combined directional sentiment.

The research design is deliberately constrained. The target is the ICE BofA US Treasury 1-3Y Total Return Index, not a yield proxy. Signals are lagged by one trading day, positions are rebalanced on non-overlapping 21-trading-day holds, and out-of-sample testing begins in 2019. The walk-forward process selects the best monetary-policy topic using only the prior three years of data before testing it over the following year.

The key finding is that topic specificity matters. The GMSI Interest Rates signal was the only fixed-rule topic with an out-of-sample Sharpe above 1.0, while broader or less directly rate-sensitive policy topics were weaker. This supports the view that front-end Treasury returns are most sensitive to direct shifts in interest-rate language, policy outlook and central-bank reaction-function narratives.

The research also shows why negative or weaker topics are informative. Policy Tools, Independence and broad Monetary Policy averages did not show the same evidence, suggesting that the relationship is not simply generic macro-news beta. Instead, the signal appears strongest where the news narrative maps most directly onto the front-end rates channel.

For institutional investors, the most practical use cases are as a signal overlay, regime monitor and research screen: helping teams quantify whether monetary-policy news is becoming persistently hawkish or dovish, compare topic-level policy signals, and assess whether front-end duration exposure is aligned with the prevailing policy narrative.

| Document | Permutable research factsheet, GMSI × US Monetary Policy |

| Research publication date | 07 July 2026 |

| Sample period | 2016-01-01 to 2026-07-01 |

| Asset target | ICE BofA US Treasury 1-3Y Total Return Index |

| Signal source | GMSI US Monetary Policy topic sentiment |

| Out-of-sample period | 2019 onward |

| Best single-topic signal | GMSI Interest Rates |

| Fixed-rule Interest Rates OOS Sharpe | 1.14 |

| Fixed-rule Interest Rates return | 7.2% gross index return |

| Fixed-rule Interest Rates hit rate | 73% across 33 trades |

| Walk-forward selected OOS Sharpe | 1.09 |

| Walk-forward selected OOS return | 6.3% gross index return |

| Walk-forward hit rate | 73% across 30 OOS trades |

| Walk-forward validation | Positive P&L in all eight annual test folds |

| Core conclusion | Granular monetary-policy topic sentiment, particularly Interest Rates sentiment, appears more informative for short-end Treasury exposure than broad monetary-policy sentiment averages. |

| Important caveat | Results are gross historical simulations and do not include transaction costs, financing, tax, fees, slippage or market-impact assumptions. |

Download the full GMSI × US Monetary Policy factsheet for the complete walk-forward validation, fixed-rule topic comparison and implementation caveats.

Analysis

08 Jul 2026

US inflation sentiment signal shows shift from energy shock to sticky services risk

Read more >

Analysis

01 Jul 2026

Global Macro Sentiment Indices: Turning point-in-time macro sentiment data into live systematic workflows

Read more >

Analysis

17 Jun 2026

Emerging markets inflation signals – a look across Turkey, Brazil and Nigeria

Read more >