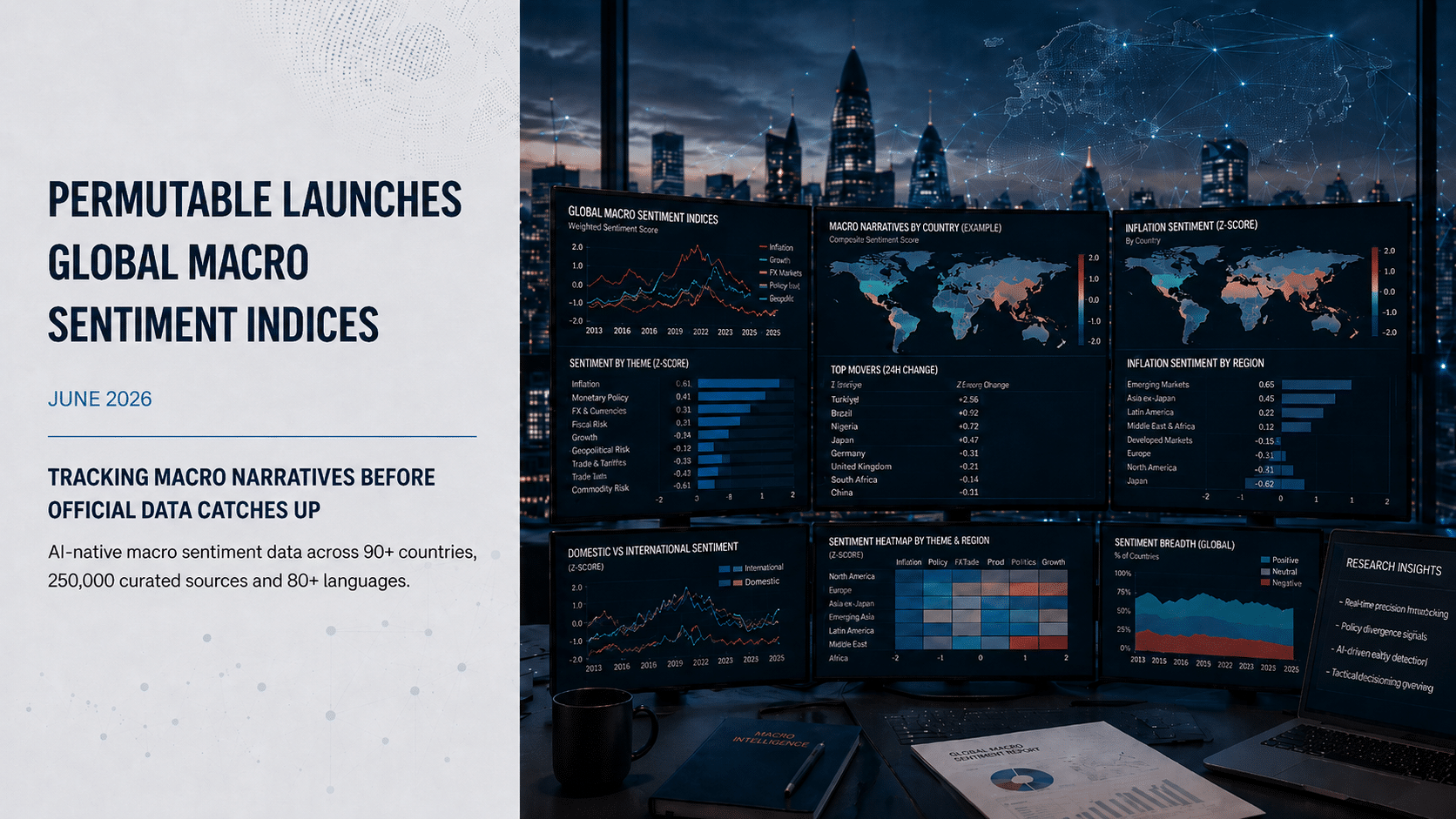

Permutable Global Macro Sentiment Indices launch: Track macro narratives before official data catches up

22 Jun 2026

22 Jun 2026

This announcement introduces the Permutable Global Macro Sentiment Indices, a new suite of point-in-time macro sentiment indicators for institutional investors, macro strategists, FX and rates desks, sovereign-risk analysts and systematic researchers. The indices help teams track inflation, policy, FX, fiscal and political-risk narratives across countries before official data, consensus forecasts or market pricing fully reflect the shift.

We are pleased to announce the official launch of the Permutable Global Macro Sentiment Indices (GMSI), a new suite of macro sentiment indicators designed to help quantitative investors, systematic researchers, macro strategists and risk teams measure how economic narratives form before they are fully reflected in official data or market pricing.

The launch comes at a time when institutional investors are seeking earlier visibility into the information layer shaping inflation expectations, monetary policy risk, FX pressure, fiscal credibility, labour-market stress and geopolitical uncertainty.

Traditional macroeconomic releases remain essential, but they often arrive after market expectations have already begun to adjust. The Permutable Global Macro Sentiment Indices are designed to help investors identify where macro pressure is building before those shifts appear in official releases, consensus forecasts or asset pricing.

GMSI converts real-time global news coverage into structured, country-level macro sentiment signals across key economic themes, including inflation, growth, monetary policy, fiscal policy, trade, labour markets, financial markets, exogenous shocks, FX vulnerability and geopolitical risk.

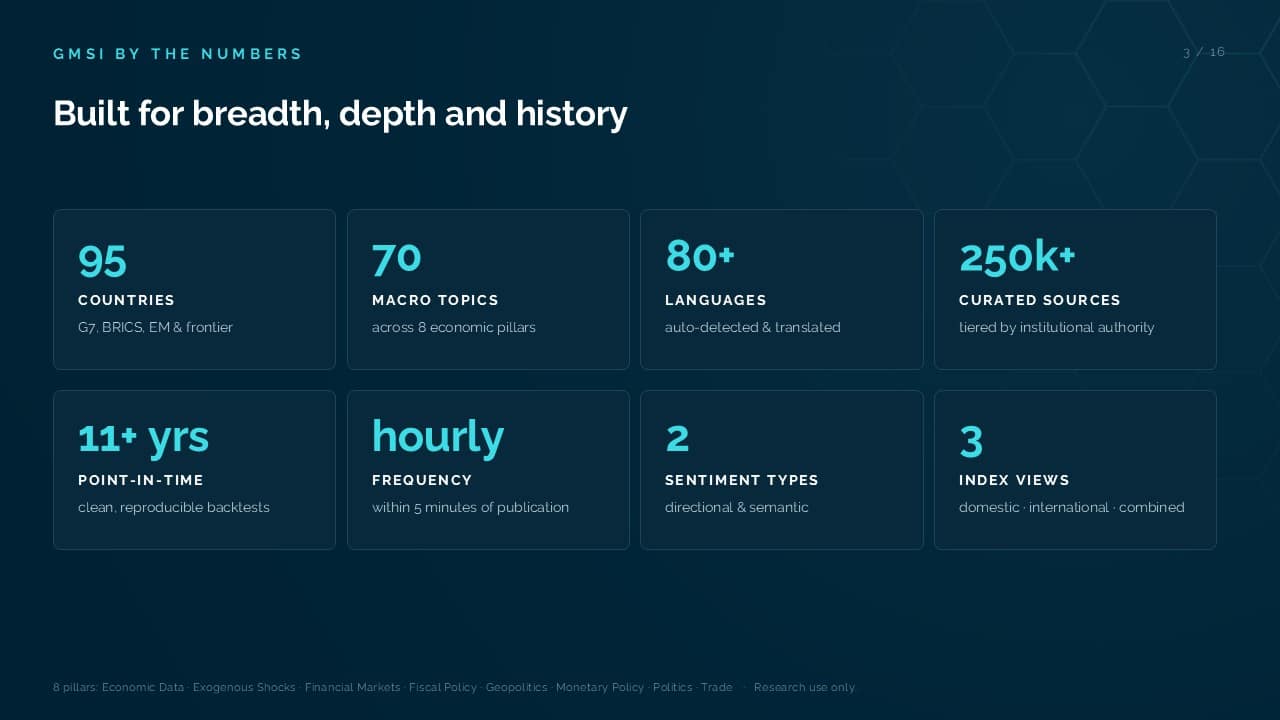

The dataset spans 90+ countries, 70+ macro indicators, 250,000 curated sources and 80+ languages, providing institutional investors with a broader view of the narratives shaping economic expectations across developed, emerging and frontier markets.

“Macro investors have always faced a timing problem,” said Wilson Chan, Founder and CEO of Permutable. “The economy often starts changing before official data confirms it. Inflation pressure, policy credibility, FX stress and political risk first appear in the language of markets, policymakers and local reporting.”

“We have built the Permutable Global Macro Sentiment Indices to make that layer measurable, providing a framework for mapping how macro pressure forms, travels and diverges across the global information environment. By separating domestic narratives from international perception, and by structuring the data point-in-time, we are giving investors a way to see what locals may be seeing before the world prices it in.”

Permutable Global Macro Sentiment Indices have been designed to provide an information layer that is structurally different from traditional macro data.

Rather than relying on market prices, surveys or official releases, GMSI is derived from global narrative flow. This makes it an orthogonal signal source for investment teams seeking to diversify their macro research inputs and identify pressure before it appears in conventional datasets.

The indices are built on more than 11 years of point-in-time history, enabling investors to analyse how macro narratives evolved before previous inflation, policy, FX and sovereign-risk events. Signals are updated hourly, with live data designed to reflect new information as it enters the global information environment.

GMSI represents a significant redevelopment of our award-winning macro sentiment infrastructure.

The framework is powered by a proprietary model trained on Permutable’s source universe and developed specifically for macroeconomic signal extraction. Development used a chronological train-test methodology across approximately 20 million headlines spanning 2015 to 2020, with outputs validated by in-house economists during the training process.

A central challenge in macroeconomic analysis is that financial news rarely carries a single meaning. One article may simultaneously affect inflation expectations, fiscal credibility, monetary policy assumptions, growth sentiment and political-risk perception.

The architecture behind GMSI was designed to classify these overlapping macroeconomic themes with greater precision, enabling country-level signal extraction across domains including inflation, growth, monetary policy, fiscal policy, trade, labour markets, financial markets, FX vulnerability and political risk.

The Permutable Global Macro Sentiment Indices incorporate two complementary sentiment methodologies: directional sentiment and semantic sentiment.

Directional sentiment measures whether news flow is supportive, adverse or mixed for a given macroeconomic theme. It is designed to capture the economic direction of the signal, for example whether inflation pressure is rising, policy tone is tightening or fiscal risk is increasing.

Semantic sentiment captures the tone and market interpretation of the reporting. It assesses whether the language surrounding a macro development is optimistic, cautious, alarming or deteriorating.

This distinction matters because macro news is not always directionally simple. A headline about rising inflation may be directionally positive for inflation pressure while semantically negative in tone. By separating these two readings, GMSI helps investors understand both what is happening and how it is being framed.

The launch marks a substantial expansion in global source coverage.

While many sentiment and alternative data products remain concentrated in English-language news, GMSI incorporates validated local and international sources across developed, emerging and frontier markets. Coverage includes meaningful depth across ASEAN, Latin America, Eastern Europe and Sub-Saharan Africa, where domestic reporting often carries early information value.

Our final source universe was selected from a wider pool of global publications and reviewed country by country by Permutable’s economists and analysts. This process was designed to remove aggregators, identify relevant macroeconomic publications and strengthen domestic source coverage.

We believe this broader source base gives investors earlier visibility into local economic developments that may not yet be reflected in international reporting, consensus forecasts or market pricing.

One of the most important features of the Permutable Global Macro Sentiment Indices is the separation of domestic and international sentiment signals.

Rather than aggregating all news coverage into a single country score, GMSI maintains three views: domestic, international and combined.

The domestic view captures how a country is reporting on itself, often in local language and through local sources. The international view captures how the rest of the world is characterising that country’s macro risk.

The divergence between these layers can be particularly valuable. Domestic pressure may build before international coverage reacts, creating an early signal. Conversely, international coverage may overstate or misread local conditions, creating potential divergence between global perception and domestic reality.

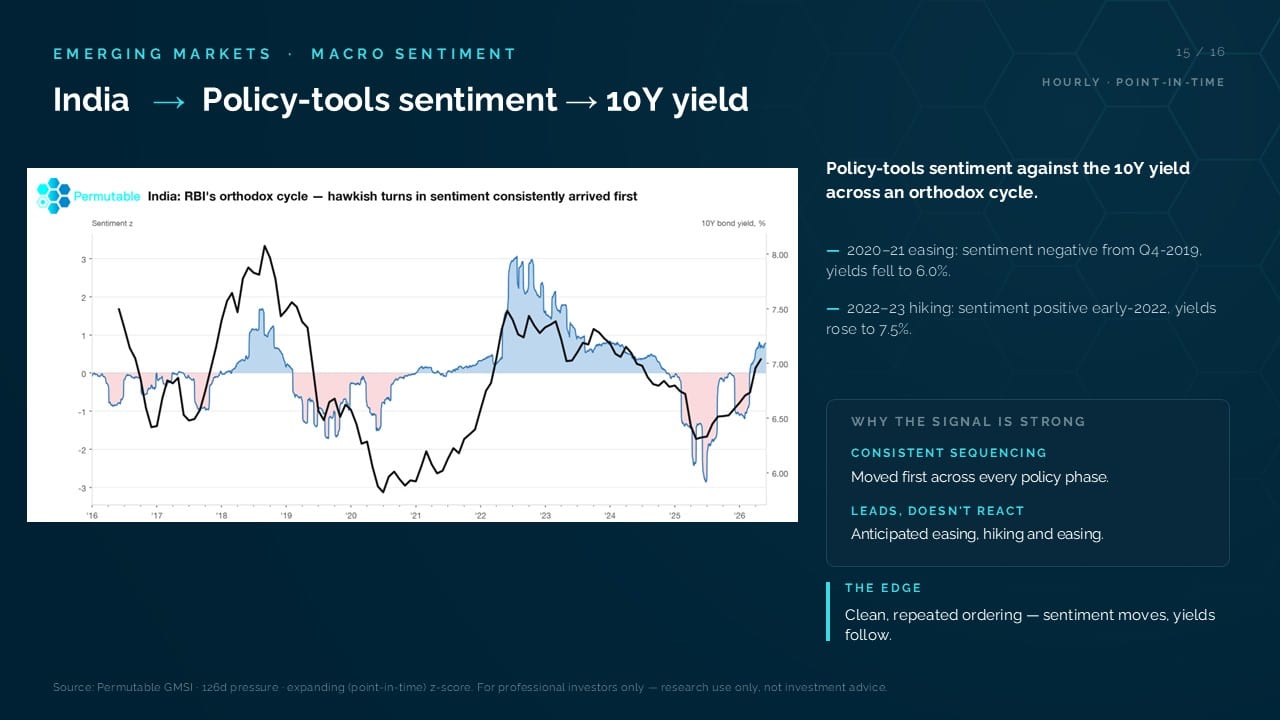

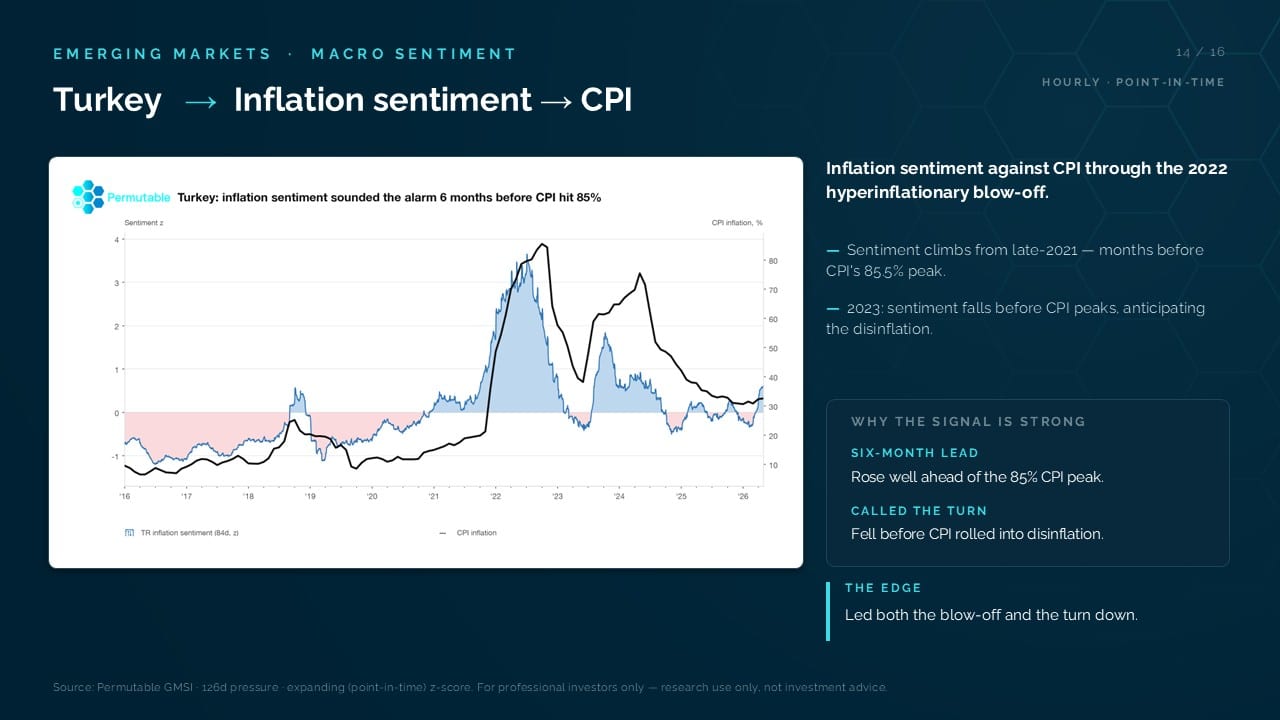

This distinction is especially relevant for emerging-market investors, sovereign-risk analysts, FX teams and macro strategists. Local inflation pressure, fiscal strain or policy credibility concerns may appear domestically before they become visible to global desks. International narratives may then amplify those risks once they become relevant for FX, rates, commodities or sovereign spreads.

GMSI has been constructed for point-in-time use, supporting historical analysis, backtesting, model development and signal validation without look-ahead bias.

For discretionary macro teams, the dataset provides a structured view of how narratives evolved before major inflation, policy, FX or sovereign-risk shifts. For systematic researchers and quantitative investors, it provides machine-readable macro sentiment data that can be tested, transformed and integrated into existing research pipelines.

“Quantitative investment teams are increasingly looking beyond traditional datasets to identify differentiated sources of signal generation and risk insight,” said Michael Brisley, Chief Commercial Officer at Permutable.

“The value is not simply measuring sentiment. It is giving macro and systematic teams a testable signal for when inflation, policy, FX or fiscal narratives are becoming persistent enough to influence markets.”

“What makes GMSI different is the combination of thematic depth, geographic breadth, point-in-time construction and the ability to separate domestic and international narratives. Investors want to understand how macroeconomic pressure forms, travels and becomes relevant for markets.”

The Permutable Global Macro Sentiment Indices have been built for institutional teams that need to monitor macro pressure across countries, themes and asset classes, using the same award-winning infrastructure which recently saw Permutable named as Technology Provider of The Year: Innovation by Hedgeweek.

For macro portfolio managers and strategists, the indices can help track intensifying or easing narratives by country and topic. For FX and rates desks, they can help monitor policy and inflation turns, as well as domestic-versus-international divergence. For economists and forecasters, GMSI provides a point-in-time text signal to support nowcasting and forecasting work. For systematic teams, it provides an orthogonal feature set for model development, signal testing and cross-country comparison.

Core applications include:

Permutable Global Macro Sentiment Indices are available immediately to institutional clients through:

We also support access to ready-made hourly indices and underlying headline-level data for teams that require custom aggregation. Additional institutional delivery integrations are expected to follow.

As information plays an increasingly important role in market formation, we believe the ability to systematically measure macroeconomic narratives will become a core component of modern investment research, risk management and systematic macro workflows.

See how macro pressure forms, travels and diverges before it reaches official data or market consensus. Request a walkthrough, test sample signals or speak to our team about API, Excel and custom index delivery. Contact enquiries@permutable.ai or book a demo.

The Permutable Global Macro Sentiment Indices are machine-readable macro sentiment indicators designed to track how inflation, growth, monetary policy, fiscal risk, trade, labour markets, FX vulnerability and geopolitical risk are evolving across global information sources.

GMSI is built for institutional investors, macro strategists, EM desks, FX and rates teams, sovereign-risk analysts, economists, systematic researchers and quantitative investment teams that need structured macro sentiment data for research, trading and risk workflows.

How are the Permutable Global Macro Sentiment Indices different from traditional macro data?

Traditional macro data is usually released after economic activity has already occurred. GMSI tracks the information environment forming around those economic conditions in real time, helping investors identify when the macro narrative is changing before official data confirms the move.

GMSI is designed specifically for macroeconomic signal extraction. It classifies overlapping macro themes, separates directional and semantic sentiment, and distinguishes domestic narratives from international perception rather than reducing news coverage to a single generic sentiment score.

Domestic sources may show inflation stress, policy credibility concerns or fiscal pressure before international coverage reacts. International sources may then amplify those risks once they become relevant for FX, rates or sovereign spreads. Separating these layers helps investors understand how local pressure becomes global market risk.

Yes. GMSI is constructed on a point-in-time basis, which supports historical analysis, backtesting, model development and signal validation without look-ahead bias.

GMSI covers 90+ countries, 70+ macro indicators, 250,000 curated sources and 80+ languages, with coverage across developed, emerging and frontier markets.

Institutional teams can access GMSI through API delivery, Excel integration, enterprise data feeds, real-time monitoring capabilities and historical point-in-time datasets for research and backtesting.

Analysis

30 Jul 2026

US growth and policy outlook Q2 2026: Q2 bought the Fed time. July may take it back

Read more >

Analysis

29 Jul 2026

South Korea economy: the chip windfall is outrunning domestic growth

Read more >

27 Jul 2026

The tide turns on Russia inflation outlook as drone strikes spread from refineries to warehouses

Read more >