Japan’s economy at a crossroads: Political risk, bond market stress, and the Yen’s decline

17 Jul 2025

17 Jul 2025

In this article, we explore Japan’s growing macro fragility as political uncertainty, surging bond yields, and a structurally weaker yen reshape investor sentiment. With JGB yields at multi-decade highs and the yen hitting record lows against major currencies, markets are undergoing a decisive re-pricing of risk. Amid this volatility, our Trading Co-Pilot has been able cut through the noise, identify turning points, and stay ahead of shifting macro trends.

In recent weeks, Japan’s economy and financial markets have entered a volatile phase, marked by a broad re-pricing of sovereign risk, mounting political uncertainty, and currency realignments across the board. Japanese Government bonds (JGBs) from 2-year to 30-year, have seen yields soar to levels not seen since the late 1990s, while the yen has collapsed to multi-decade lows against the euro, dollar, and Swiss franc. Against this backdrop, our Trading Co-Pilot has remained an essential lens through which investors can detect signals from noise, capturing inflection points, anticipating macro shifts, and providing confidence amid complexity.

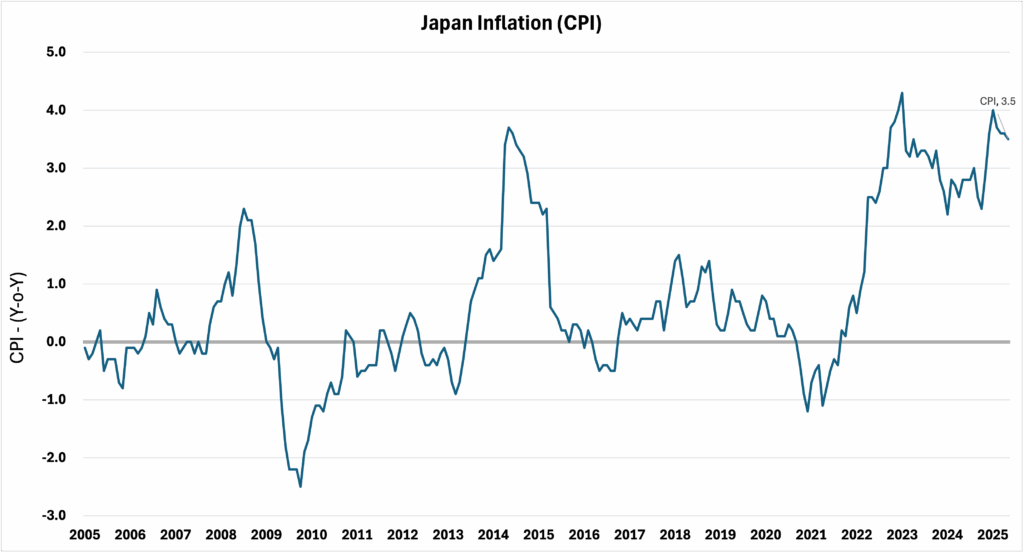

Japan’s inflation picture is diverging from historic norms. Headline inflation softened to 3.5% in May, its lowest reading since November, driven by slower price increases in healthcare, clothing, and household goods. However, the Bank of Japan’s (BoJ) preferred core inflation metric accelerated to 3.7%, its highest in over two years, reflecting structural price stickiness. Adding to the inflation woes is the doubling of rice prices, which has demonstrated the limitations of state subsidies in shielding households from food-driven price shocks.

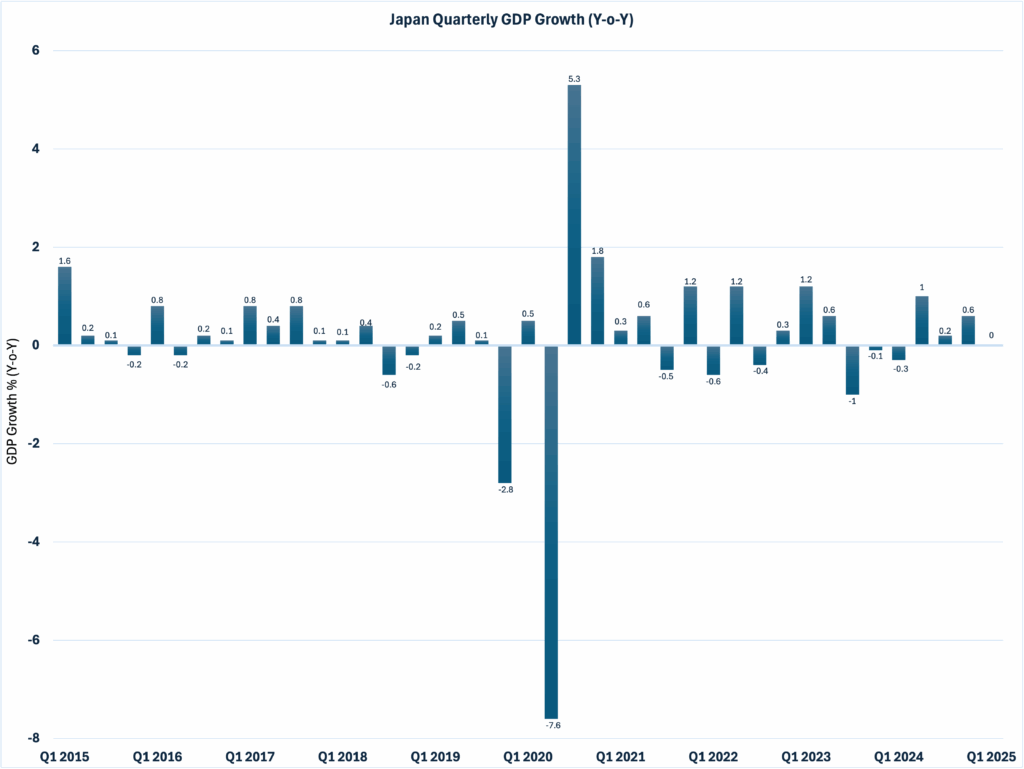

This presents a fundamental puzzle for the BoJ and reflects the broader uncertainty hanging over Japan’s economy. Having delivered its first interest rate hike in 17 years earlier in 2025, the BoJ opted to pause in June and to taper its bond issuance programme. Despite a string of weak GDP prints and flagging real wages, inflationary dynamics rooted in cost-push pressures, tariff-induced distortions, and wage trends suggest an undertone of fragility and persistent underlying price pressure. Growth remains subdued across Japan’s economy, with Q1 GDP flat and exporters challenged by a weakening yen and intensifying trade headwinds as Trump set a 25% tariff on Japanese imports. The political imperative, specifically looking ahead to the 20th July Upper House election, only raises the stakes.

In the absence of any new inflationary surprise, further monetary tightening is likely to be delayed until Q4 at the earliest. What we’re witnessing for policy in both a fiscal and monetary sense, is a balancing act whereby institutions are navigating a tightrope of inflation becoming too entrenched to dismiss, coupled with a subdued growth outlook too precarious to risk throwing off balance.

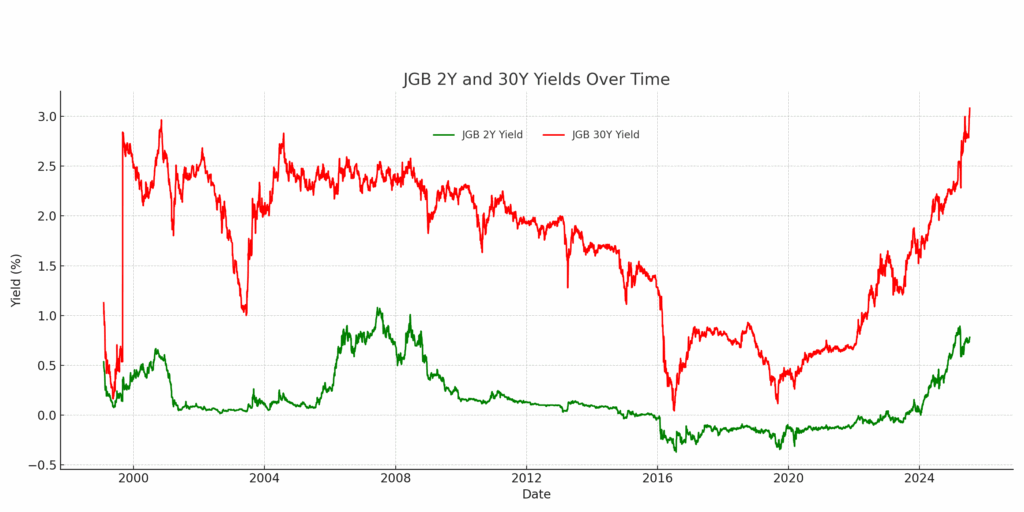

Japanese Government Bond yields have surged recently, signalling both structural unease and tactical repricing owing to mounting risk premiums. The 10-year yield has breached 1.55%, its highest level since March, and now teeters on the edge of a breaking higher above 1.6%, a level not seen since 2007. Meanwhile, the longer term bonds, notably the 30-year yield, have climbed past 3.2%, while the 20-year touched highs not seen since 1999.

This vertical repricing reveals a market bracing for fiscal slippage across Japan’s economy. With opposition parties campaigning on large-scale stimulus and potential tax cuts, the market fears a breakdown of fiscal discipline. Indeed, the Ministry of Finance’s earlier attempt to cap yields through bond issuance cuts proved short-lived and offered sparse relief. The chart reflects how JGB yields (both 2Y and 30Y) are now diverging from traditional norms, even as the yen weakens. This unusual dynamic underscores the risk premium now being priced into Japanese assets.

Our Trading Co-Pilot’s currency and political sentiment components have been leading indicators of this dislocation, signalling stress as early as June. The spread between the 2-year and 30-year JGB yields has widened dramatically, hinting investor discomfort.

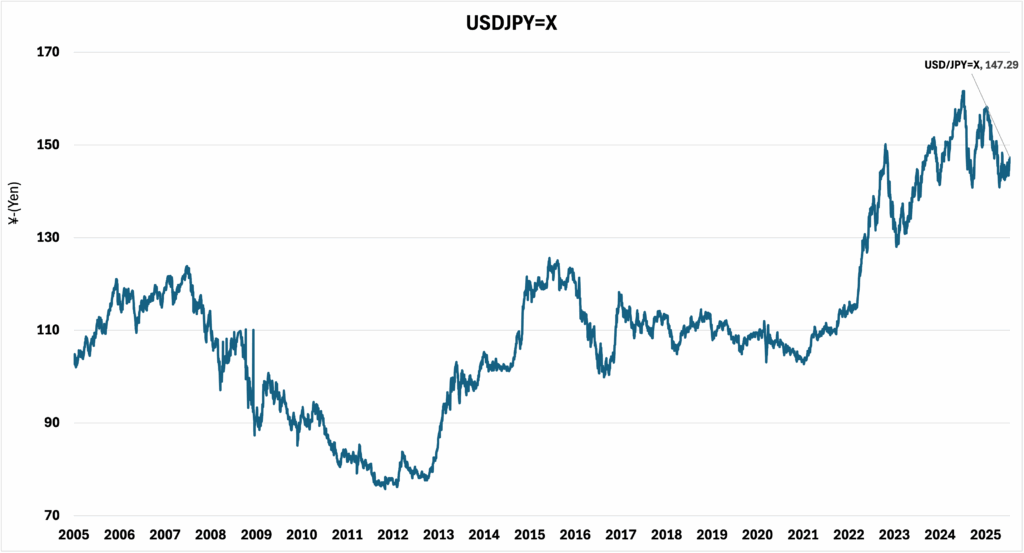

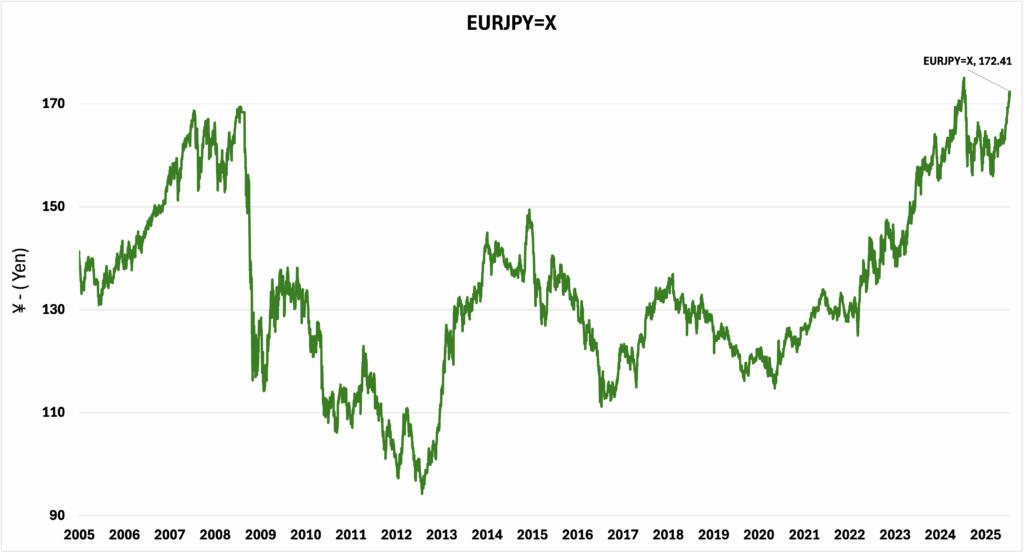

Despite the surge in JGB yields, the yen has continued to slide. USD/JPY has pushed above ¥147.00, closing in on cycle highs. Even more striking is the EUR/JPY cross, which hit a one-year high of ¥172.63, driven by euro strength and Japanese political risk. The yen’s underperformance reflects not just interest rate differentials, but also doubts over Japan’s fiscal trajectory, weak domestic demand, and the BoJ’s caution to commit to a sustained hiking cycle.

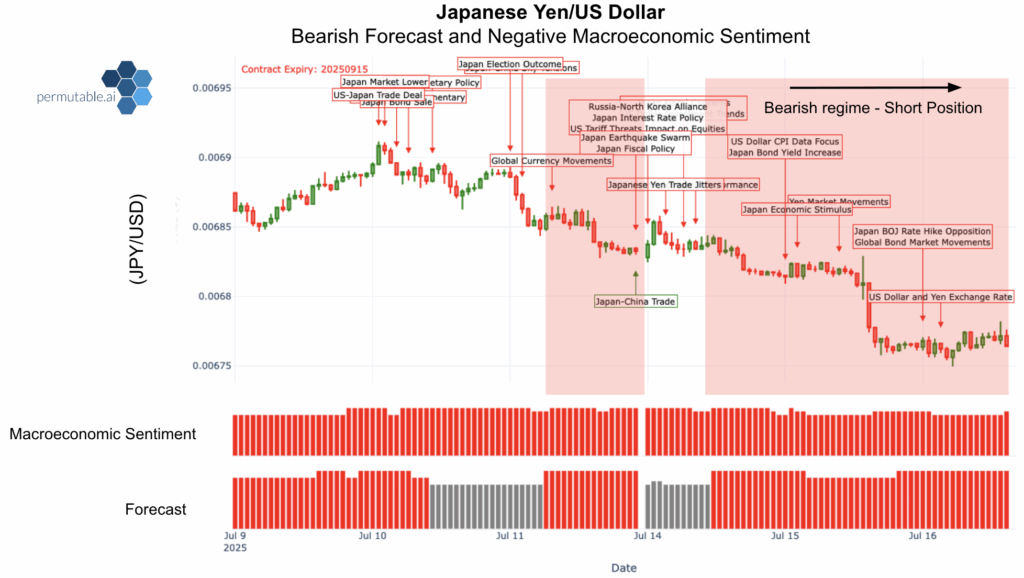

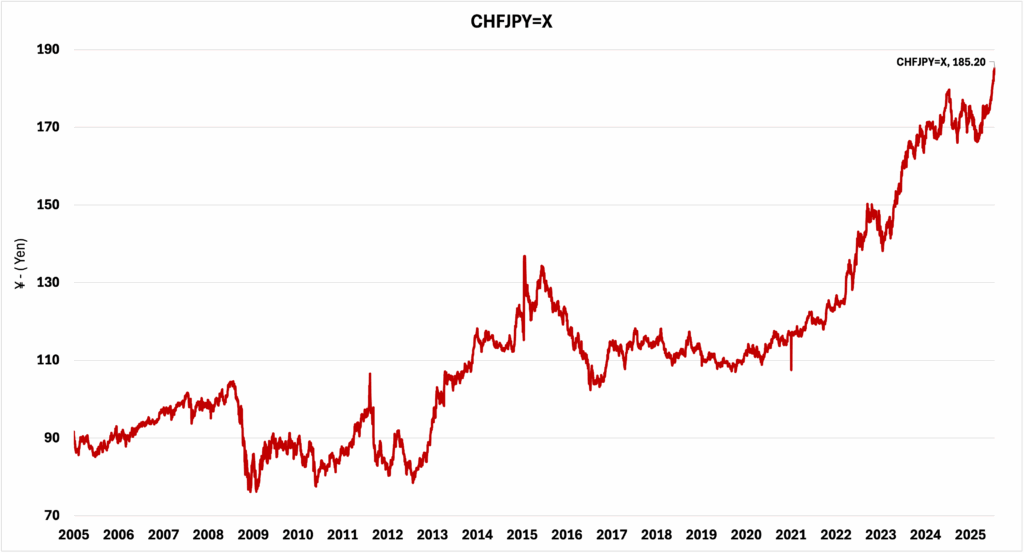

CHF/JPY offers another lens into safe haven divergence. Despite global risk-off sentiment, the Yen is no longer acting as a defensive asset. CHF/JPY recently surged to ¥185.30, in line with our Trading Co-Pilot headlines showing positive momentum in the Swiss economy, while Japan’s economy registered negative scores across nearly all categories, fiscal, political, and economic. The chart below shows the bearish outlook for the Yen, with macroeconomic and forecast sentiment turning pessimistic over the last week. Therefore, for investors to gain more confidence and the Yen to retain its defensive stature, the BoJ must look to signal a more hawkish stance or policymakers must allude to greater fiscal credibility which is difficult during election periods as parties look to appeal to voters.

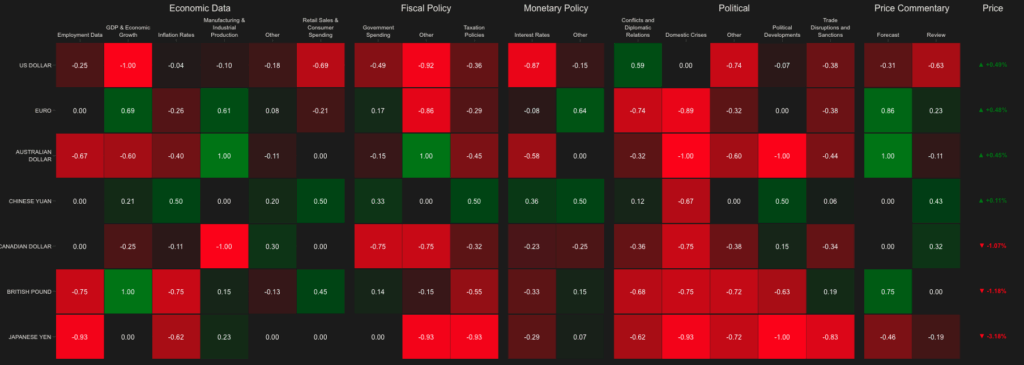

As highlighted in our FX sectoral heat-map, the Yen ranks as the weakest among major currencies. Negative sentiment spans across political developments (-1.00), employment data, fiscal policy, taxation, domestic crisis, at (-0.93), trade disruptions and sanctions (-0.83), inflation (-0.62), and interest rates (-0.29). This rare pattern of cross sector weakness explains the currency’s inability to benefit from yield rises or global volatility, conditions that historically supported the Yen.

The pair has surged to multi-week high of ¥147.00, as U.S. yields rose and Japanese yields repriced risk. Co-Pilot’s forecasts turned bullish on USD/JPY as early as July 9, correctly identifying the widening yield differentials and safe-haven premium for the dollar amid global tariff threats. The pair similarly reflects investor pessimism in the Japanese economy, showing strong negative sentiment with GDP growth (-0.80), interest rates (-0.77), and QE measures (-1.00), suggesting the market views Japanese tightening as tentative and insufficient given the fragility of Japan’s economy. In contrast, the dollar retains its policy momentum despite its own domestic challenges.

Recently soaring to a one-year high of ¥172.63, driven not just by Japanese weakness but eurozone resilience. Our Trading Co-Pilot’s EUR sentiment index pointed to continued investor rotation into euro assets due to comparative political stability and a hawkish-leaning ECB. EUR/JPY, is benefitting from a favourable eurozone backdrop. Modest economic resilience, improving inflation data, and political cohesion has benefitted rotation into the single currency. Even with EUR-based political frictions, the relative perception of stability keeps the Euro bid in JPY crosses.

The safe haven status of Swiss Franc has emerged as one of the most notable FX pivots. The pair has extended its longstanding uptrend, hitting highs near ¥185.30, supported by the Swiss franc’s classic safe-haven bid and deep investor scepticism toward Japan’s economy and its ability to contain fiscal slippage and recent geo-political shocks. The Franc is still regarded as the highest-quality safe haven across dimensions, with the yen losing its historical defensive status. The FX performance shows this clearly that CHF/JPY is now testing all-time highs even as JGBs rally, implying that market confidence in Japan’s policy coordination is fraying.

Looking ahead, Japan’s fiscal outlook and the Upper House election result will be pivotal. If the ruling coalition loses its majority, markets may brace for aggressive stimulus proposals, raising the spectre of debt monetisation. However, a divided opposition and legislative hurdles make immediate fiscal expansion less likely. It remains to be seen whether the current political noise will sustain uncertainty in bond markets, capping the Yen on the upside.

For investors, Japan’s economy is no longer the low-risk, low-return anchor that it once was. Yields are rising, but not for the right reasons. Currency weakness appears structurally inherent and not a tactical play. The bigger picture at hand sees the BoJ being boxed in by confluence of above target inflation and lacklustre growth. This is coupled by the emergence of political risk returning to Tokyo complicating matters of fiscal orthodoxy and raising the guard of bond vigilantes.

In this environment, our Trading Co-Pilot remains a vital tool for institutional decision-making. By aggregating sentiment across sectors and policy domains, being able to track structural divergences in real time enables faster rebalancing across FX strategies. As Japan’s economy edges towards its policy reckoning, we’ll be watching the headlines, and signalling ahead of the turn.

Stay ahead of structural dislocations and policy uncertainty with our real-time macro intelligence. Our plug and play Trading Co-Pilot intelligence suite empowers clients to anticipate turning points across FX and fixed income, before the market prices them in.

To access our full dashboards, strategy tools, or schedule a demo, simply email: enquiries@permutable.ai

A: It measures real-time sentiment across political, fiscal, monetary, and trade domains, highlighting how shifts in narrative and investor confidence shape Japan’s bond and currency markets.

A: This unusual divergence reflects structural concerns about Japan’s fiscal trajectory and doubts over the Bank of Japan’s commitment to sustained tightening. Rising yields are driven by risk premiums, not stronger fundamentals, while the yen’s safe-haven appeal has eroded.

A: Leadership uncertainty, election-driven fiscal promises, and tensions with trading partners amplify volatility. These political risks reduce confidence in fiscal discipline, contributing to both rising yields and yen weakness.

A: The yen has lost ground as a traditional defensive currency. Crosses such as CHF/JPY show investors increasingly prefer the Swiss franc, reflecting waning trust in Japan’s policy coordination during periods of global stress.

A: Institutional clients can integrate the sentiment data into FX and fixed-income strategies to anticipate turning points. It helps flag credibility risks, track divergence between yields and currencies, and identify structural dislocations before they manifest in price action.

Analysis

04 Aug 2026

Global industrial production sentiment: Canada, India and South Korea Gain as the UK, Germany and China weaken

Read more >

Analysis

30 Jul 2026

US growth and policy outlook Q2 2026: Q2 bought the Fed time. July may take it back

Read more >

Analysis

29 Jul 2026

South Korea economy: the chip windfall is outrunning domestic growth

Read more >