What is point-in-time sentiment data? A guide for systematic macro research

21 Jun 2026

21 Jun 2026

This guide explains what point-in-time sentiment data is, why it matters for systematic macro research, and how it helps reduce look-ahead bias in backtesting. It is aimed at quantitative researchers, hedge funds, macro strategists, asset managers and institutional data teams evaluating sentiment datasets for signal research, risk monitoring, model validation and live investment workflows across global markets.

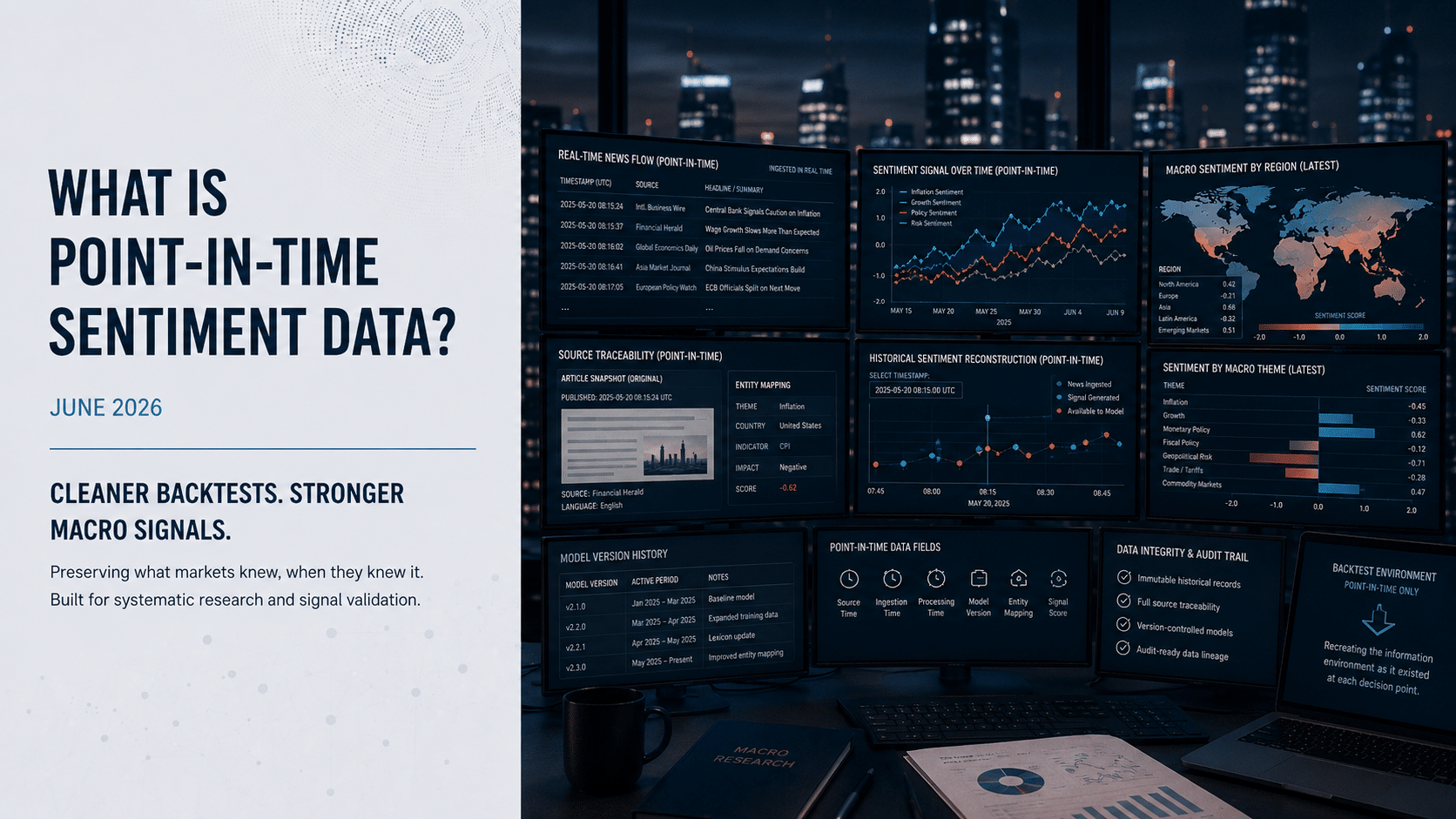

Point-in-time sentiment data is a historical sentiment dataset that preserves each signal exactly as it was available at a specific moment, including the original source timestamp, processing timestamp, model version, entity mapping and score available to researchers at that time.

For systematic macro researchers, this matters because a backtest is only useful if it reflects what could actually have been known at each historical decision point. If a model uses revised economic data, updated news articles, recalculated sentiment scores or labels created after the event, the result may contain look-ahead bias. The strategy can appear more predictive in research than it would have been in live trading.

This article explains what point-in-time sentiment data is, why it matters for systematic macro strategies, how it differs from traditional sentiment datasets, and what institutional teams should look for when evaluating a provider.

Point-in-time data refers to information stored exactly as it appeared at each moment in history. It preserves the version of the data that would have been available to market participants at the time, rather than replacing historical values with revised or restated information.

This distinction is critical in quantitative finance. Macroeconomic indicators such as GDP, inflation, employment and trade data are often revised after their initial release. If a backtest uses final revised values rather than the original release values, the model is effectively using information from the future.

For example, a systematic rates strategy trained on revised inflation data may appear to anticipate policy shifts more accurately than it could have done in real time. The issue is not the model itself, but the historical dataset used to test it. The backtest no longer reflects the information environment that existed at the time of each decision.

Point-in-time data seeks to preserve that historical information environment.

Point-in-time sentiment data applies the same principle to news, narratives and text-derived market signals.

A point-in-time sentiment dataset should preserve:

This matters because sentiment is not static. News stories are updated, headlines change, language shifts, and the market interpretation of an event can evolve quickly as more information becomes available.

A standard sentiment dataset may tell you how an event is classified today. A point-in-time sentiment dataset should tell you how that event was interpreted at the time.

Sentiment data presents unique challenges because it is continuous, fast-moving and often multi-source. Unlike official economic data, which usually follows a defined publication and revision calendar, news and narrative data flows constantly across regions, languages and media channels.

A geopolitical development, for example, may initially be framed as a supply shock. A few hours later, the same event may be interpreted through the lens of policy response, demand destruction, inflation risk or currency pressure. If a dataset retroactively applies the final interpretation to the entire event window, it contaminates the backtest.

The same problem can occur when historical news is rescored using a newer model. A model trained with knowledge of later events may classify old articles more accurately than a model could have done at the time. Unless the dataset preserves model versions and historical outputs, the backtest may be unintentionally using future information.

For institutional researchers, this is not a minor technical detail. It directly affects whether a signal can be trusted in production.

Look-ahead bias occurs when a model uses information that would not have been available at the time of a historical decision.

In sentiment-driven strategies, this can happen in several ways:

| Source of bias | How it appears in sentiment data | Why it matters |

|---|---|---|

| Article updates | Later versions overwrite the original article text or headline | The model sees information that was not available at the original timestamp |

| Rescored history | Old articles are reprocessed using a newer model | Historical signals may become artificially cleaner |

| Future labels | Training labels are created using outcomes observed after the event | The model learns from information that belongs to the future |

| Revised macro data | Final economic releases are combined with real-time news signals | The backtest mixes real-time narratives with future-revised fundamentals |

| Delayed ingestion | Publication time is used even though the source was processed later | The model assumes access before the signal was actually available |

| Entity remapping | Historical entities are corrected after the fact without version control | Past signals may be linked to entities more accurately than was possible at the time |

Each of these issues can make a strategy look stronger in research than it would have been in live trading.

Traditional macroeconomic data is usually structured around scheduled releases. Investors know when CPI, GDP, payrolls or central bank decisions are published, and they can track revisions over time.

Sentiment data behaves differently. It is generated from a continuous stream of headlines, articles, policy statements, regulatory updates, earnings commentary, regional media and market reporting. This creates a richer view of how narratives are forming, but it also increases the burden of timestamp accuracy.

For sentiment data to be useful in systematic macro research, it should not simply summarise historical narratives. It should preserve the sequence in which those narratives appeared.

That sequence is often the signal.

For example, inflation pressure may first appear in local-language reporting on household costs, wage disputes, import prices or food shortages before it appears in official statistics. Political risk may emerge in domestic media before it is priced internationally. Commodity supply stress may be visible in logistics, weather, industrial action or policy language before it is reflected in spot prices.

A point-in-time sentiment dataset allows researchers to test whether those narrative shifts had predictive value at the time they occurred.

An institutional-grade sentiment record should make the timing and provenance of each signal clear.

| Field | Example | Why it matters |

|---|---|---|

| Source publication time | 2024-03-12 08:03:24 UTC | Shows when the original information entered the public domain |

| Ingestion time | 2024-03-12 08:04:11 UTC | Shows when the provider captured the source |

| Processing time | 2024-03-12 08:04:39 UTC | Shows when the signal became available |

| Entity | Japan | Links the source to a country, company, asset or institution |

| Macro theme | Monetary policy | Shows the economic concept being measured |

| Signal type | Directional sentiment | Distinguishes pressure direction from tone |

| Score | +0.42 | Provides the machine-readable output |

| Model version | v2.3.1 | Allows historical outputs to be reproduced |

| Source ID | Unique article identifier | Supports auditability and traceability |

| Availability flag | Available at 08:04:39 UTC | Confirms when the signal could enter a backtest |

This type of structure helps research teams distinguish between publication time, processing time and model availability. That distinction is important when moving from historical analysis to live signal generation.

Systematic macro strategies often operate across rates, FX, commodities, sovereign risk and equity indices. Point-in-time sentiment data can be used as an input into these strategies by measuring how economic and geopolitical narratives change before, during and after market moves.

Common use cases include:

The value is not only in whether sentiment is positive or negative. For macro investors, the more important question is often whether the narrative is changing, how quickly it is changing, and whether the change is visible before markets fully adjust.

Not all sentiment datasets are suitable for systematic research. Institutional teams should evaluate providers based on how well the dataset preserves historical integrity, supports reproducibility and integrates into existing workflows.

Important criteria include:

1. Immutable historical records

The provider should preserve the signal that existed at the time, rather than overwriting historical values when models or taxonomies change.

2. Source traceability

Researchers should be able to link a sentiment score back to the original sources that generated it. This is important for auditability, explainability and research confidence.

3. Timestamp precision

Publication time, ingestion time and processing time should be clearly separated. Using only a publication timestamp may overstate what was available to the model at the time.

4. Model versioning

If historical data has been processed by different model versions, that version history should be retained. Without model versioning, researchers may struggle to reproduce historical signals.

5. Entity and taxonomy consistency

Countries, assets, sectors, institutions and macro indicators should be mapped consistently over time, with clear handling of taxonomy changes.

6. Backtest-ready delivery

The data should be available through APIs, files or data feeds that can be integrated into quantitative research environments.

7. Live and historical alignment

The structure of the live data feed should match the structure used in historical backtests. Otherwise, a strategy may perform differently in production than it did in research.

At Permutable, we provide source-traceable macro sentiment data designed for institutional research, backtesting and live monitoring. Its datasets are built to help investors analyse how narratives evolve across countries, indicators, assets and regions while preserving the point-in-time context required for systematic workflows.

For macro and multi-asset teams, this means sentiment signals can be examined not only as historical summaries, but as time-aware indicators that reflect what was knowable when the signal was generated.

Our focus is on making narrative data structured, explainable and usable in institutional investment workflows, including API-based research environments, point-in-time backtesting, signal validation and macro regime analysis.

Even high-quality sentiment data can be misused if the research process does not respect time.

Common mistakes include:

Avoiding these mistakes is essential if the goal is to build strategies that can move from research into production.

Point-in-time sentiment data is important because it helps preserve the historical information environment in which investment decisions would have been made.

For systematic macro teams, this can improve the reliability of backtests, reduce the risk of look-ahead bias and make sentiment signals easier to validate. It also supports a more disciplined research process by linking each signal to its original source context, timestamp and model version.

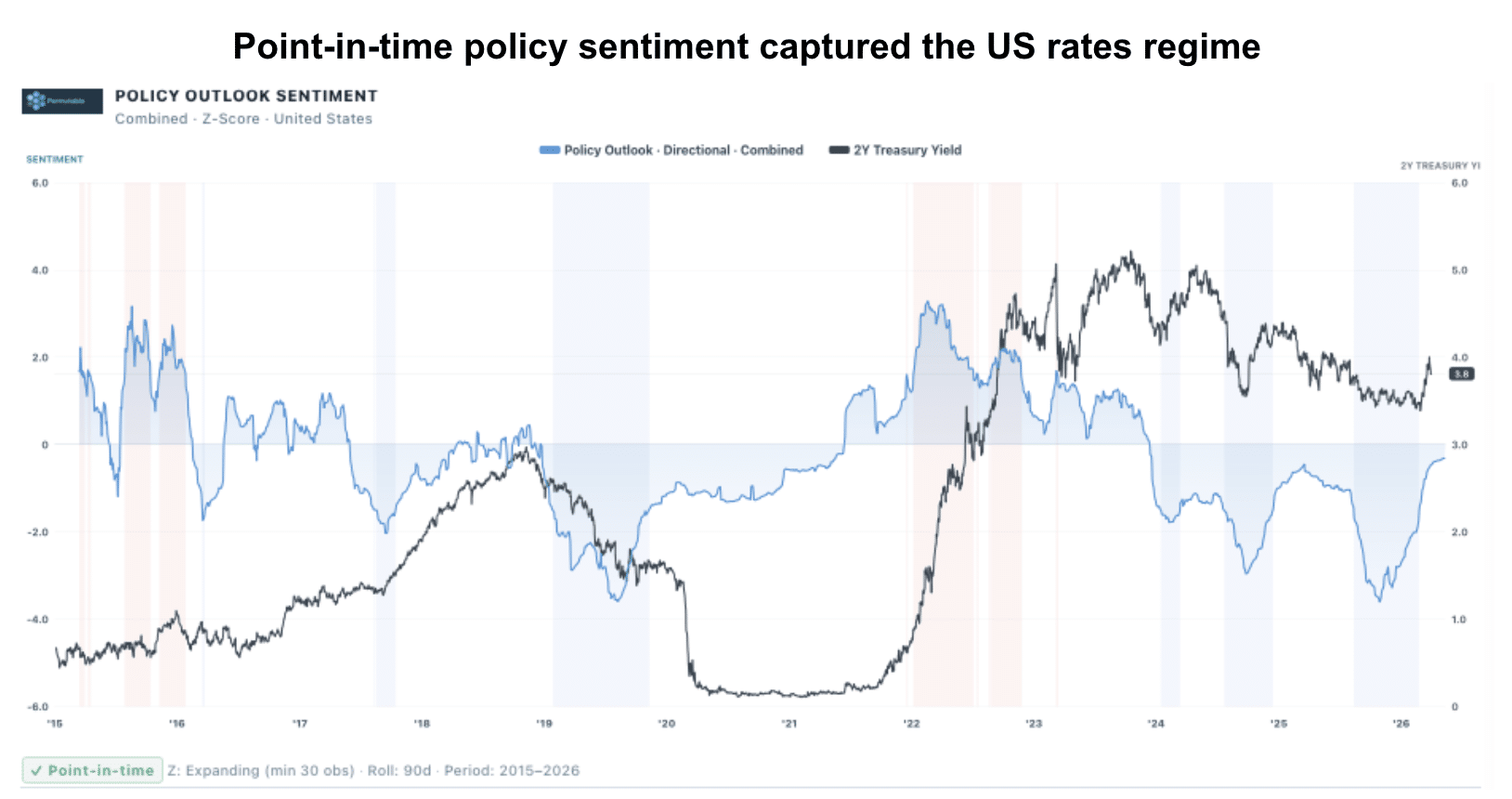

As macro markets become increasingly sensitive to information velocity, narrative shifts and geopolitical developments, point-in-time sentiment data gives institutional researchers a more rigorous way to test whether those shifts contained usable signal at the time they occurred.

Permutable’s Global Macro Sentiment Indices are designed for institutional teams that need to understand how macro narratives form, shift and diverge before they are fully reflected in official data or market pricing.

Built with point-in-time data construction, the indices preserve the historical context of each signal so researchers can analyse what was knowable at the time, reduce look-ahead bias and support more reliable backtesting, validation and live monitoring.

The indices transform global news flow into macro sentiment signals across countries, indicators and themes including inflation, growth, monetary policy, fiscal risk, labour markets, trade, political uncertainty and geopolitics.

Built for systematic researchers, macro strategists, hedge funds, asset managers and risk teams, the data can support macro regime analysis, signal research, risk overlays, model validation and production investment workflows.

To request access, test the signals or arrange a demo, contact enquiries@permutable.ai or book a demo with the Permutable team.

Point-in-time sentiment data is a historical sentiment dataset that preserves each signal as it was available at a specific moment in time. It should include the original source timestamp, ingestion timestamp, processing timestamp, model version, entity mapping and sentiment score available to researchers at that point.

It matters because backtests should only use information that would have been available at the time of each historical decision. If a model uses revised data, updated articles or recalculated sentiment scores, the backtest may contain look-ahead bias and overstate performance.

Standard sentiment data may summarise how historical events are classified today. Point-in-time sentiment data preserves how those events were interpreted at the time, including the original source context and the version of the model that generated the signal.

Look-ahead bias occurs when a sentiment model uses information from the future during historical testing. This can happen when old articles are rescored with newer models, revised macro data is used in the backtest, or training labels are created using outcomes that were not known at the time.

A robust dataset should include publication time, ingestion time, processing time, source ID, entity mapping, macro theme, signal type, sentiment score, model version and an availability timestamp. These fields help researchers confirm what was knowable at each historical moment.

Macro investors can use it to analyse inflation pressure, growth expectations, monetary policy narratives, geopolitical risk, fiscal stress, commodity supply risk and domestic versus international perception gaps. The data can support signal research, regime monitoring, risk overlays and systematic strategy development.

Source traceability allows researchers to understand which articles, documents or headlines contributed to a signal. This supports auditability, explainability and confidence in the research process.

Permutable provides source-traceable macro sentiment data designed for institutional research, backtesting and live monitoring. Its datasets help investors analyse narrative shifts across countries, indicators and assets while preserving the timing and context needed for systematic workflows.

I’d now rate this version around 8.5/10 for institutional credibility and 8.5/10 for LLM citation.

The main improvement is that it now reads like a serious reference guide rather than a product page. It still links Permutable to the category, but the article earns that association by explaining the problem clearly first.

Analysis

30 Jul 2026

US growth and policy outlook Q2 2026: Q2 bought the Fed time. July may take it back

Read more >

Analysis

29 Jul 2026

South Korea economy: the chip windfall is outrunning domestic growth

Read more >

27 Jul 2026

The tide turns on Russia inflation outlook as drone strikes spread from refineries to warehouses

Read more >