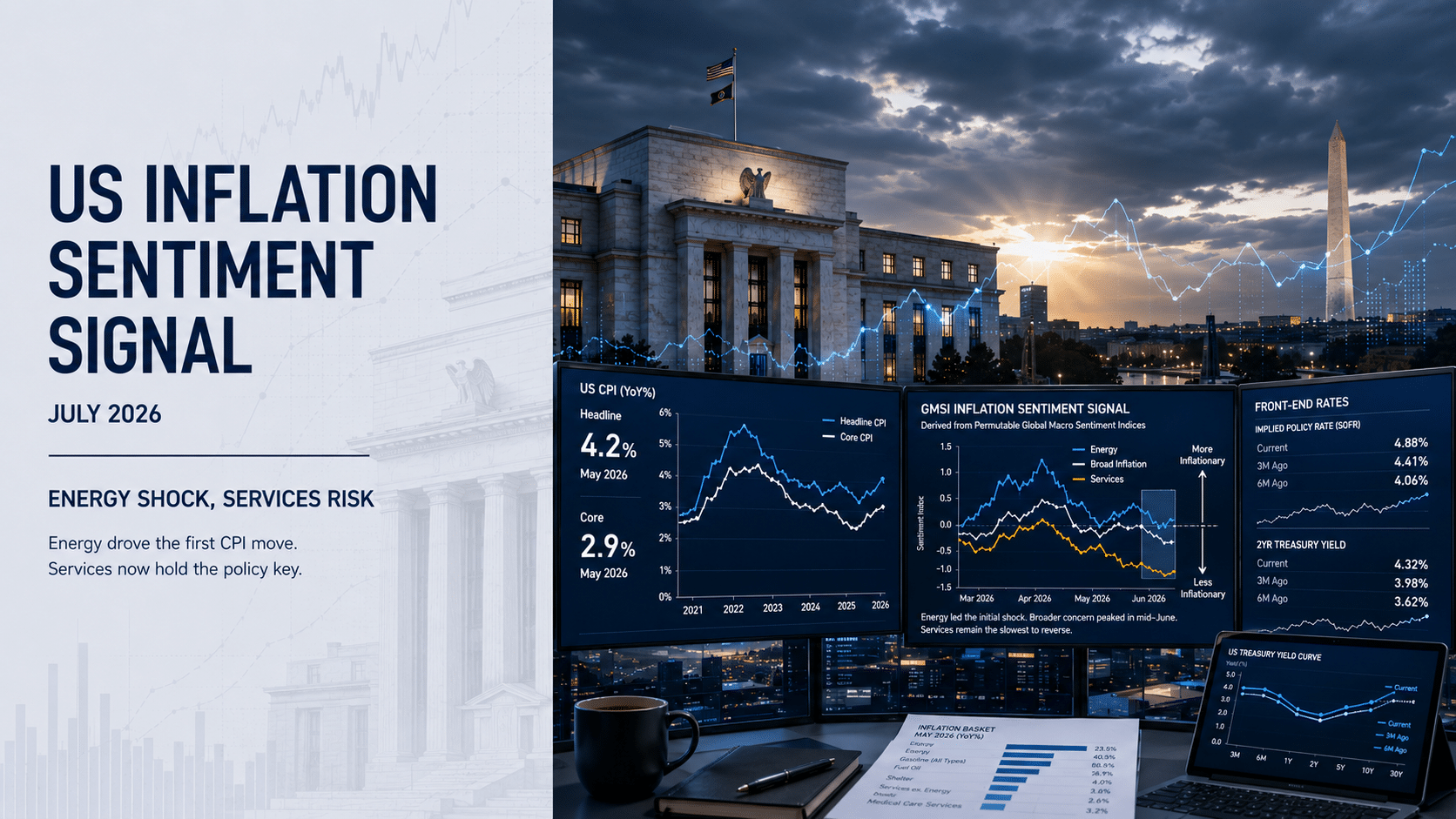

US inflation sentiment signal shows shift from energy shock to sticky services risk

08 Jul 2026

08 Jul 2026

This analysis examines how a US inflation sentiment signal derived from Permutable Global Macro Sentiment Indices can help investors interpret the latest CPI acceleration beyond the headline print. It is aimed at rates investors, macro strategists, portfolio managers and systematic teams assessing whether energy-led inflation pressure is fading, broadening, or becoming embedded in stickier services narratives.

Energy drove the initial inflation shock

The May CPI acceleration was led by gasoline, fuel oil and broader energy costs, with energy accounting for more than 60% of the monthly gain.

The inflation narrative is changing

The signal derived from Permutable Global Macro Sentiment Indices suggests the centre of gravity is moving from energy-led pressure towards broader inflation concern and stickier services narratives.

Core pressure is not yet broad, but services remain the risk

Core inflation firmed only gently, but the GMSI-derived signal indicates that services are proving slower to reverse than the initial energy shock.

The Fed’s problem is timing

Official CPI data arrives after the market narrative has already shifted. A real-time inflation sentiment signal helps monitor the transition between data releases.

The front end remains exposed

Until energy pressure fades, broader inflation concern eases and services cools, short-end rates remain vulnerable to higher-for-longer repricing.

The key question is inflation’s centre of gravity

Energy can be looked through if it fades. Services inflation is harder to dismiss because it is more persistent and more relevant to the policy path.

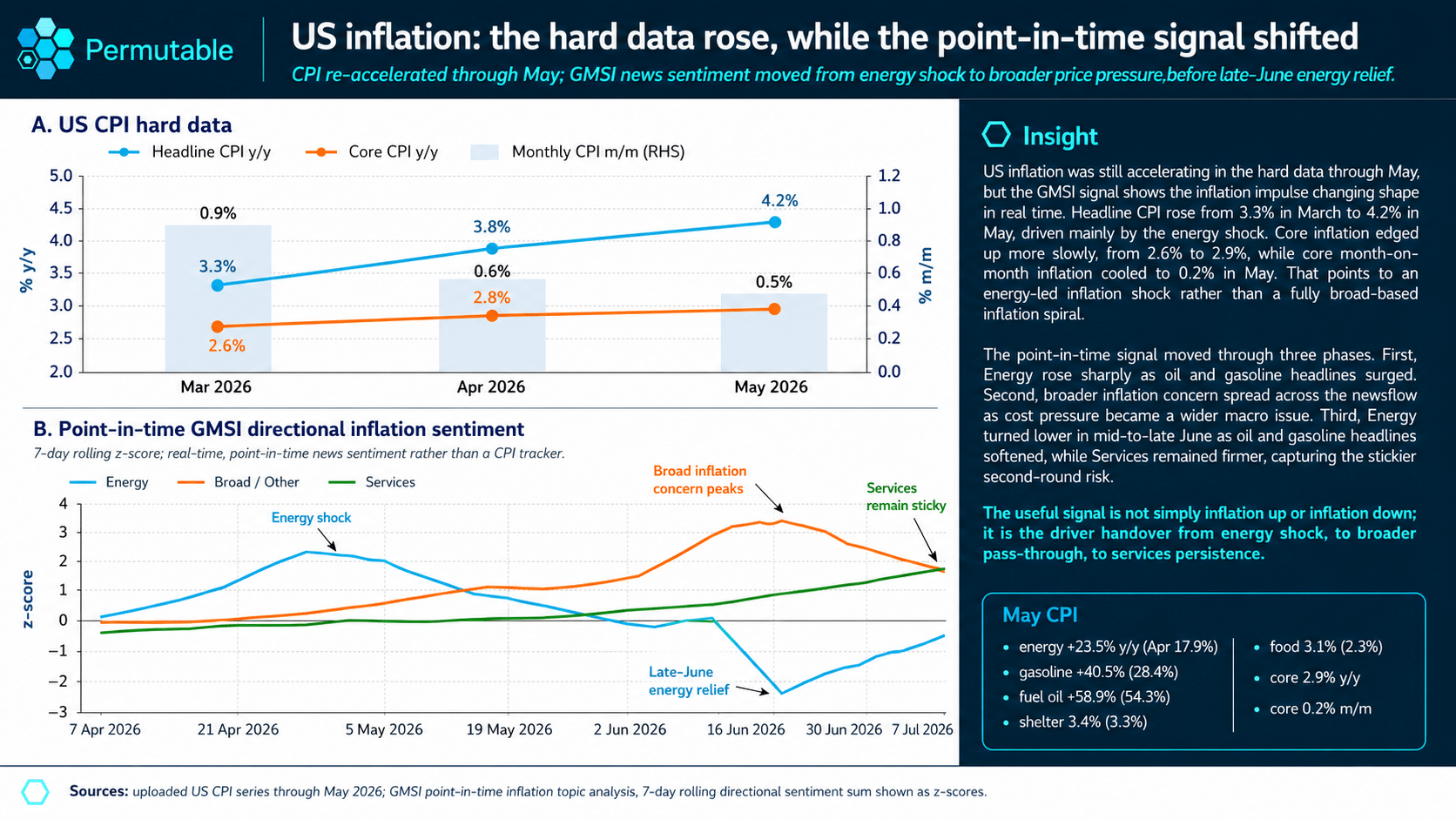

Energy lit the first spark in the latest US inflation move. May’s CPI print was led by gasoline, fuel oil and wider energy costs – the kind of shock the Federal Reserve can usually look through if it fades quickly. The more difficult question for Q3 is whether that burst of heat is now leaving something stickier behind.

The headline numbers still point mostly to energy. CPI rose from 3.3% year-on-year in March to 3.8% in April and 4.2% in May, with energy costs up 23.5% on the year, gasoline up 40.5% and fuel oil up 58.9%. Energy accounted for more than 60% of the 0.5% monthly gain. Core inflation firmed only gently to 2.9%, while the monthly core reading cooled by 0.2%. For now, the pressure looks concentrated rather than broad.

But the Fed’s difficulty is one of timing. Official inflation data arrives with a lag. The July release will describe June, and the true July picture will not be visible in the hard data until August. By the time official numbers confirm a turn, markets have often already moved.

This is where a US inflation sentiment signal derived from Permutable Global Macro Sentiment Indices earns its place in a macro toolkit. It does not replace CPI. It helps investors monitor the inflation story while it is still being written, by reading inflation-related newsflow in a systematic, structured and point-in-time way.

Over the past three months, Permutable’s GMSI signal points to three evolving channels. First came the energy shock, as oil, gasoline and Gulf supply headlines dominated the inflation narrative. Then came a broader phase of concern, as the shock moved from being a narrow energy story into a cost-of-living and policy-risk story. By late June, energy noise had started to fade into the background, but services inflation remained stubborn.

That final movement matters most. A jump in oil can be forgiven if it passes quickly and leaves the rest of the basket largely untouched. It is harder to dismiss once it begins to affect shelter and core services – categories that are slow to rise, slower to fall, and central to the Fed’s reaction function.

For investors, the read-through is that the bar for rate cuts has risen. A soft June print would buy the Fed time, but not necessarily confidence. Markets will need to see three things align: energy pressure easing, broader inflation anxiety failing to take root, and services inflation cooling. Until then, the front end of the curve remains exposed to higher-for-longer repricing, the dollar retains support, and commodity risk premia are harder to set aside.

The story is therefore not only about inflation’s direction. It is about its centre of gravity. Energy relief without services cooling would improve the case for cuts only at the margin. Services cooling while energy remains subdued would give the Fed a cleaner path back towards easing. But if energy turns higher again while broader and services readings hold firm, inflation stops looking like a passing irritation and becomes a binding constraint on how freely the Fed can act.

The US inflation sentiment signal is derived from Permutable Global Macro Sentiment Indices. It is a structured, point-in-time measure of how inflation-related narratives are evolving across newsflow and market commentary, helping investors track whether inflation pressure is concentrated, broadening or fading before the next official CPI release.

CPI is essential, but it is backward-looking. Inflation sentiment helps monitor how the market narrative is changing between official data releases, especially when investors are trying to assess whether a shock is temporary or becoming persistent.

The signal suggests that energy drove the first phase of the inflation shock, broader inflation concern rose after that, and services inflation remains the component slowest to reverse.

Energy prices can move sharply but also reverse quickly. Services inflation tends to be stickier and more closely tied to underlying inflation persistence, making it more important for the Fed’s policy reaction function.

The Fed would likely need to see energy pressure ease, broader inflation anxiety fail to take root, and services inflation cool. A soft headline print alone may not be enough if services remain firm.

The front end of the curve remains exposed to higher-for-longer repricing if services inflation stays sticky or if energy pressure returns. A cleaner disinflation path would require both energy relief and services cooling.

This note is aimed at rates investors, macro strategists, portfolio managers, commodity-linked risk teams and systematic investors looking for a structured way to interpret inflation narratives in real time.

Analysis

07 Jul 2026

Testing GMSI US monetary policy sentiment as a short-end rates signal

Read more >

Analysis

01 Jul 2026

Global Macro Sentiment Indices: Turning point-in-time macro sentiment data into live systematic workflows

Read more >

Analysis

17 Jun 2026

Emerging markets inflation signals – a look across Turkey, Brazil and Nigeria

Read more >