In this article, we examine the renewed turn in US inflation Q2, as April’s CPI print challenges the idea that disinflation is still moving comfortably in the right direction. The headline points to re-acceleration, but the composition is more awkward: an energy-led shock has reached the consumer basket while core inflation has also edged higher.

April’s CPI report showed what happens when an energy shock reaches the consumer basket.

Headline CPI rose 3.8% y-o-y, up from 3.3% in March, and increased 0.6% m-o-m. Energy did much of the work. The energy index rose 3.8% m-o-m and accounted for more than 40% of the monthly all-items increase. Gasoline rose 5.4% m-o-m and 28.4% y-o-y. Energy prices overall were 17.9% y-o-y.

The headline says inflation has re-accelerated. The detail says the shock is energy-led.

That does not make the report benign. Energy shocks can fade quickly, but they can also move through transport, utilities, freight, business costs and expectations. Once that happens, the Fed can no longer treat them as a petrol-price inconvenience.

Core inflation was not soft enough to offset the energy story either. Core CPI rose 0.4% m-o-m and 2.8% y-o-y. Shelter rose 0.6% m-o-m. Energy was the spark, but the underlying picture was not calm.

Analysts are not reading April as a classic overheating signal. The stronger view is that the US is facing an energy-led inflation shock at an awkward point in the policy cycle.

Reuters framed the print as a higher-than-expected inflation reading that reinforced expectations of the Fed remaining on hold for longer. Principal Asset Management made the policy risk clear: the Fed can usually look through energy shocks, but further pass-through into core inflation would argue for keeping rates steady through 2026, with the risk that easing slips into 2027.

That is the market point. April does not force a hike. It raises the evidence needed for a cut.

The Fed’s communication has already become more defensive. The labour market outlook looks more resilient, but the inflation outlook has worsened, partly because of the Iran war. The policy debate is no longer simply about when cuts begin. It is now about what would allow the Fed to cut without looking too relaxed on inflation.

CPI confirms the shock after the fact. Sentiment helps show whether the market is starting to organise around it.

That is the value of Permutable’s US inflation sentiment signal. It does not need to forecast every CPI print to be useful. Its role is to show whether inflation is becoming more prominent, persistent and market-relevant in the daily macro narrative.

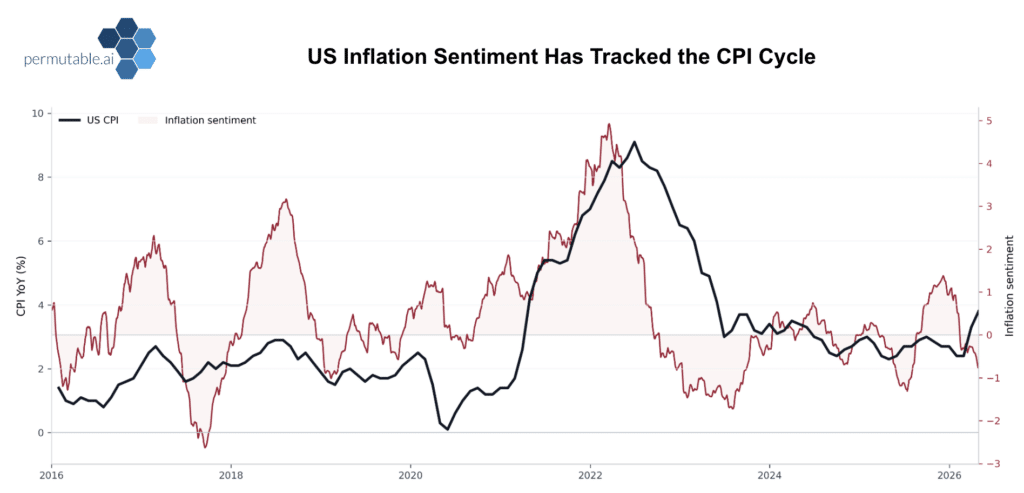

The historic chart gives context. Inflation sentiment tends to rise when inflation pressure becomes a dominant macro theme and fade when disinflation takes hold. It is not a replacement for CPI. It is a way of reading the pressure around CPI between official releases.

Energy inflation does not remain an oil-market story for long.

Higher gasoline prices hit households directly. Higher fuel and power costs raise costs for firms. Higher freight and transport costs feed into margins. Higher headline inflation complicates the Fed’s ability to guide markets towards easier policy.

The loop is straightforward: geopolitical tension lifts energy prices, energy lifts inflation, higher inflation narrows the Fed’s easing path, higher-for-longer rates support the dollar and tighten financial conditions.

What starts as a commodity shock becomes a rates and FX problem.

The producer-price data reinforce the concern. US wholesale inflation rose sharply in April, with energy costs adding pressure on companies and raising the risk of further pass-through to consumers. Producer prices rose 6.0% y-o-y, while PPI rose 1.4% m-o-m, with services, transport, warehousing and trade also contributing to the move.

CPI shows the shock reaching households. PPI suggests it is still moving through the corporate cost base.

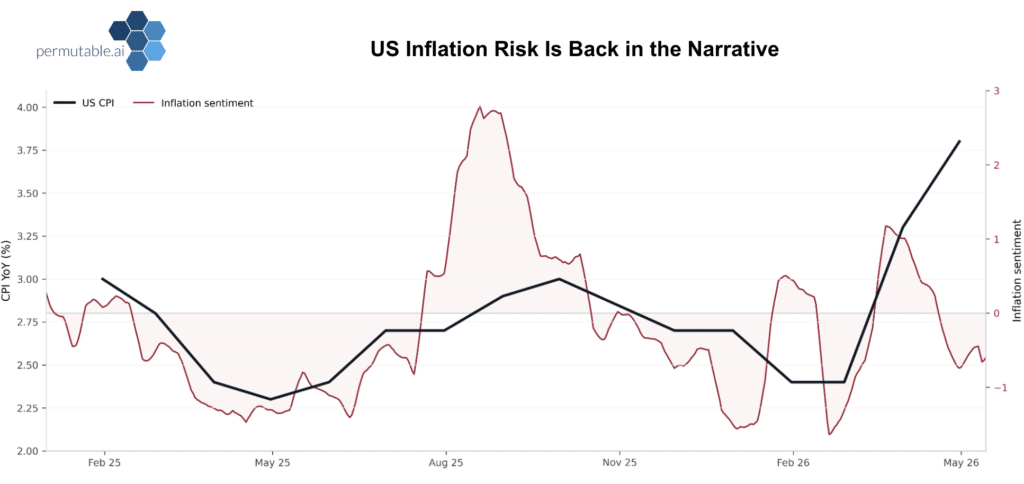

The recent chart shows why April matters.

Inflation sentiment has rebuilt as CPI has turned higher again. The point is not that sentiment perfectly predicted the April number. The more useful point is that inflation risk is re-entering the market conversation at the same time as official data are becoming less comfortable.

A single CPI print can be dismissed. A broader resurgence in the inflation narrative is harder to ignore.

The key issue is whether inflation language remains concentrated in energy and gasoline, or broadens into freight, services, margins, wages and policy credibility. The former can fade. The latter would make life harder for the Fed.

If inflation peaks quickly and energy prices fade, the Fed can wait it out.

If the shock lingers, markets have to reassess cuts, front-end yields, the dollar and equity multiples. April does not settle that debate. It raises the stakes of the next few months.

Energy persistence: If gasoline and broader energy costs fade, April can still be treated as a temporary shock. If they hold, the Fed’s room to ease narrows further.

Core pass-through: Services, transport and shelter will decide whether this becomes harder to dismiss.

Fed language: The policy debate is no longer only about when cuts begin. The possibility of a longer hold, or even a renewed hiking discussion, is back in play.

Inflation sentiment does not replace CPI. It changes the timing of the inflation debate.

The historic chart shows the signal has cycle relevance. The recent chart shows why it matters now: inflation language is rebuilding as official CPI turns higher again.

The US is not facing a clean demand-led inflation cycle. It is facing an energy-led cost shock that has reached the consumer basket at a difficult point for policy. For rates, the question is whether this delays the easing path or closes it altogether. For FX, it is whether a more cautious Fed keeps the dollar supported. For equities and credit, it is whether higher input costs and higher rates begin to weigh on margins, valuations and refinancing conditions.

April does not prove inflation is becoming embedded.

It does show that the bar for dismissing it has moved higher.

For institutional access to our US Inflation Sentiment Indices and regional macro indicators, contact us at enquiries@permutable.ai

Analysis

08 Jul 2026

US inflation sentiment signal shows shift from energy shock to sticky services risk

Read more >

Analysis

07 Jul 2026

Testing GMSI US monetary policy sentiment as a short-end rates signal

Read more >

Analysis

01 Jul 2026

Global Macro Sentiment Indices: Turning point-in-time macro sentiment data into live systematic workflows

Read more >