How oil and geopolitical risk are driving US inflation and Fed policy

14 Apr 2026

14 Apr 2026

This article explores how US inflation is being driven by rising oil prices and geopolitical risk, particularly around the Strait of Hormuz, which has reintroduced energy-led price pressure. Macro sentiment data from Permutable AI shows these risks were reflected in market narratives before appearing in official CPI data, signalling a potential shift in the inflation regime and limiting the Federal Reserve’s ability to ease policy.

There is a particular kind of market discomfort that does not begin with panic, but with recognition. It is the moment investors realise the path they had priced is no longer the one in front of them. That is where the U.S. inflation outlook stands in April 2026.

The market had settled into a comfortable pattern. Inflation was easing, the soft landing remained intact, and the Fed had already begun its easing cycle in late 2024. Further easing was still assumed to be the path of least resistance.

Then the geopolitical shockwave flipped the script.

Escalation in the Gulf and renewed disruption risk around the Strait of Hormuz pushed crude sharply higher, returning energy to the centre of the U.S. inflation outlook. Markets did not need a full interruption to flows, yet that is exactly what happened. The threat to shipping routes and the energy complex alone was enough to challenge the assumption of a smooth disinflation path.

March CPI provided the first hard confirmation of this. Headline inflation rose 0.9% m/m and 3.3% y/y, up from 2.4% previously. The energy index rose 10.9% in March, while gasoline surged 21.2%, accounting for much of the monthly increase.

This was more than an upside print. It hinted at a change in regime. An outlook built on easing price pressure and gradual policy loosening now faces a more systemic risk: energy-led inflation proving stickier than expected, forcing markets to revisit the path of rates.

Energy now sits at the centre of the inflation basket. Strip out volatile energy components and core CPI remains comparatively composed at 2.6% y/y, modestly below expectations.

But calm in the core basket offers limited reassurance. Energy shocks rarely stop at the petrol pump. They pass through freight costs, input margins and pricing decisions with a lag. April’s release will matter less for the headline than for signs that second-round effects are beginning to emerge.

None of this is mysterious. The geopolitical rupture pulled the trigger; the macro channels are now carrying the force of it. Renewed disruption risk around the Strait of Hormuz, the world’s most important energy corridor, has reintroduced a scarcity premium into oil. Brent has traded in the low-$100s in recent sessions, materially above pre-shock levels.

Weekend talks failed. Maritime pressure on Iranian shipping has intensified. Markets are no longer pricing a short-lived event risk. They are beginning to price duration.

Rising oil prices linked to geopolitical disruption are reintroducing inflation pressure, with energy acting as a transmission channel into broader costs and increasing the risk of more persistent inflation.

What Does Rising Inflation Mean For the Federal Reserve Outlook?

That leaves the Federal Reserve in an awkward position. Rates remain at 3.5% to 3.75% for a second consecutive meeting. Officials still signal limited easing over time, but confidence around that path has thinned materially.

Recent commentary has shown a Committee more concerned by upside inflation risk than downside labour-market weakness. Markets have noticed. Futures imply only a modest probability of cuts this year, while the 10-year Treasury yield has moved back towards the 4.35% area.

The market is no longer asking when cuts begin again. It is asking whether the easing cycle has already delivered most of what it can.

Elevated inflation risk is reducing the Federal Reserve’s flexibility, with markets increasingly questioning whether further rate cuts are achievable in the current environment.

Why Does Macro Sentiment Matter for Inflation and Fed Policy?

The relevant question is no longer whether U.S. inflation has turned higher. It has. The more important question is whether this is a transient geopolitical shock that mean-reverts, or the early stage of a more persistent inflation regime with consequences for rates, FX and cross-asset positioning.

Official data will settle the question in time. Market sentiment moves faster.

That is where Permutable’s sentiment data earns its place in the process. For macro PMs, it offers a live read on how narratives are feeding through inflation expectations, policy pricing and positioning before those shifts are fully reflected in the data. For systematic investors, it can function as an additional regime signal, helping distinguish short-lived noise from changes in the underlying macro backdrop.

Used properly, sentiment is not a substitute for hard data. It is an earlier signal of information.

Macro sentiment provides an earlier signal of inflation and policy shifts than official data, allowing investors to identify changes in market expectations before they are reflected in CPI or central bank decisions.

If the past two years offer a clear lesson, it is that inflation rarely turns first in the official data. It tends to turn first in the narrative around it. Markets adjust to that shift long before the statistics catch up.

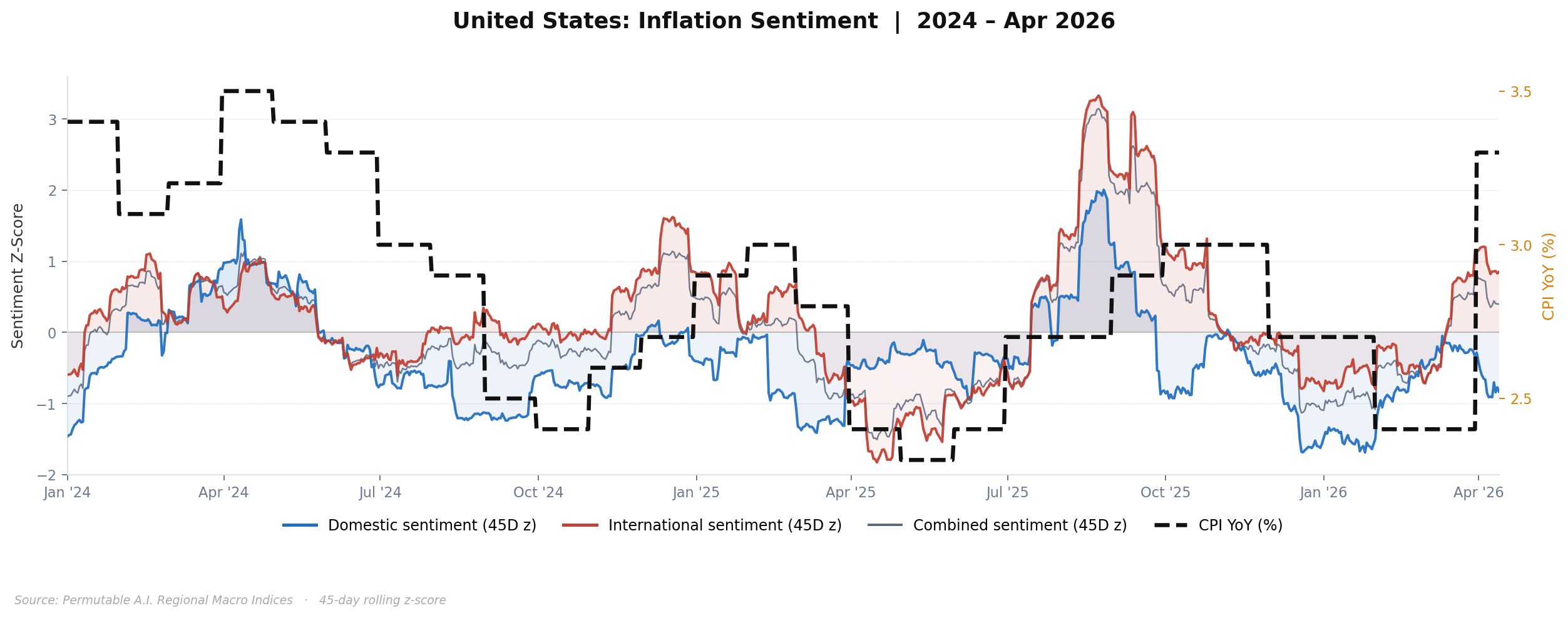

For much of 2024, domestic and international inflation sentiment traded around neutral to negative levels. The prevailing regime was one of orderly disinflation. Goods prices had normalised, supply constraints had eased, and investors had grown comfortable with the view that the next meaningful move in policy would be lower rates rather than renewed price pressure.

That confidence began to erode in spring 2025.

Headline CPI, then near 2.5%, subsequently moved back towards 4%. Permutable’s sentiment data did not merely anticipate the move. It identified the change in regime before the official releases validated it.

Late 2025 brought a temporary unwind as the first inflation pulse moved through the data and commodity pressures eased. Yet by early 2026, both domestic and international series had begun to recover from deeply negative readings, rising together as inflation concerns quietly re-emerged.

The combined signal is particularly telling.

This time the catalyst was different. Gulf escalation, shipping disruption and a renewed surge in crude prices replaced tariffs as the immediate transmission channel.

March CPI at 3.3% confirmed that turn.

At the right-hand edge of the chart, both measures remain positive. The international series, notably, has shown little sign of retreat since the March release.

The earlier pattern has not disappeared. It has reasserted itself.

Inflation sentiment consistently turned ahead of official CPI data, demonstrating that shifts in market narratives can signal regime changes before they appear in traditional economic indicators.

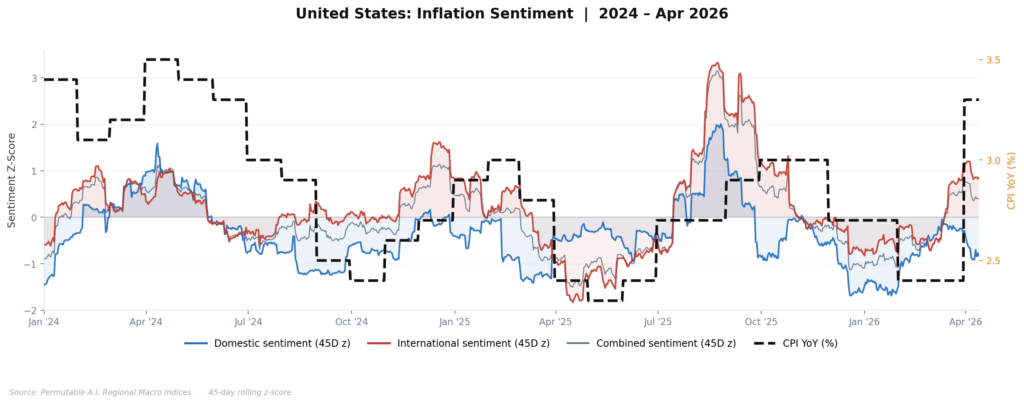

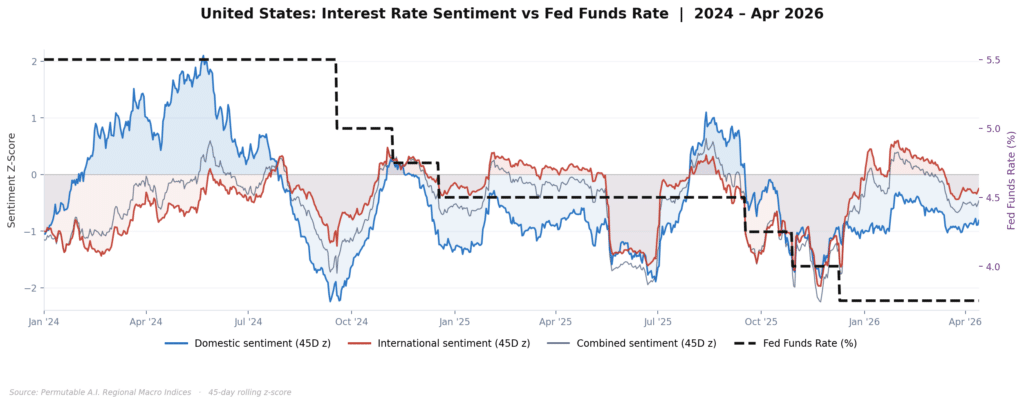

If Permutable’s inflation sentiment captured the return of price pressure, rate sentiment captured the market’s growing discomfort with the easing cycle that preceded it.

During the first half of 2024, domestic rate sentiment moved firmly positive while the Fed held policy at restrictive settings. Cuts were not simply expected; they had become embedded in the market’s central case.

The international series was more restrained. In retrospect, that divergence mattered. Domestic commentary leaned into the soft-landing narrative, while external investors remained more sensitive to geopolitical risk, commodity volatility and the possibility that U.S. inflation would prove less cooperative than consensus assumed.

The easing cycle began in late 2024, taking rates from 5.5% towards today’s 3.5% to 3.75% range. Soon after, both sentiment measures deteriorated sharply.

This was not frustration over the pace of cuts. It was a deeper reassessment that policy may have turned easier before the inflation process had been fully contained.

By late summer 2025, rate sentiment reached its weakest point of the cycle just as inflation was beginning to re-accelerate in the hard data. Tariff pressures, firmer goods prices and a renewed bid in energy were already testing the benign macro narrative.

Once again, sentiment moved ahead of confirmation.

The rebound into early 2026 was measured rather than convincing. Both series returned to mildly positive territory as markets adjusted to a Fed on hold. That recovery is now losing traction.

The combined rate signal tells a similar story. As domestic optimism around cuts faded and international caution persisted, the grey series rolled over decisively. That shift suggested doubts over the easing path had become more broadly embedded, rather than confined to one market perspective.

Treasury yields have moved higher again. The FOMC has adopted a more balanced, less explicitly dovish stance. Markets are no longer focused solely on the timing of the next cut.

They are beginning to reprice the possibility that the easing cycle has already run its course.

Rate sentiment deteriorated as markets reassessed the sustainability of the easing cycle, indicating that confidence in lower rates weakened before policy expectations fully adjusted.

Taken together, the two charts map the arc of the current macro cycle: from the confidence of 2024’s disinflation trade, through the inflation scare of 2025, to today’s more complex regime in which geopolitics, energy and policy uncertainty are again shaping the distribution of risks.

Inflation sentiment tends to turn first. Rate sentiment follows as markets reassess the policy path. That repricing then feeds through to front-end yields, the dollar and broader asset allocation.

Across both charts, the combined grey signal is the clearest read of regime change. It smooths local noise and isolated reactions, showing when domestic and international narratives are converging into a broader macro trend. At each major inflection point in this period, that convergence offered information ahead of confirmation in the official data.

The immediate market question is whether this proves another transient geopolitical premium or the early phase of a more durable inflation regime.

Current signals lean towards the latter.

Inflation sentiment remains elevated. Rate sentiment is re-firming. Official releases have begun to validate the turn.

That is where Permutable’s real-time macro sentiment has value. It does not remove uncertainty. It offers earlier recognition of regime change than traditional data can provide.

For macro desks, that means a cleaner read on narrative direction before it is fully expressed in pricing. For systematic investors, it offers a regime filter when relationships between inflation, policy and markets begin to change.

Both inflation and rate sentiment remain positive. The international series continues to lead. The hard data is beginning to follow.

The current macro regime reflects a shift from disinflation to renewed uncertainty, where energy, geopolitics and policy constraints are interacting to reshape inflation and interest rate expectations.

The current macro sentiment signal suggests that inflation risks are no longer transient. Energy-driven price pressure and persistent geopolitical uncertainty are increasing the probability of a more durable inflation regime.

For markets, this implies:

Macro sentiment data indicates that the current inflation shift is not purely a short-term shock. Oil-driven price pressure and persistent geopolitical risk are reinforcing a more complex inflation regime, with direct implications for Federal Reserve policy and market positioning.

Our Regional Macro Indices track domestic and international policy narratives across 50+ economies, updated daily. For access or integration enquiries, contact us at enquiries@permutable.ai.

This analysis uses Permutable AI’s Regional Macro Indices, which track sentiment across global news and financial narratives in real time. The indices measure both domestic and international sentiment across 50+ economies, allowing for early identification of macro regime shifts.

Analysis

29 Jul 2026

South Korea economy: the chip windfall is outrunning domestic growth

Read more >

27 Jul 2026

The tide turns on Russia inflation outlook as drone strikes spread from refineries to warehouses

Read more >

Analysis

27 Jul 2026

Saudi supply risk and import costs drive energy inflation sentiment higher

Read more >