Welcome to Our Weekly Forex Market Sentiment Roundup

Overview

This report provides a structured view of global FX sentiment using real-time data from Permutable AI. The dataset aggregates tens of thousands of headlines across hundreds of sources, transforming narrative flow into directional indicators across major currencies and FX pairs.

All sentiment indicators reflect market conditions at the time of writing. In current FX markets, narrative shifts can occur rapidly, particularly when driven by policy signals or intervention, and positioning may adjust quickly.

The defining feature of the current regime is not directional clarity, but balance. Across most major currencies and pairs, sentiment is neutral, with conviction levels clustering around 65 to 75 percent. This reflects a market where macro, geopolitical and policy drivers are offsetting one another rather than reinforcing a single trend.

Executive view

Currently, FX markets are characterised by equilibrium rather than trend persistence.

- The US dollar lacks sustained safe-haven momentum despite geopolitical risk

- Commodity-linked currencies are supported but face intermittent volatility

- Policy signals across central banks are no longer aligned, creating fragmentation

- Intervention dynamics, particularly in Japan, are introducing episodic dislocation

The result is a regime defined by consolidation, where price action is reactive rather than directional.

Major currencies

US dollar – Neutral

The US dollar is currently defined by competing forces. Geopolitical risk continues to provide some safe-haven support, but this has been offset by mixed domestic data, weaker growth signals and fluctuating Treasury yields. Recent sessions have also seen profit-taking, while intervention-driven yen strength has reduced the dollar’s momentum across key crosses.

Permutable AI’s data suggests the dollar is no longer acting as the central driver of FX direction. Instead, it is reacting to external developments and shifting risk appetite. Presently, this supports a neutral stance, though conditions may change quickly.

Euro – Neutral

The euro remains range-bound, with supportive and negative forces broadly offsetting one another. Rising yields and inflation expectations have provided intermittent support, while weak growth data, energy pressures and geopolitical uncertainty continue to limit upside. Recent price action shows that euro rallies are struggling to build sustained momentum, particularly when the dollar benefits from safe-haven demand or stronger US data.

Permutable AI’s data indicates a market still searching for direction rather than confirming a durable trend. As of now, the euro sits in a neutral regime, with volatility likely if policy or energy narratives shift.

British pound – Neutral

Sterling is trading in a mixed sentiment regime. Bank of England policy stability and occasional positive domestic data have supported the pound, but growth concerns, trade risks and geopolitical uncertainty continue to cap conviction. Recent rallies appear more corrective than structural, with gains repeatedly challenged by broader dollar dynamics and domestic fragility.

Permutable AI’s data suggests the pound is neither breaking down nor establishing clear leadership among major currencies. At the time of reporting, sentiment remains neutral, with positioning likely to remain sensitive to UK growth data, inflation expectations and global risk appetite.

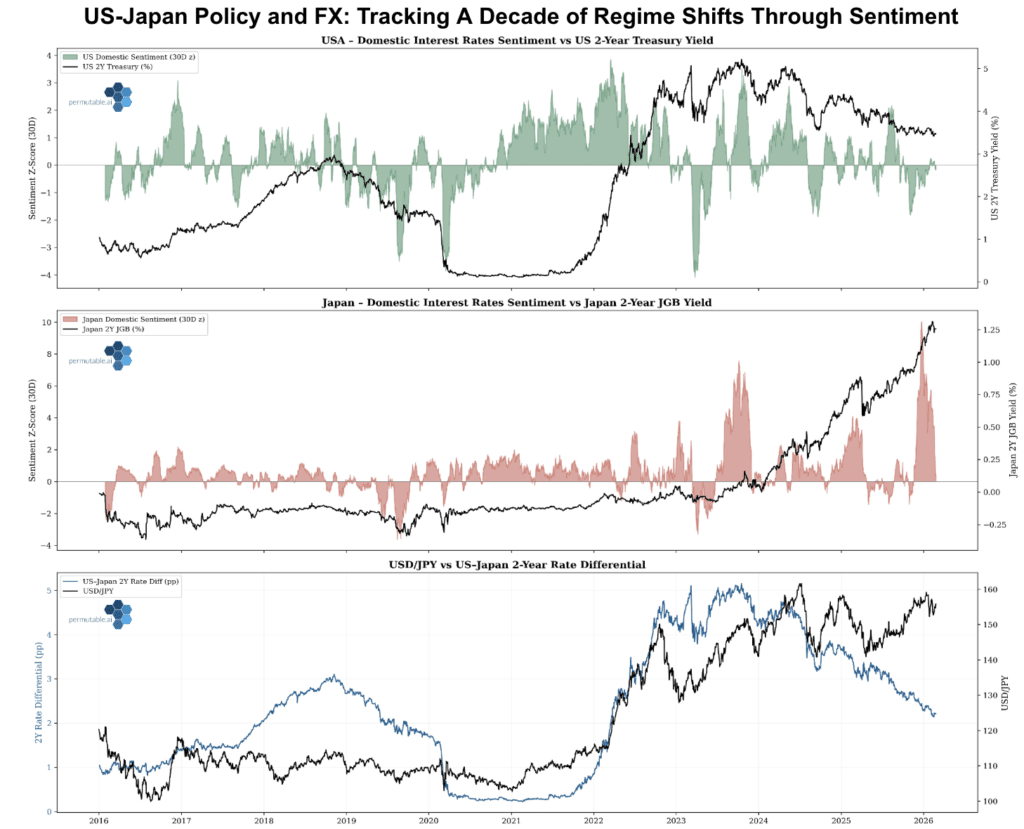

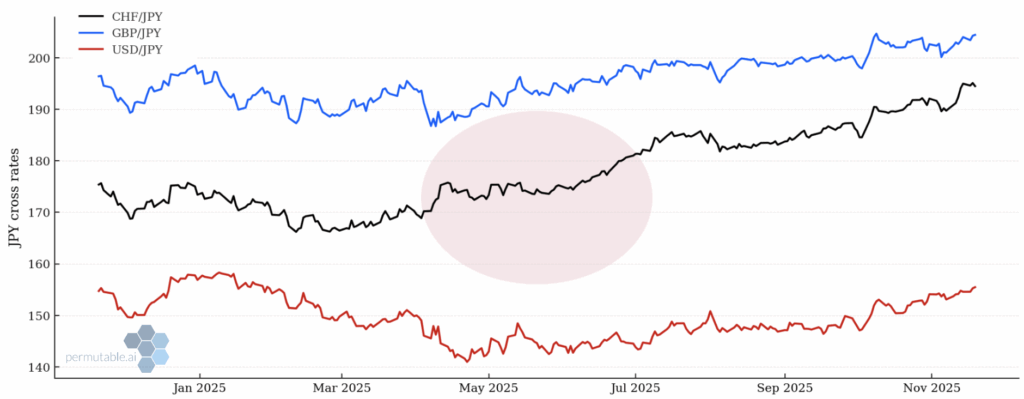

Japanese yen – Neutral

The yen remains one of the most volatile currencies in the current FX landscape. Recent intervention by Japanese authorities triggered a sharp appreciation, reinforced by safe-haven flows, higher Japanese government bond yields and firmer Bank of Japan signalling. However, part of that strength has since been offset by profit-taking and mixed domestic data, including concerns around below-target inflation.

Permutable AI’s data indicates that while yen downside has been challenged, the case for sustained appreciation is not yet conclusive. In the current context, the yen remains neutral, with intervention risk keeping volatility elevated.

Canadian dollar – Bullish

The Canadian dollar stands out as one of the stronger major currencies at the time of writing. Permutable AI data shows that CAD sentiment is being supported by elevated oil prices, positive energy-sector developments and expectations of potential Bank of Canada tightening. Canada’s role as a major energy exporter means rising crude prices continue to reinforce currency demand. Although soft domestic data and a firmer US dollar present counterweights, these have not yet displaced the dominant commodity narrative. The current bullish stance reflects strong energy-linked support, but remains sensitive to any reversal in oil prices.

Australian dollar – Neutral

The Australian dollar is supported by commodity exposure and rising expectations of a Reserve Bank of Australia rate increase, but the broader sentiment picture remains mixed. Permutable AI data shows that AUD has recovered from risk-off weakness, helped by materials and mining strength. However, stronger US dollar episodes, softer domestic confidence and a slight decline in Australia’s commodity price index have limited conviction. This creates cautious optimism rather than a clear bullish regime at the currency level.

In the current context Permutable AI’s sentiment indicators are showing that AUD remains neutral, though AUD/USD still shows stronger relative upside versus the dollar.

Chinese yuan – Neutral

The Chinese yuan remains in a managed and balanced sentiment regime. Permutable AI’s data shows support from firmer domestic policy signals, trade incentives and previous appreciation linked to stronger local data. However, these positives are being offset by external pressures, including US export controls, geopolitical tension and uncertainty around trade flows. Recent price action indicates consolidation rather than sustained appreciation. The yuan remains policy-supported but not independently directional.

Currently, Permutable’s sentiment indicators are neutral, with potential for volatility if policy stance, trade conditions or dollar dynamics shift materially.

High conviction pairs and key crosses

AUD/USD – Bullish

AUD/USD remains one of the clearest directional expressions in the current FX landscape. Permutable AI’s data shows that Australian dollar strength is being supported by elevated commodity prices, improving risk sentiment and expectations of a Reserve Bank of Australia rate move. At the same time, the US dollar lacks sustained momentum following the Federal Reserve’s recent pause. The pair experienced volatility earlier in the week during a risk-off episode, but subsequent price action indicates recovery and stabilisation.

At this stage, the balance of narratives continues to favour AUD, although the outlook remains sensitive to global risk sentiment shifts.

USD/CAD – Bearish

USD/CAD reflects strong Canadian dollar outperformance driven primarily by energy markets. Permutable AI’s data indicates that rising oil prices, supported by geopolitical tensions and supply concerns, are reinforcing CAD strength. As a major oil exporter, Canada benefits directly from this environment, which has outweighed intermittent support for the US dollar. Recent price action shows consistent downside pressure on the pair, with limited ability for USD to regain momentum.

As of now, Permutable’s indicators are showing a bearish stance reflecting sustained commodity-driven support for CAD, although the trajectory remains highly sensitive to any reversal in oil prices.

GBP/JPY – Bearish

GBP/JPY has shifted decisively lower, driven primarily by yen strength following intervention by Japanese authorities. Permutable AI’s data highlights that the yen’s sharp appreciation was supported by rising Japanese government bond yields and a more hawkish Bank of Japan stance. At the same time, the British pound has faced pressure from weaker domestic data and limited policy support. This divergence has created strong downward momentum in the pair.

At this point, the bearish outlook reflects yen-driven repricing rather than sterling collapse, although further direction remains dependent on additional intervention signals and global risk dynamics.

EUR/USD – Neutral

EUR/USD is currently characterised by balance rather than direction. Permutable AI’s data shows that euro support from rising yields and inflation expectations has been offset by US resilience and safe-haven flows. Geopolitical developments and energy price volatility have introduced further uncertainty, resulting in range-bound trading conditions. While the euro has demonstrated periods of strength, these have not translated into sustained upward momentum.

Presently, neither currency exhibits clear dominance, supporting a neutral stance. Future direction is likely to depend on policy divergence and shifts in macroeconomic expectations across both regions.

GBP/USD – Neutral

GBP/USD reflects a market defined by competing narratives. Sterling has shown resilience, supported by Bank of England policy stability and occasional positive data, but these gains have been capped by broader US dollar dynamics and geopolitical risk. The pair has exhibited repeated rallies followed by retracements, indicating a lack of sustained conviction. Permutable AI’s data suggests that both currencies are reacting to external drivers rather than establishing independent trends.

As things stand, the pair remains range-bound, with direction likely to depend on shifts in global risk sentiment and relative macro data surprises.

USD/JPY – Neutral

USD/JPY is currently driven by intervention dynamics rather than conventional macro factors. The pair initially moved higher on US yield support and geopolitical risk, but this was sharply reversed following direct intervention by Japanese authorities. Permutable AI’s data shows that this has introduced significant volatility and capped upside potential for the dollar. At the same time, underlying yen fundamentals remain mixed, limiting sustained appreciation.

At the time of writing, the pair is trading in equilibrium, with traders cautious and highly sensitive to further policy action from the Bank of Japan and evolving global risk conditions.

EUR/GBP – Neutral

EUR/GBP remains firmly range-bound, reflecting a balance of weaknesses rather than strengths. Permutable AI’s data indicates that both the euro and sterling are influenced by domestic economic challenges and external pressures, including energy costs and geopolitical developments. While the euro has benefited from yield support, UK asset demand has provided relative stability for sterling. Neither currency has established a decisive advantage.

Currently, the cross reflects equilibrium conditions, with limited directional conviction. Future movement is likely to be driven by relative growth data and shifts in central bank expectations.

Conclusion

FX markets are currently defined by competing narratives rather than a single directional force. Permutable AI’s data indicates that while selected pairs show conviction, the broader market remains balanced. Most currencies are trading within neutral regimes at the time of writing, with volatility driven by shifts in policy, commodities and geopolitics. The advantage lies in tracking sentiment as it evolves, rather than reacting after price adjusts.

Access real-time FX sentiment intelligence

Institutional FX teams require more than delayed macro data or reactive price signals. At Permutable, our real-time sentiment intelligence layer continuously monitors global news flow, policy developments and macro narratives, transforming them into structured, model-ready indicators across currencies and FX pairs.

This enables earlier identification of regime shifts, clearer attribution of market drivers and more precise timing of positioning decisions.

To access Permutable’s full real-time FX sentiment indicators, cross-asset narrative analytics and institutional data feeds, request a demo or speak directly with our team at: enquiries@permutable.ai