Japan energy inflation is becoming a BoJ problem as JGB yields price inflation risk

09 Jun 2026

09 Jun 2026

This article examines how Japan’ energy inflation inflation pressure is complicating the Bank of Japan’s policy path and changing the way investors should read JGB yields. Using Permutable’s forthcoming Global Macro Sentiment Indices, it explores energy sentiment, BoJ policy sentiment, political and geopolitical tension, yen weakness and the US-Japan yield gap.

Japan’s rates story is becoming harder to classify. JGB yields are no longer being driven only by the end of yield-curve control or the gradual removal of an old policy distortion. Those forces still matter, but the May-June data flow has added a more difficult layer.

The key facts now point in the same direction. Wholesale inflation has risen to a three-year high at 4.9% year on year, driven by energy and import costs. The 10Y JGB yield has reached 2.54%. BoJ normalisation pressure remains positive at +1.6 sigma, even after easing from earlier highs. The Ministry of Finance has spent more than ¥11tn supporting the yen since late April. At the same time, economists now expect rates to reach 1.0% by end-June and 1.25% by year-end.

That combination matters because Japan’s inflation problem is no longer just a question of headline CPI. Energy, import costs and yen weakness are interacting with policy credibility. The BoJ can usually look through a Japan energy inflation shock if it fades quickly. The harder case is when that shock arrives before the wider inflation process has settled.

If Japan energy inflation remains isolated, the BoJ has more room to wait. If it feeds through import prices, household bills and domestic price-setting, JGB yields may continue to carry more than a normalisation premium.

For institutional investors, the implication is that Japan is no longer only a post-YCC rates trade.

The JGB market is now being shaped by a broader mix of inflation pressure, yen pass-through, BoJ credibility, political tension and geopolitical risk. That matters across duration, FX, relative rates and cross-asset allocation.

A market that is pricing policy normalisation can reverse when expectations are met. A market that is pricing inflation credibility, FX stress and risk premium is more difficult to fade.

The central issue is no longer whether Japan has exited an old regime. It is whether the new regime is one in which inflation, the yen and JGB yields reinforce each other.

Permutable’s Global Macro Sentiment Indices show the pressure beneath the JGB move.

Energy is the clearest acceleration. BoJ policy sentiment has cooled, but not turned. Political and geopolitical tension sentiment has moved higher alongside JGB yields. The US-Japan policy sentiment spread also points to pressure on the hard yield differential.

GMSI is not forecasting the next BoJ meeting. Its value lies in mapping the drivers that markets absorb between data releases and policy decisions. In Japan’s case, those drivers now include energy pass-through, policy credibility, FX intervention risk and political constraint.

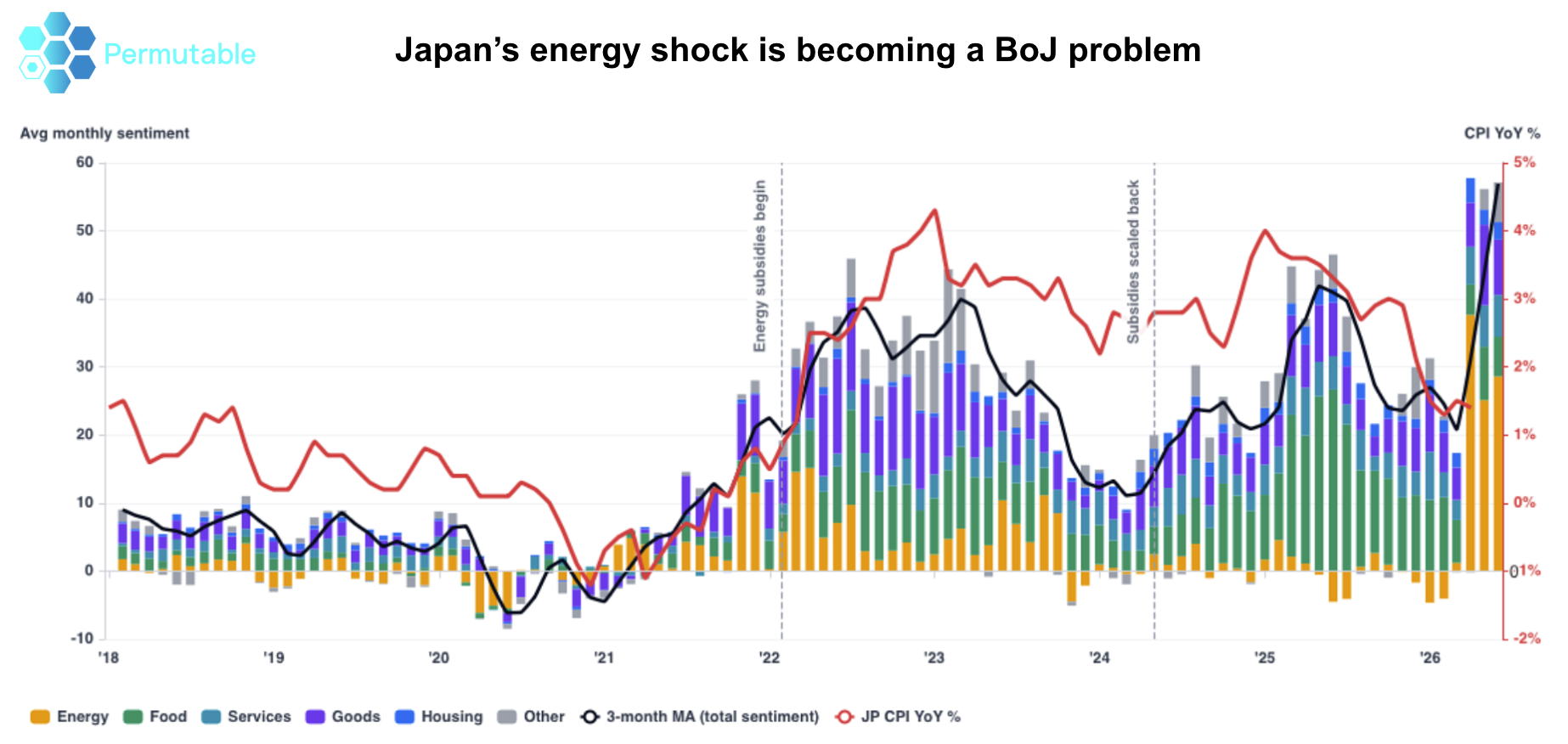

Above: Energy sentiment has become the dominant contributor to Japan’s inflation narrative. Rising import costs, commodity prices and yen pass-through effects are increasing pressure on households and businesses, creating a more complex challenge for the Bank of Japan’s inflation management strategy. Source: Permutable Global Macro Sentiment Indices (GMSI),

Energy sentiment is the sharpest move in the latest Japan inflation breakdown.

That fits the May-June macro flow. Wholesale inflation has risen to 4.9% year on year, its highest rate in three years, with energy and import costs the main pressure points. Yen weakness adds another channel, raising the local-currency cost of imported fuel, food inputs and industrial materials.

For Japan, this is not a distant commodity story. Energy pressure can move quickly into utilities, transport and food distribution. Subsidies may soften the headline CPI path, but they do not remove the underlying pressure from import costs and household-facing prices.

An energy shock can be looked through if it fades quickly. The harder case is when it arrives while the wider inflation process is still unsettled. That is where Japan now sits.

Energy starts the move. The policy problem begins if the shock becomes part of the domestic inflation process.

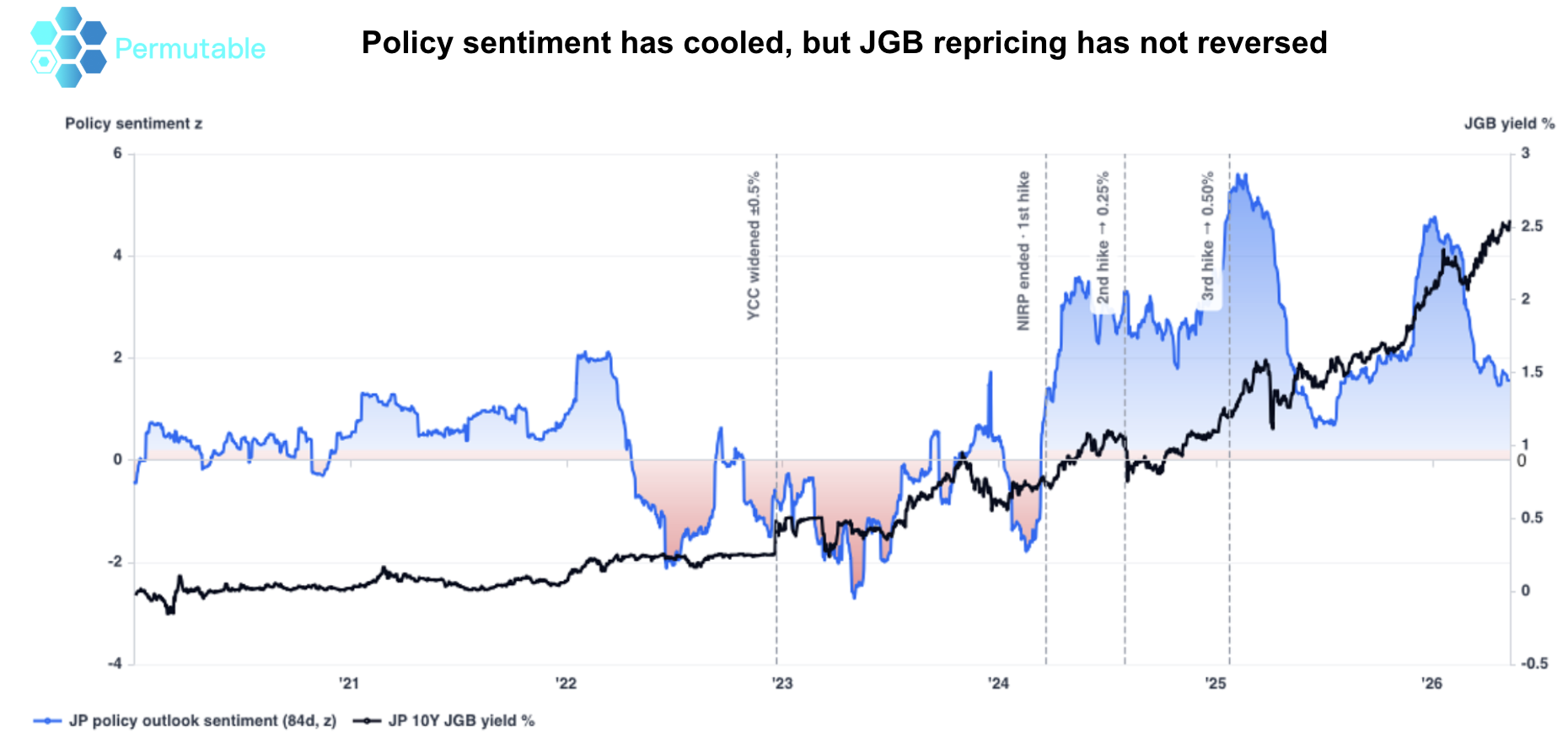

Above: BoJ policy sentiment has eased from earlier highs, but Japanese government bond yields continue to rise. The divergence suggests markets are increasingly focused on inflation persistence, yen weakness and risk premiums rather than policy normalisation alone. Source: Permutable Global Macro Sentiment Indices (GMSI).

BoJ normalisation pressure remains positive at +1.6 sigma. The 10Y JGB yield has reached 2.54%.

The signal has eased from its earlier peak. That argues against treating the current move as a fresh, uninterrupted acceleration in policy pressure. But it remains above zero, and the recent hard-news flow has not softened enough to make that reassuring.

The policy backdrop has also shifted. Economists now expect rates to reach 1.0% by end-June and 1.25% by year-end, while BoJ communication has placed more weight on second-round effects, wage gains and higher oil prices.

The BoJ is still managing an inflation credibility problem, not just the technical exit from an old policy regime. The case for further tightening now rests less on the mechanics of post-YCC adjustment and more on whether energy, import costs and wage-sensitive categories keep inflation pressure alive.

For JGB investors, the risk is not necessarily another abrupt sell-off. It is a market that struggles to recover because the BoJ cannot credibly sound relaxed while inflation pressure remains visible.

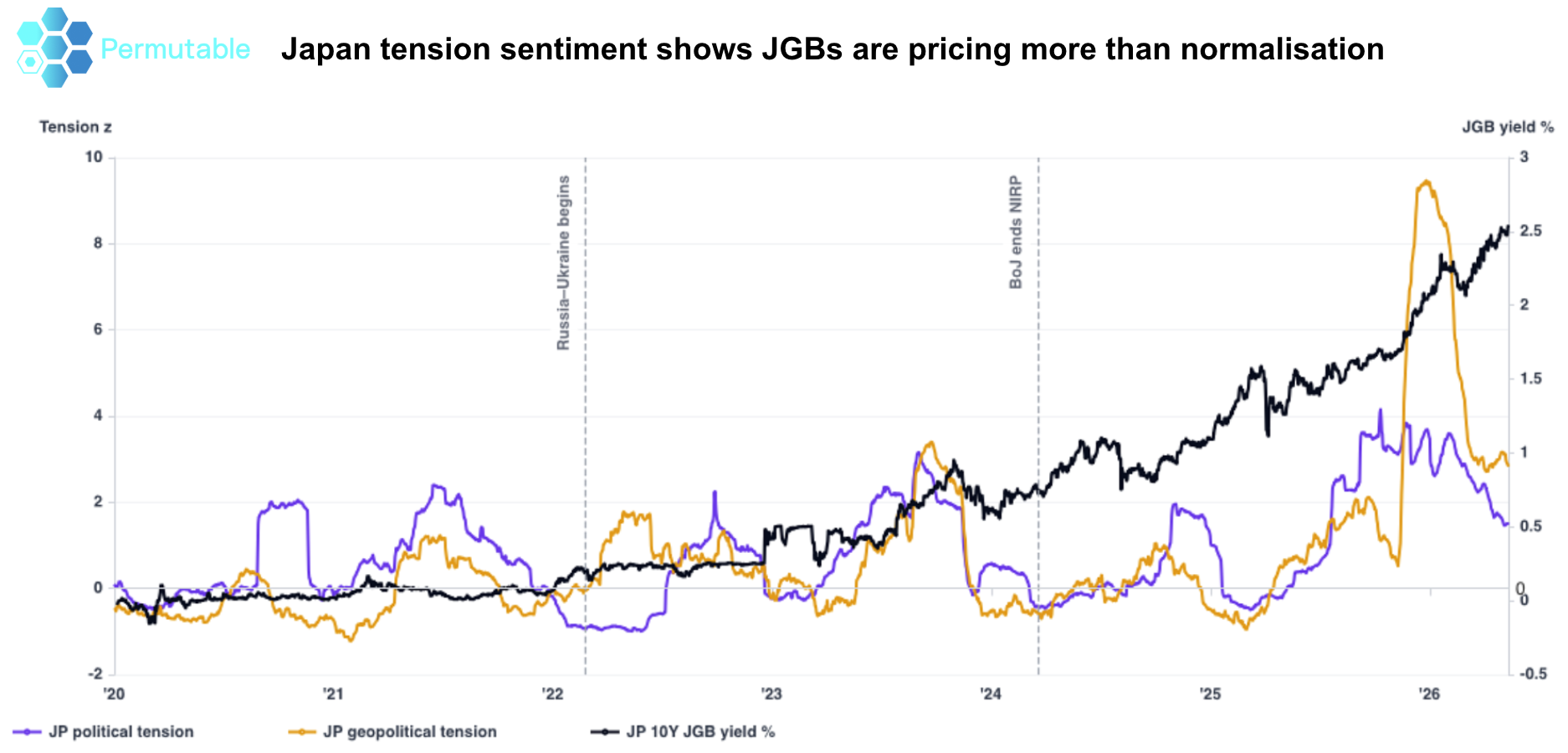

Above: Japan political and geopolitical tension sentiment has risen alongside 10-year JGB yields, indicating that investors are increasingly pricing risk premiums related to energy exposure, geopolitical uncertainty and policy constraints rather than simply Bank of Japan normalisation. Source: Permutable Global Macro Sentiment Indices (GMSI).

Political and geopolitical tension sentiment has risen alongside JGB yields.

The chart does not say tension is the main driver of the sell-off. BoJ policy expectations and inflation persistence still matter most. But it does show that the JGB move is carrying more than a clean normalisation story.

For Japan, geopolitical tension matters through energy exposure. A rise in Middle East supply risk can feed directly into import costs, utilities and transport. Domestic political tension matters through the fiscal response to higher household costs, especially if relief measures or subsidies complicate the BoJ’s tightening path.

That is the read-through for investors. Rising JGB yields are not just about where the next policy rate settles. They also reflect a market pricing a less comfortable mix of inflation pressure, yen weakness, energy exposure and policy constraint.

The exchange rate has become central to Japan’s inflation problem.

Yen weakness lifts import costs. Import costs feed household prices. Higher household inflation narrows the BoJ’s tolerance for further currency weakness. The Ministry of Finance has already spent more than ¥11tn supporting the yen since late April, showing that currency weakness is now being treated as part of the inflation-management problem.

The yen is no longer only reacting to the rate gap. It is feeding the inflation pressure that makes the rate gap harder to sustain.

For rates and FX desks, the value of GMSI lies in showing which pressure is leading: energy pass-through, BoJ credibility, political and geopolitical tension, FX intervention risk or residual US inflation.

Price compresses those pressures into one number. Driver-level sentiment keeps them separate.

Inflation breadth: whether energy pressure fades, or moves further through household-facing prices.

BoJ reaction function: whether policy sentiment stabilises above zero, or the earlier hawkish impulse continues to fade.

JGB repricing: whether yields are still reflecting normalisation, or a higher risk premium around inflation, politics and energy exposure.

FX pressure: whether the Ministry of Finance keeps resisting yen weakness, or allows rate differentials to carry more of the adjustment.

US-Japan spread: whether the hard yield differential follows the sentiment spread lower, or begins to reverse.

Japan has become a harder market to classify.

The inflation impulse is energy-led, but the pass-through channels are warmer than the headline implies. Wholesale inflation at 4.9%, a 2.54% 10Y JGB yield, positive BoJ policy sentiment and more than ¥11tn of FX intervention all point to a market being pulled by more than one force.

BoJ policy sentiment has cooled, but it has not turned. FX weakness is now part of the inflation-management problem. Political and geopolitical tension are adding a risk-premium layer to what began as a cleaner normalisation trade.

The old regime of suppressed yields, weak inflation and a structural overseas-yield advantage has gone. Japan now behaves more like an inflation-sensitive rates market, where energy exposure, yen dynamics and BoJ credibility interact directly.

GMSI helps identify which pressure is leading. At present, more than one is moving in the same direction.

For institutional access to our Japan Inflation and Policy Sentiment Indices, contact us at enquiries@permutable.ai

JGB yields are rising due to a combination of higher inflation expectations, Bank of Japan (BoJ) policy normalisation, persistent yen weakness and rising energy costs. While the end of yield curve control remains important, investors are increasingly pricing inflation credibility, FX risks and geopolitical pressures into Japanese government bonds.

Japan’s inflation pressure is being driven primarily by energy costs, imported inflation and yen depreciation. Wholesale inflation recently reached 4.9% year-on-year, with higher import costs feeding through to businesses and households. Energy remains one of the strongest inflation drivers identified by Permutable’s Global Macro Sentiment Indices.

A weaker yen increases the cost of imported goods, energy and raw materials. As Japan remains heavily dependent on imports for energy and commodities, currency weakness can accelerate inflation through higher household bills, transport costs and business input prices.

The Bank of Japan influences JGB yields through interest rate policy, bond purchases and market communication. As expectations for higher policy rates increase, investors often demand higher yields on government bonds. However, JGB yields are also increasingly influenced by inflation expectations, currency pressures and risk premiums.

BoJ policy normalisation refers to the gradual removal of ultra-loose monetary policies that were implemented to combat decades of low inflation and economic stagnation. This includes ending yield curve control, raising policy rates and reducing market interventions.

Japan energy inflation can have a broad impact across the Japanese economy. Higher fuel and utility costs often feed into transport, manufacturing and consumer prices. If energy-driven inflation becomes embedded in the wider economy, the Bank of Japan may face greater pressure to tighten monetary policy further.

Japan’s Ministry of Finance has spent more than ¥11 trillion supporting the yen since late April. FX intervention aims to reduce excessive currency weakness, which can otherwise increase imported inflation and complicate the Bank of Japan’s efforts to maintain price stability.

Global Macro Sentiment Indices (GMSI) are AI-generated macroeconomic indicators developed by Permutable. They transform global information flows into structured sentiment signals across countries, asset classes and macro themes, helping investors monitor emerging risks, opportunities and narrative shifts in real time.

GMSI helps investors identify the underlying drivers shaping Japanese markets, including energy sentiment, BoJ policy sentiment, geopolitical risk, inflation pressure, FX intervention risk and yield differentials. Rather than focusing solely on market prices, GMSI reveals the narrative and sentiment dynamics influencing investor behaviour.

Key indicators include inflation breadth, energy price pass-through, Bank of Japan policy communication, yen intervention activity, JGB yield movements and the US-Japan policy differential. Changes across these areas will help determine whether Japan’s current repricing remains a policy normalisation story or evolves into a broader inflation and risk-premium regime.

Analysis

08 Jul 2026

US inflation sentiment signal shows shift from energy shock to sticky services risk

Read more >

Analysis

07 Jul 2026

Testing GMSI US monetary policy sentiment as a short-end rates signal

Read more >

Analysis

01 Jul 2026

Global Macro Sentiment Indices: Turning point-in-time macro sentiment data into live systematic workflows

Read more >