Emerging markets inflation signals – a look across Turkey, Brazil and Nigeria

17 Jun 2026

17 Jun 2026

This article examines why emerging-market inflation should be read as a regime story, not just a CPI-release story. Using Turkey, Brazil and Nigeria as examples, it shows how Permutable’s forthcoming Global Macro Sentiment Indices help investors track sticky inflation, policy-cycle shifts and FX-led pass-through before official data fully confirms the turn.

Emerging-markets – and in particular – emerging markets inflation signals – can be difficult to track with consistent and fast flowing data points, the reality of what happening in those markets rarely turns at the moment the a CPI print or policy decision says it has. Pressure builds first in the narrative flow: local reporting, policy language, external coverage, funding stress, FX commentary and household sensitivity sets in. The official data then confirms, lags or revises the story.

That is the value of the sentiment layer in your toolkit. It is not replacement of CPI, the official rates or bond yields. But where it does help is in identifying when the information set around those variables has changed, spotting inflection points as they happen.

This week’s EM signals focus on three different countries observing each’s distinct inflation and policy regimes.

Turkey is the sticky-inflation case. Brazil is the policy-cycle case. Nigeria is the FX-pass-through case. The sentiment signal helps show whether the pressure is still building, fading or changing channel.

Turkey’s annual inflation rate rose to 32.61% in May from 32.37% in April, while monthly CPI increased by 1.71%. The monthly pace has hastened from April’s 4.18% rise, but the inflation process is still too high to treat as resolved even though it has come down from historic norms.

The sentiment pressure remains concentrated in essential and administered categories, including housing and energy, electricity, gas and other fuels. These are not discretionary-price categories that can fade quietly with weaker demand. They are socially visible, politically sensitive and harder for households to avoid.

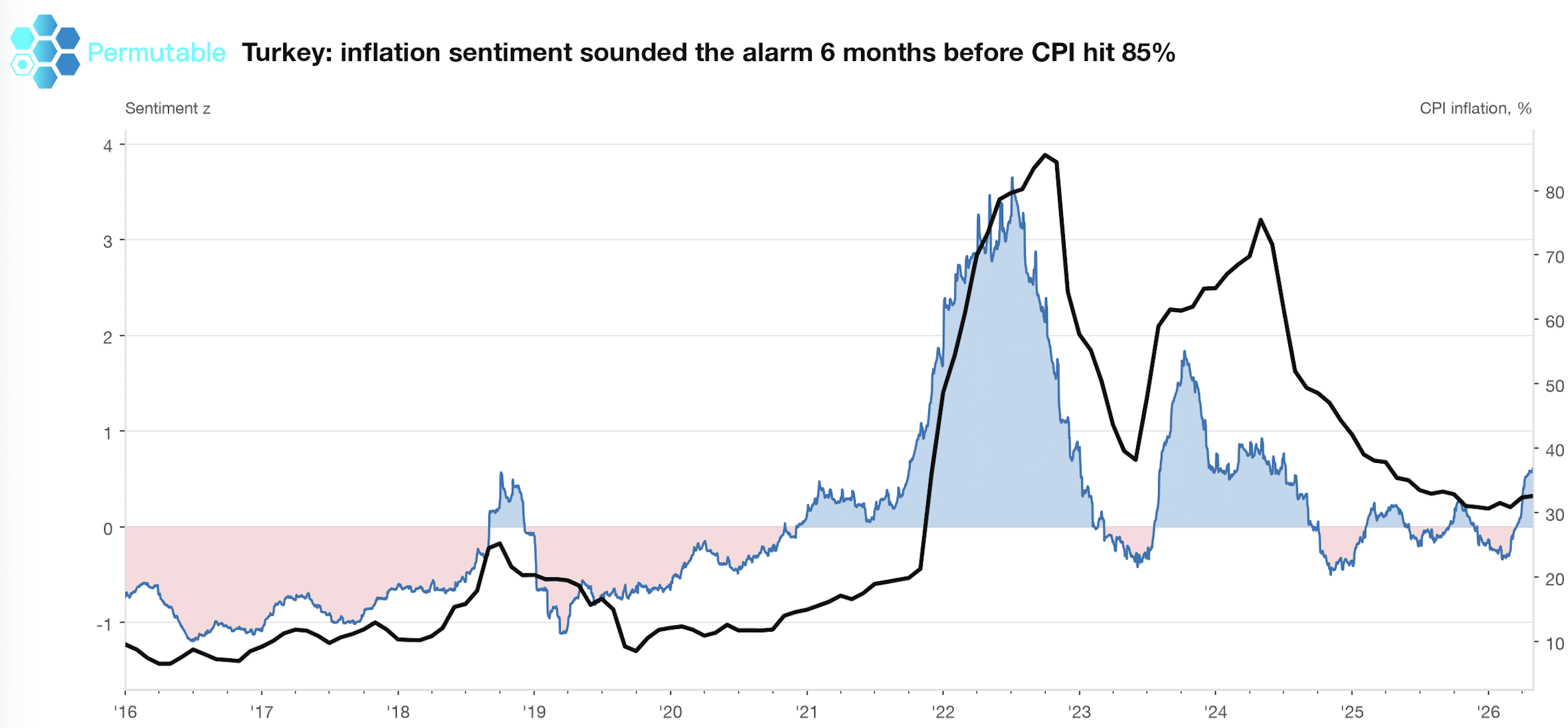

This is where the sentiment chart adds value. In the historical Global Macro Sentiment Indices chart, Turkish inflation sentiment rose from late 2021, around six to nine months before CPI reached its 85.5% peak in 2022. The signal also began to fall before the official peak, capturing the shift towards base-effect disinflation before it was fully visible in the annual rate.

That is not a claim that sentiment mechanically forecasts each CPI print. Its value is earlier in the chain. It captures when the inflation discussion changes character: from a known high-inflation problem to an accelerating regime, and later from panic to gradual normalisation.

Turkey now sits in the second phase. Sky high inflation is in the rear view mirror, but the return to lower altitudes remains the next leg of the challenge. When housing, utilities and food remain firm, the annual CPI rate can fall while the lived inflation regime still feels sticky. For EM desks, the useful signal is whether inflation sentiment keeps softening, or whether the essential categories begin to rebuild pressure before the CPI data fully turns.

Investor read: Turkey is no longer a peak-inflation story. It is a persistence story. The value of sentiment is in detecting whether disinflation is becoming embedded, or whether the economy remains caught up in a high-inflation regime with recurring monthly pressure.

Above: Turkey’s inflation sentiment rose months before CPI peaked above 85% in 2022, showing how narrative pressure can signal a regime shift before official inflation data fully confirms it.

Brazil’s central bank has begun to ease, but the policy corridor remains narrow. The Selic was cut to 14.50% in April after a period at 15%, with market expecting another 25 bp reduction to 14.25% to proceed. That is an easing cycle, but not a full pivot towards growth support.

Inflation explains the caution. May CPI rose 0.58% on the month and 4.72% on the year, above the 3% target and sits just outside the 1.5 pp tolerance band. Food prices remain a source of pressure, while services and domestic demand leave the central bank with limited room to accelerate cuts.

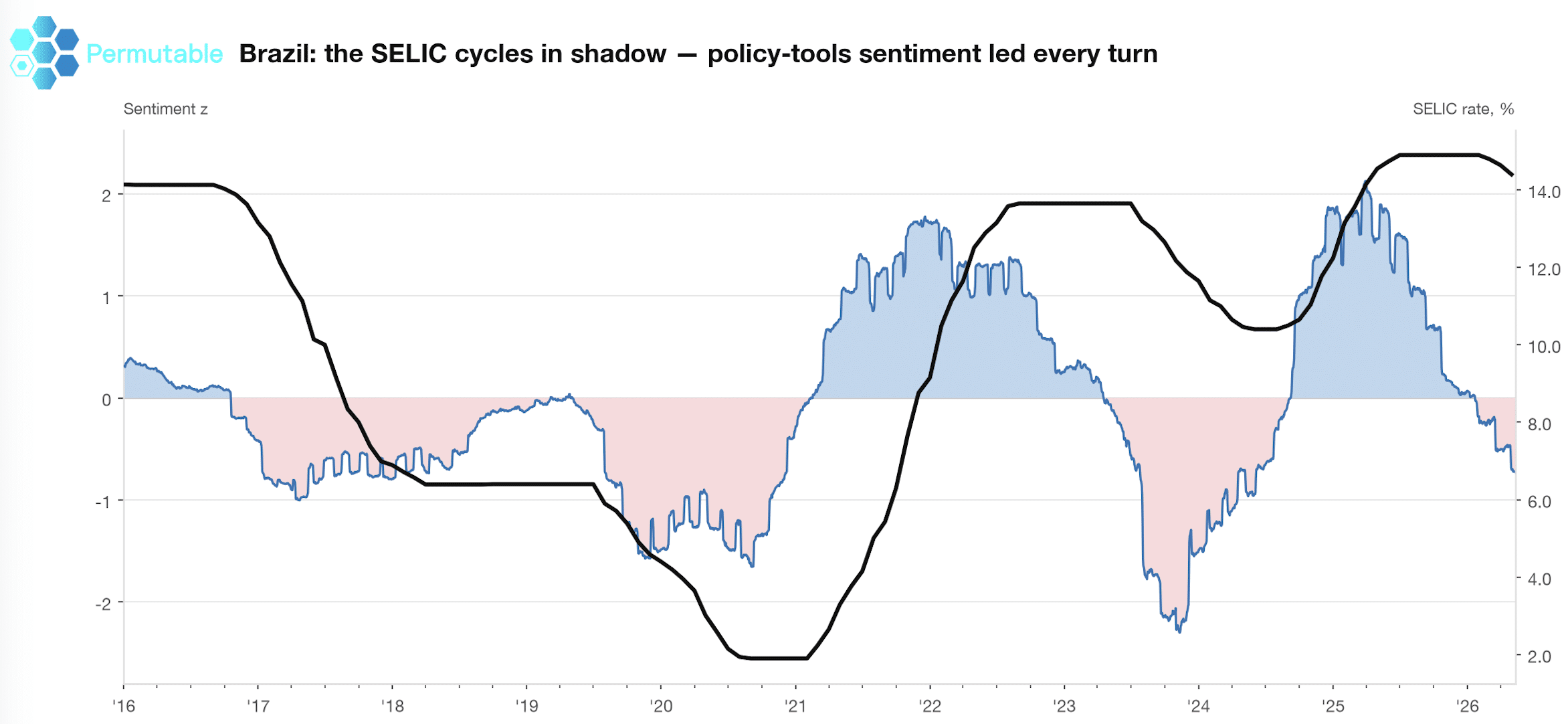

The Brazil chart earns its keep because the sentiment signal maps directly onto the policy cycle. GMSI policy sentiment pre-signalled three complete monetary cycles: the 2016 easing cycle, the 2021 hiking cycle and the renewed hawkish turn before SELIC moved back towards 14.75%. The rate of change is the strongest validation of sentiment picking up on the narrative pressure as it swings from hawkish to dovish.

What you see is sentiment carrying information over the policy reaction function, not just moving with rates. In Brazil, the market does not only need to know whether CPI is high. It needs to know whether policy stance is becoming more tolerant of inflation and rates, or less so, with concerns building around restricting growth being constrained by expectations and fiscal risk.

The current message is leaning towards easing. The central bank can cut because real rates were too high, but it cannot move quickly while inflation is above target. That makes the sentiment layer useful as a policy-temperature gauge. If policy sentiment turns less cautious, the dovish case gains support. If it stays hawkish, nominal rate cuts may not translate into a broader loosening of financial conditions.

Investor read: Brazil is easing from a restrictive stance. The value of sentiment is in reading the policy corridor before the next rate decision: how much room Copom believes it has, not just where the Selic sits today.

Above: Brazil’s policy sentiment has tracked major Selic cycles, helping investors read the central bank’s reaction function before policy shifts are fully reflected in rate decisions.

Nigeria’s annual inflation rate rose for a third consecutive month to 15.93% in May from 15.69% in April. Monthly CPI slowed to 1.75% from 2.13%, but the annual direction still moved higher.

The detail points to a pass-through problem. Food inflation accelerated, transport costs remained firm, and core inflation rose to 16.82%. Imported food prices, fuel costs and service-sector pressures not helped by the months of tensions between US Iran mean inflation has been left exposed to spillover in the FX channel.

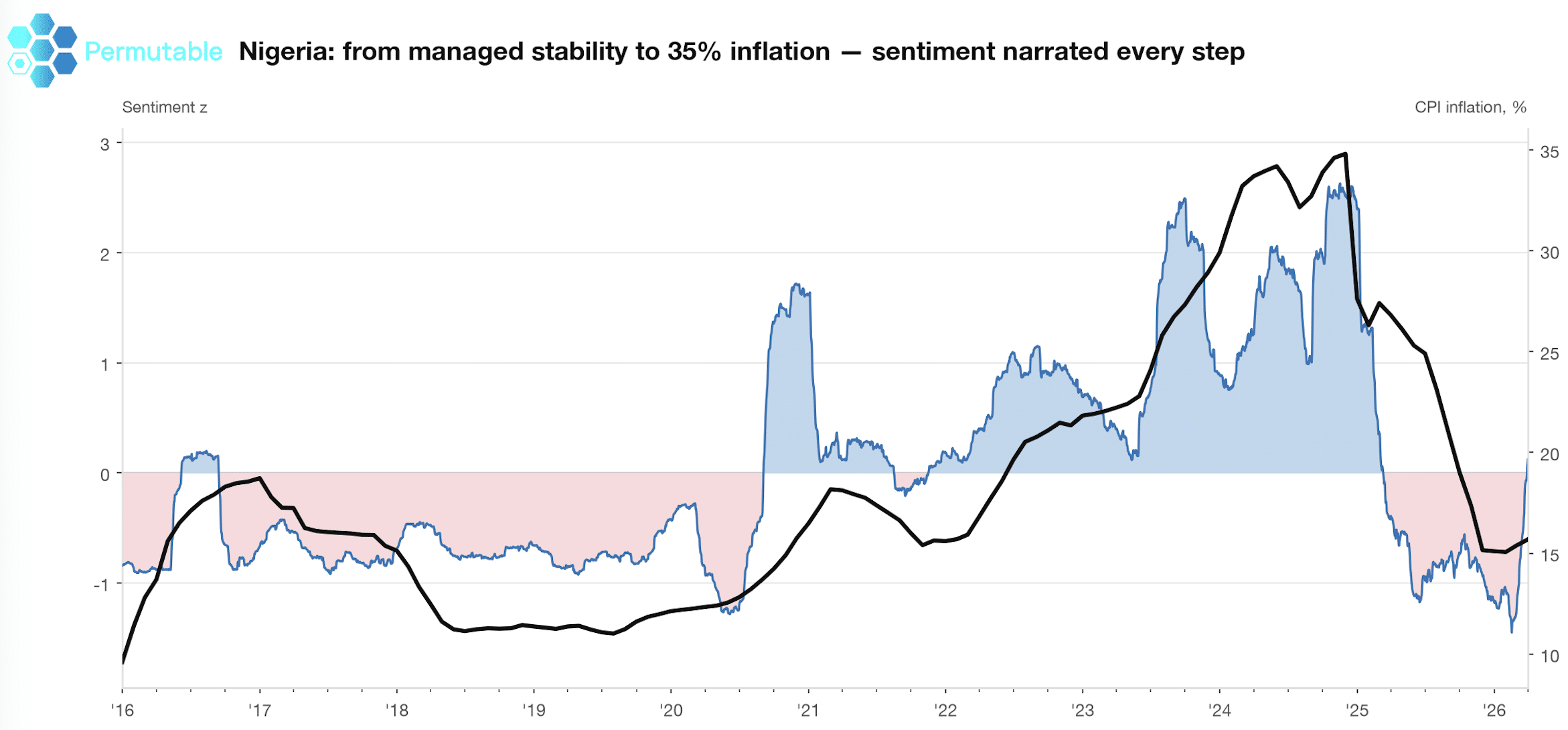

We chose Nigeria because its one of the latest additions to the expansion of over macro coverage from 45+ countries to 95+ and offers a insightful window on how well we are able to pick up on international news both internationally but also on the ground at local level. The chart is the useful in reading the regime cycle, especially during the managed-peg period, inflation was high but sentiment remained relatively unfazed. The market already understood the pressure as structurally embedded as the narrative was baked into expectations. Yet you can see the signal shift once the currency regime flipped and the naira channel became the main transmission mechanism.

That is the real value of sentiment in Nigeria. It helps distinguish stale inflation from active inflation pressure. A country can have high CPI without a fresh market signal if the story is already priced and slow-moving. But when FX policy shifts, fuel prices reset or import costs surge, the same inflation theme becomes dynamic again. Coverage begins to focus on pass-through, credibility and household pressure.

For Clients looking at Nigeria should therefore be read less as a conventional demand-cycle story and more as a currency-transmission story. Weak domestic demand does not prevent inflation from re-accelerating if the naira weakens or imported-cost pressure returns. The sentiment signal is most useful when it captures that change in transmission before it is fully visible in the CPI basket.

Investor read: Nigeria remains vulnerable to FX-led inflation persistence. The value of sentiment is in identifying when inflation is becoming active again through the naira, fuel, food and import-price channels.

Above: Nigeria’s sentiment signal became more valuable as the currency regime shifted, helping distinguish structural inflation from active FX-led pass-through through the naira, fuel, food and import-price channels.

◆ Turkey: identifies the inflation regime before the annual CPI peak and helps monitor whether disinflation is genuinely taking hold.

◆ Brazil: tracks the policy reaction function, not just the rate level. This is why the SELIC chart has the strongest validation in the pack.

◆ Nigeria: separates structural inflation from active pass-through risk, especially when the FX regime changes.

The three charts make a stronger point together than they do separately.

Turkey shows sentiment as an early inflation-pressure gauge. Brazil shows sentiment as a policy-cycle gauge. Nigeria shows sentiment as a regime-change gauge.

That is the broader value of the framework. It does not treat all EM inflation prints as equal. It asks what is driving the pressure, whether the driver is changing, and whether official data is confirming a move already visible in the information flow.

A sharper way to frame the week is this:

Turkey remains trapped in sticky inflation, Brazil is easing only within a narrow policy corridor, and Nigeria remains exposed to FX-led pass-through. Across all three, the useful signal is not the headline CPI print alone, but whether the inflation regime is changing before the data fully confirms it.

Permutable’s Global Macro Sentiment Indices tracks these shifts across countries and macro themes, helping investors identify where pressure is forming, how it is travelling and when it is becoming relevant for markets.

A limited number of EM and macro desks are being invited to preview GMSI ahead of launch, with early access to sample indices, historical data and API previews. Register your interest here.

Why do emerging-market inflation signals matter for investors?

Emerging-market inflation signals help investors monitor pressure before it is fully visible in official CPI data. They are useful where inflation, policy, FX, funding stress and political risk move faster than the release calendar.

What makes sentiment useful in emerging-market macro analysis?

Sentiment captures changes in local reporting, policy language, FX commentary, external coverage and household-cost pressure. This helps investors see whether macro pressure is building, fading or changing channel before official data or consensus forecasts catch up.

What are Permutable’s Global Macro Sentiment Indices?

Permutable’s Global Macro Sentiment Indices are forthcoming structured macro sentiment datasets designed to track narrative shifts across countries, macro themes and information sources, including inflation, monetary policy, FX, growth, political risk and sovereign-risk signals.

Why is emerging-market inflation described as a regime story?

Emerging-market inflation is described as a regime story because the drivers vary by country and phase. Inflation may be driven by sticky domestic costs, policy credibility, currency weakness, import prices, fuel costs or political risk. The headline CPI print alone does not always show which regime is active.

How can sentiment data help before CPI or policy data is released?

Sentiment data captures changes in local reporting, policy language, FX commentary, external coverage, funding stress and household-cost pressure between official releases. This helps investors identify when the macro narrative is changing before monthly data, policy decisions or market consensus fully reflect the shift.

What do the Turkey, Brazil and Nigeria signals show?

Turkey shows sticky inflation risk after the peak. Brazil shows how policy sentiment can track the central bank’s reaction function during an easing cycle. Nigeria shows how FX pass-through can keep inflation pressure live through the naira, fuel, food and import-price channels.

How can institutional investors use Global Macro Sentiment Indices?

Discretionary teams can use GMSI to monitor where macro pressure is forming across countries, regions and themes. Systematic teams can use point-in-time sentiment data for research, backtesting, model development, regime classification and portfolio-monitoring workflows without look-ahead bias.

How can investors access Permutable’s Global Macro Sentiment Indices?

Permutable is onboarding a limited number of EM and macro desks ahead of the official Global Macro Sentiment Indices launch. Institutional teams can request early access to preview sample indices, historical data and API access.

Analysis

07 Jul 2026

Testing GMSI US monetary policy sentiment as a short-end rates signal

Read more >

Analysis

01 Jul 2026

Global Macro Sentiment Indices: Turning point-in-time macro sentiment data into live systematic workflows

Read more >

Analysis

09 Jun 2026

Japan energy inflation is becoming a BoJ problem as JGB yields price inflation risk

Read more >