A quick guide to Permutable’s macro sentiment indices API for quantitative hedge fund strategies

07 May 2026

07 May 2026

This article examines how Permutable AI’s Macro Sentiment Indices API helps quantitative hedge fund strategies convert global news narratives into structured macro signals. Designed for quant hedge funds, systematic macro teams and institutional researchers, the platform combines local-language news analysis, historical traceability and real-time delivery to support macro research, cross-asset analysis and risk monitoring across FX, rates, commodities and sovereign markets.

Macro markets increasingly move on narrative shifts before official economic releases confirm the change. Inflation concerns, policy credibility, consumer stress and geopolitical tension often emerge first through local reporting and financial commentary, long before they appear fully in GDP data, CPI releases or central bank forecasts.

For funds running quantitative hedge fund strategies, this creates growing demand for real-time market intelligence APIs capable of transforming unstructured information into structured macro signals.

Permutable AI’s Macro Sentiment Indices API is designed to address that gap. Drawing from tens of thousands of international and local-language sources across more than 50 countries and 50+ languages, the platform converts global news narratives into continuously updated macro sentiment indices covering inflation, rates, GDP, employment, housing, manufacturing, fiscal policy and political risk.

The objective is not simply to measure positive or negative headlines. Our platform is designed to quantify how macroeconomic narratives build, diverge and evolve across countries and regions in ways that can support quantitative hedge fund strategies and institutional macro research workflows.

Traditional macroeconomic datasets remain central to investment research, but they are inherently delayed. Markets frequently reprice expectations before official releases are published.

Narrative-based data offers an additional layer of macro information. Changes in inflation expectations, for example, may first appear through:

Similarly, labour market weakness or fiscal stress may emerge in local reporting before it becomes visible in official statistics. For quantitative hedge fund strategies, this type of information can help identify shifts in macro conditions earlier within the cycle.

Permutable AI’s framework converts this narrative flow into structured indices suitable for:

Coverage spans more than 25 macroeconomic themes, including inflation, interest rates, employment, retail sales, manufacturing, housing, elections and geopolitical risk.

At Permutable, one of the more differentiated aspects of ourframework is the separation of domestic and international narrative coverage.

Domestic sentiment captures local-language reporting and on-the-ground economic discussion. International sentiment reflects how countries are perceived externally through institutional media coverage, sovereign risk narratives and global macro commentary.

The distinction matters because the two narratives can diverge materially.

Our analysis shows that countries such as Spain, Turkey and Poland display heavily domestic-led narrative structures, while countries including China and the United Kingdom show significantly larger international narrative influence.

For quantitative hedge fund strategies, this divergence can help identify:

This framework is particularly relevant for FX markets, sovereign debt, rates positioning and cross-country relative value analysis.

Permutable’s Macro Sentiment Indices are built from continuously updated local-language and international news datasets sourced from financial media, regional publications and institutional reporting across developed and emerging markets.

We apply a proprietary methodology designed to identify and track changes in macroeconomic narratives across countries, sectors and policy themes. Domestic and international datasets are maintained separately to preserve differences between local economic sentiment and externally traded market narratives.

To improve comparability across countries and varying news volumes, the indices are normalised and structured into consistent historical time series suitable for institutional research workflows.

The platform also maintains historical vintage datasets, allowing institutional investors to:

This is particularly important for quantitative hedge fund strategies where transparency, reproducibility and historical validation matter.

Additional information on methodology, coverage and integration is available on request for institutional research teams evaluating the dataset for systematic or discretionary macro applications.

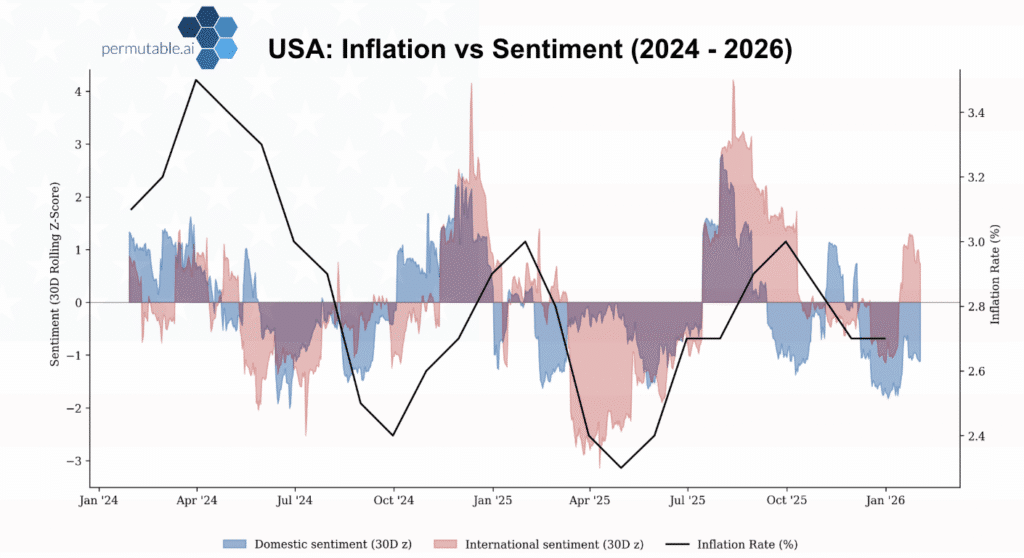

Our US macro sentiment indices illustrate how narrative signals can move ahead of traditional macro indicators.

Internal analysis comparing US inflation sentiment with core inflation shows that inflation narrative intensity rose sharply ahead of the 2021 to 2022 inflation surge and later weakened as disinflation pressures emerged.

Similarly, rates sentiment tracked changes in Federal Reserve policy expectations and broader Treasury market narratives through the tightening cycle. Additionally, GDP and consumer sentiment series also showed deterioration in narrative momentum during periods where growth expectations weakened.

Here, the purpose is not to replace traditional macroeconomic data, but to provide earlier visibility into narrative shifts and policy expectations. For quantitative hedge fund strategies, potential applications include duration positioning, yield curve analysis, inflation regime monitoring and FX macro positioning.

Above: Permutable’s US inflation sentiment chart comparing domestic and international narrative trends against inflation rates from 2024 to 2026. The visual highlights how local economic sentiment and internationally traded macro narratives can diverge during changing inflation environments, providing additional context for quantitative hedge fund strategies and macro risk analysis.

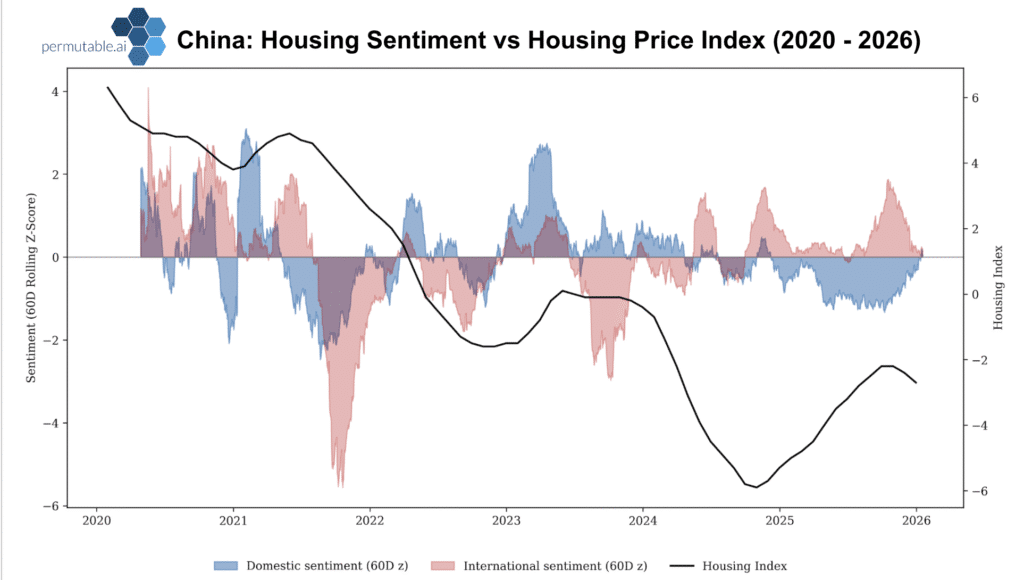

China’s property market provides a useful example of how domestic and international narratives can diverge significantly.

Permutable’s domestic housing sentiment series remained materially more constructive than international sentiment coverage during periods of property market stress. Domestic reporting focused more heavily on policy support measures, mortgage relief and housing stabilisation efforts. International reporting focused more on structural growth concerns, developer defaults and systemic macro risks.

For quantitative hedge fund strategies, this type of divergence can help identify:

Above: Permutable’s China housing sentiment chart comparing domestic and international macro narratives against the Housing Price Index between 2020 and 2026. The chart illustrates how local-language sentiment and international market perception diverged during China’s property market slowdown, offering additional insight for macro research and quantitative hedge fund strategies.

The value of our macro sentiment data is typically strongest when used alongside traditional economic and market datasets rather than in isolation. For institutional investors and teams building quantitative hedge fund strategies, the indices can support:

Because the data is available historically with point-in-time structure, it can also be incorporated into backtesting environments and signal validation workflows.

Markets increasingly react not only to economic data itself, but also to how economies are discussed, interpreted and repriced across domestic and international narratives. For institutional investors, the challenge is turning that information flow into something measurable, historically testable and operationally useful.

At Permutable, our Macro Sentiment Indices API provides a framework for doing that by combining local-language coverage, structured macro classification, historical traceability and real-time delivery into a dataset designed for modern macro research environments.

For firms developing quantitative hedge fund strategies, narrative-based macro intelligence is increasingly becoming a complementary layer alongside traditional economic and market data.

For institutional investors exploring quantitative hedge fund strategies, the practical challenge is not simply accessing more data, but operationalising macro narrative intelligence within existing research and portfolio workflows.

At Permutable, we work closely with macro, cross-asset and systematic investment teams demonstrating how our Macro Sentiment Indices can be integrated into:

For further examples of regional macro sentiment analysis and domestic versus international narrative divergence, to request a walkthrough of the platform, discuss methodology in more detail or explore how these signals could be operationalised within your investment process, get in touch with our team.

Analysis

29 Jul 2026

South Korea economy: the chip windfall is outrunning domestic growth

Read more >

27 Jul 2026

The tide turns on Russia inflation outlook as drone strikes spread from refineries to warehouses

Read more >

Analysis

27 Jul 2026

Saudi supply risk and import costs drive energy inflation sentiment higher

Read more >