China macroeconomic indicators and economic outlook 2026: Growth delivered, domestic demand still catching up

29 Jan 2026

29 Jan 2026

This article takes a closer look at what China macroeconomic indicators are signalling as the cycle turns into 2026. We set the official prints alongside regional macro sentiment indices to separate headline stabilisation from genuine improvement, and to gauge whether domestic confidence is building or still absent. It is aimed at macroeconomists, strategists and investors across rates, FX, equities and cross-asset allocation.

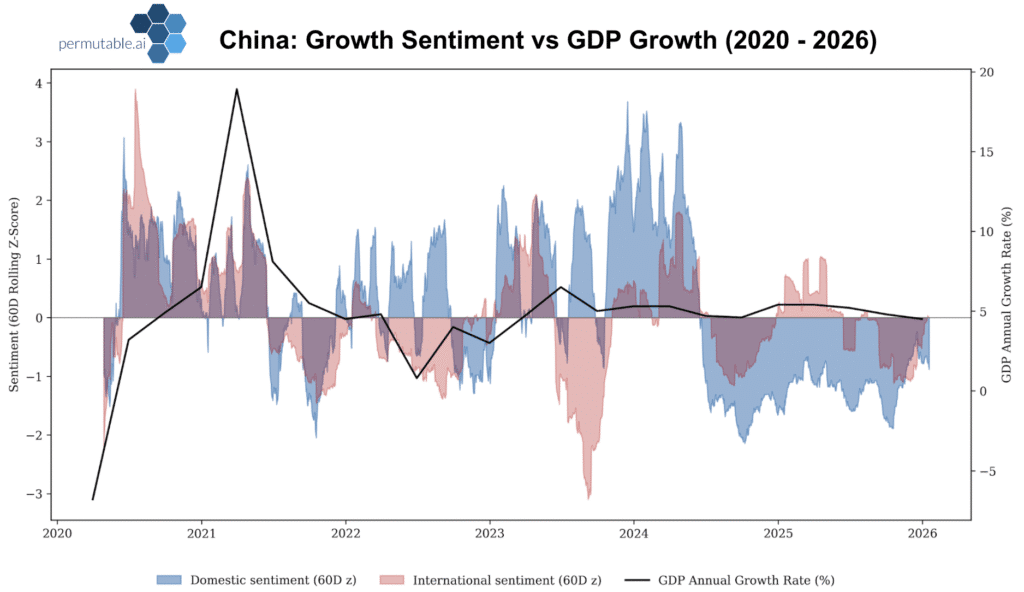

China hit its 5% growth target in 2025, exactly as Beijing intended. The more revealing question is what sat underneath that headline. Real GDP growth slowed to a three year low of 4.5% y/y in Q4, down from 4.8% in Q3. For the year as a whole, growth came in at 5.0%. The quarterly pace ticked up to 1.2% q/q, suggesting the economy is stabilising in places, rather than slipping into outright stall.

The headline figure is hard to look past. Yet the composition tells a different story. This is growth by shipment, not sentiment. Manufacturing and trade are doing the heavy lifting, while household demand remains subdued. Exports and policy are acting as stabilisers, but there is no broad based recovery in domestic conviction. That imbalance runs through output, consumption, housing and prices, and is where we start in our outlook for 2026.

Hard data tells you where the economy has been. Sentiment tells you where conviction is forming, or failing to form, in real time. Our sentiment-driven China macroeconomic indicators track narrative tone across domestic and international sources: what is being said, how loudly, and whether the narrative is turning.

The domestic series picks up household confidence, policy reception, and ground level conditions. The international series captures external perception, covering trade dynamics, supply chains, growth and geopolitics.

In our charting we smooth these signals, using rolling windows and normalisation techniques, so domestic and international reads sit on a comparable scale. What you get is a clean read on macro pulse through the sentiment lens, telling you what the hard data is unable to convey.

China finished 2025 exactly where Beijing wanted it on the scoreboard, but less comfortably on the pitch. Growth reached 5.0% for the year, though the tempo softened into year end. Q4 slowed to the weakest in three years. The composition matters more than the headline figure. Net exports did the heavy lifting, contributing an outsized share of growth as firms rerouted trade away from the US and into non-US channels to manage tariff disruption risk.

As we turn into 2026, the economy is far from crisis, but it is materially constrained. Growth is respectable on paper. The engines are narrow. The cycle depends on confidence holding up in trade flows and policy continuity, which is to say, things largely outside Beijing’s direct control.

GDP growth sits within the official comfort zone, but domestic growth sentiment trends lower and does not validate the headline. The result is growth that looks managed rather than self sustaining. According to our China macroeconomic indicators, international sentiment is steadier, which tells you how much of the stabilisation story is being carried by external momentum and policy continuity rather than anything happening on the ground domestically.

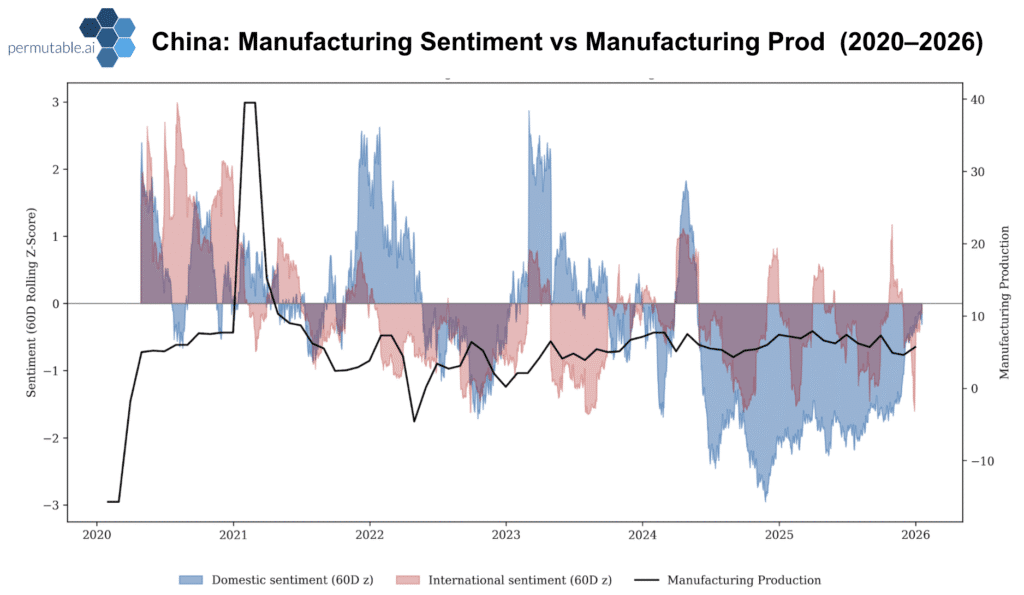

December brought a firmer industrial read, even as the domestic backdrop remains uneven. Manufacturing production growth accelerated to 5.7% y/y from 4.6% in November. Both the official PMI and Caixin PMI returned to 50.1, with production at 52.3 and new orders at 51.0. Trade was stronger than expected, with exports and imports both beating forecasts, and construction activity improved as targeted support began to show through.

This is export momentum doing enough to keep factories from shedding workers, plus a calmer trade temperature. It is not a domestic revival.

Factories on pace, households on pause. Output keeps ticking along, but it is not pulling domestic confidence up with it. The supply side is being propped up by policy, export competitiveness, and an external channel that is able to side step a tentative trade environment.

Manufacturing output has held up even as domestic manufacturing sentiment struggles to stay positive. International sentiment tracks the stronger phases more cleanly, reinforcing that exports and external demand are doing the work here.

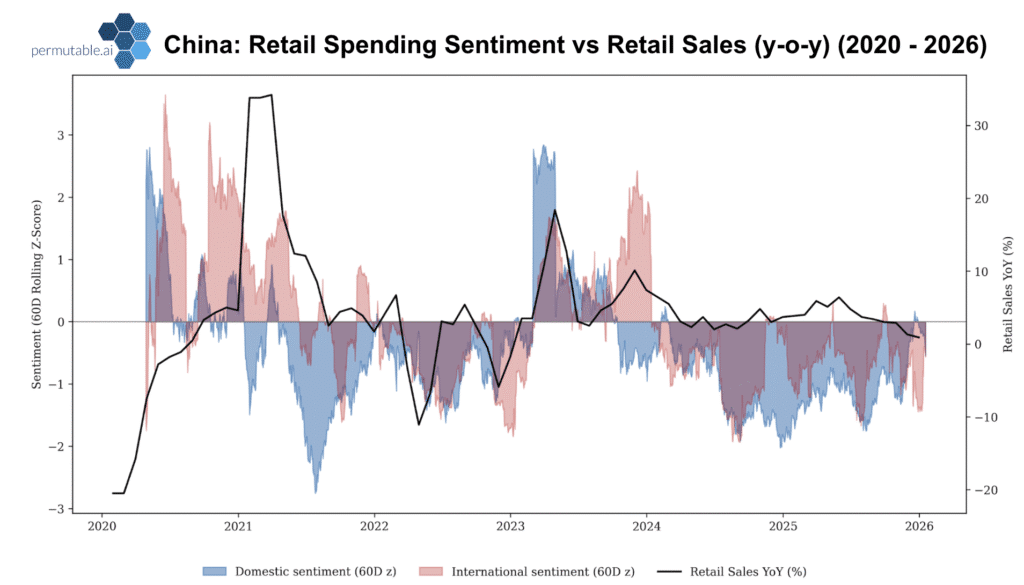

The demand side remains the Achilles’ heel. Confidence has edged higher over the past year but is still stuck at a low level, and household behaviour reflects that. The sugar rush from earlier consumer subsidies has faded. Nominal retail sales growth slowed to 0.9% y/y in December, with Q4 averaging around 1%, slipping to a post‑pandemic low from nearly 5% in June. This is not a classic sign of an economy growing at 5%, yet retail activity is struggling.

A growth print without a demand pulse. Spending remains cautious, easily spooked. The drag from housing, uncertainty around income prospects, weak wealth effects, have continued to linger. The readings are steady enough to avoid alarm, but too soft to generate a domestic lift.

Domestic retail sentiment stays persistently subdued and tends to weaken ahead of softer retail sales prints. Even when the hard data stabilises briefly, sentiment does not follow through. The high street still feels hesitant, and the narrative backs that up.

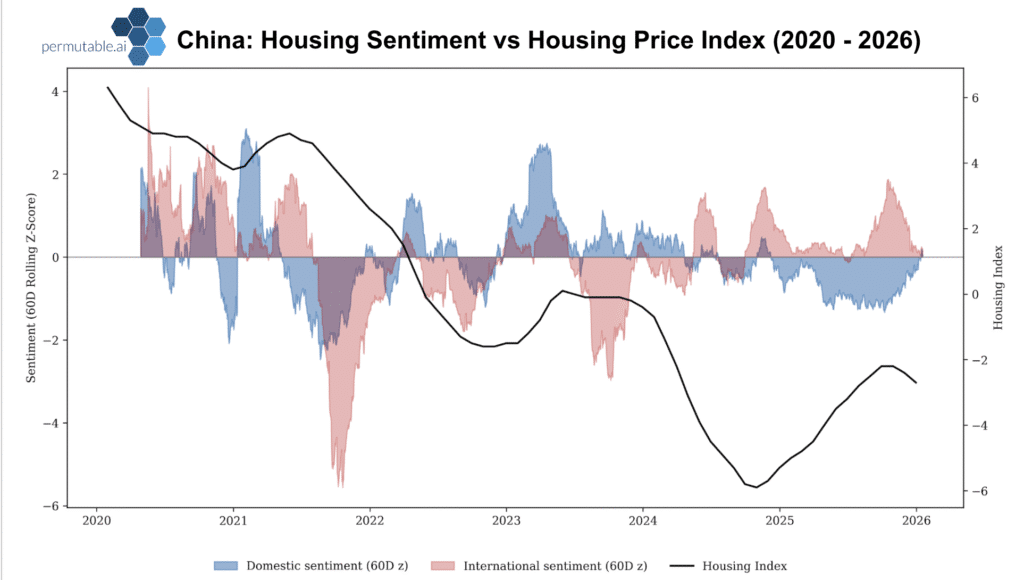

Property remains the stubborn drag underpinning everything else. In 2025, floor space of new commercial housing sold in China fell 8.7% y/y, with residential sales down 9.2% and sales value dropping 12.6%. That is compared against 2024’s severe downturn, so the actual picture is worse than it looks. The broader property sector continues to suppress confidence, spending, and investment. This is not a cyclical wobble. It is balance sheet repair, still incomplete, with households and developers both acting defensively.

In China, this matters enormously, because property is where the wealth effect used to live, and where consumption momentum went to die.

Housing sentiment remains structurally negative, with only brief moments of picking up around supportive policy. Policy can slow the fall. It has not rebuilt conviction among households or developers, and there is little sign it will anytime soon.

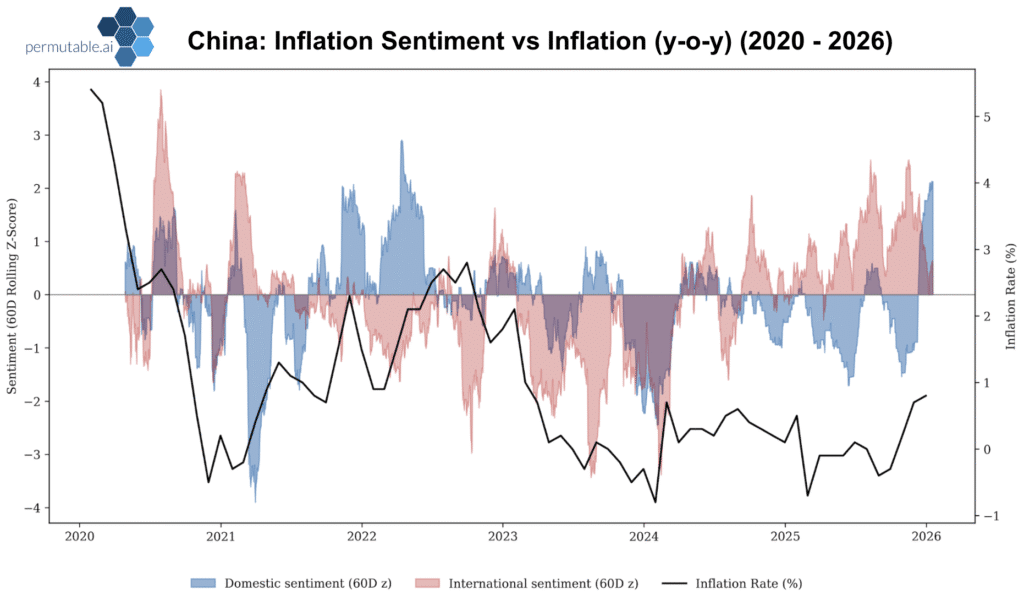

Price dynamics are edging in a more comfortable direction, though they have not flipped the cycle. CPI moved from -0.3% y/y in September to +0.8% in December its highest since 2023, helped by improving core inflation, and higher food prices after a long stretch of declines. Producer prices remain in deflation territory, hovering at -1.9% y/y in December. Thin pricing power, excess capacity, tell the story of a lack of demand and rife competition.

There are signs of hope. Policy measures aimed at curbing cut throat competition could temper some of the more aggressive price discounting. But without a stronger domestic demand impulse, firms are pricing for survival, not strength. It remains difficult for firms to regain durable pricing power, and harder still for households to believe inflation is returning as a permanent feature rather than an episodic blip.

Our sentiment-driven China macroeconomic indicators shows that inflation sentiment stays swayed towards disinflation, which aligns with weak pricing power and subdued demand expectations. Occasional base effect firming has not translated into any shift in underlying confidence in a reflation story.

As we embark into 2026, growth is still being kept on track by trade and targeted easing, the policy playbook is unlikely to involve a grand stimulus moment. The more likely path is continued incremental support, with the emphasis shifting from consumption nudges towards investment and construction linked channels, plus small steps on the monetary side via policy rate and RRR cuts.

The risk, of course, is that the external environment stops being such a willing co-star. The US China truce has held, but it is fragile, the kind that depends on everyone choosing not to test each other’s limits. Fresh tariff threats and wider geopolitical frictions keep the risk pulse alive, especially with the US targeting Iran oil, a key import for China.

From a sentiment perspective, this matters because the current growth mix is disproportionately reliant on confidence staying intact in trade flows and policy continuity. If the narrative around China macroeconomic indicators turns, the economy has less domestic momentum to fall back on.

Additionally, with Beijing applying policy ointment to the demand side, incremental impetus to lift consumption will only happen gradually. Policy can slow the fall, but it has not yet rebuilt conviction.

That matters, because external conditions are still doing the line share of meeting growth targets. When the domestic engine has idled for this long, sharper swings in trade confidence or geopolitical tone can quickly undermine the key pillars supporting growth.

Assuming the trade truce largely holds and targeted support continues to work through the economy, growth should stabilise in early 2026, even if the drivers are running at two speeds. On that basis, expect full year GDP growth to sit around 4.5% in 2026.

China’s 2026 outlook rests on a key set of pillars. The growth impulse is still being carried by exports and policy continuity, not a broad domestic rebound. If external conditions turn less forgiving, tariff risks return, geopolitics heats up, or the truce frays, the buffer thins quickly and downside risks step back to the forefront.

This is precisely where our regional macroeconomic sentiment indices act as the market’s heartbeat. They separate stabilisation from real improvement by showing whether domestic conviction is strengthening ahead of the prints or slipping behind them.

Our regional sentiment-driven macroeconomic indicators can flag turning points before official data confirms them. For asset allocation, they are an early warning for regime shifts: is China still a growth story, or now a policy story? Is trade a tailwind, or a shock risk? The domestic and international split shows whether momentum is broadening or narrowing, and whether the impulse is internal or externally driven.

This is where the regional macro sentiment indices add edge, by tracking the divergence between sentiment and the data before it shows up in positioning.

For Clients, our suite of regional macro indices helps support cleaner regime reads, relative value selection, and risk monitoring.

For institutional access to our China Sentiment Indices and integration with your macro portfolio contact us at enquiries@permutable.ai

Analysis

04 Aug 2026

Global industrial production sentiment: Canada, India and South Korea Gain as the UK, Germany and China weaken

Read more >

Analysis

30 Jul 2026

US growth and policy outlook Q2 2026: Q2 bought the Fed time. July may take it back

Read more >

Analysis

29 Jul 2026

South Korea economy: the chip windfall is outrunning domestic growth

Read more >