China economic growth outlook 2025: Stability on paper, strain beneath the surface

02 Oct 2025

02 Oct 2025

In this article, we explore China’s path in 2025, marked by headline figures that on the surface appear solid. GDP growth in the first half of the year held close to 5%, industrial production expanded at a steady pace, and domestic equities staged a rally. These outcomes enabled policymakers to project confidence that the official growth target would once again be met.

Beneath the surface, however, the story is mired in a less convincing narrative. Our China macro sentiment indices show that households, firms, and investors are far more cautious than the data alone suggests. Confidence has been eroded by a property market still in reprise, dubious household demand, persistent manufacturing overcapacity, and renewed tariff frictions with the US.

Taken together, the hard data and sentiment reveal a familiar pattern: China’s economic growth outlook in 2025 looks much like China in 2024. Growth is being delivered, but it is skewed, driven by state-supported manufacturing and exports, while property, consumption, and private-sector investment remain tentatively wrapped in fragility and unshared prosperity. Our market sentiment captures these narratives with conviction, adding an additional lens to see the drivers and outlook more sharply than the official numbers.

The property downturn continues to exert the heaviest drag on domestic demand. In H1 2025, real estate investment fell by –11% y-o-y, worse than last year’s contraction. New starts dropped -16% and completions -15%, confirming that developers are still drawing down on unsold inventories rather than kick starting new projects.

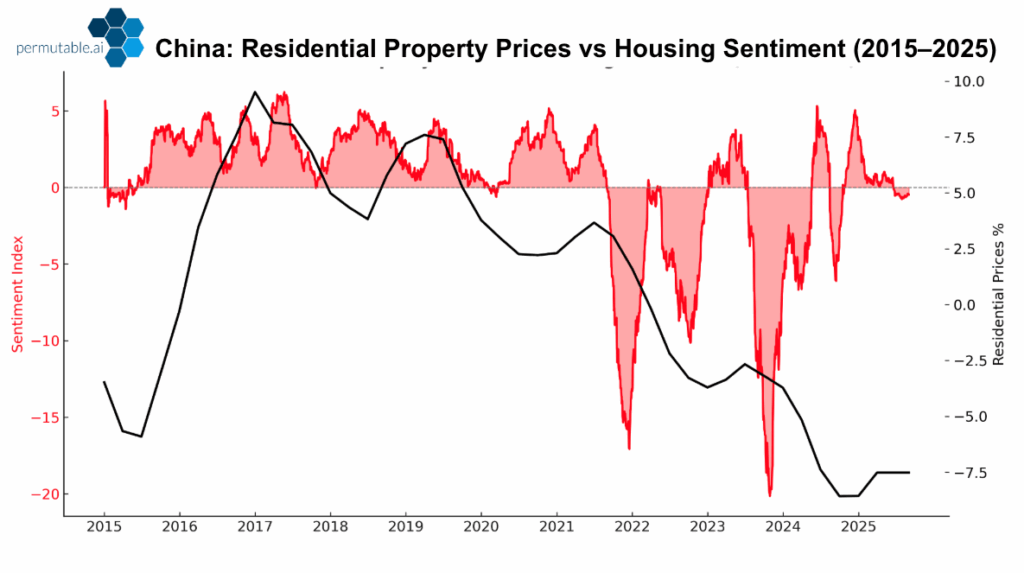

Residential prices have continued to slide through 2024 and into 2025, sitting at -7% y-o-y in March, with buying interest waning. Households no longer expect an uptick in property appreciation, and each targeted policy measure, whether mortgage easing or credit lines to developers, has produced only an episodic bounce in sentiment before being reversed by renewed weakness and unease in the sector.

Our China Housing Sentiment Index exhibits this trend, it has remained firmly negative since early 2024, tracing residential prices closely. Both sentiment and the hard data show persistent weakness with no signs of long-run stabilisation. The sector’s inability to make a notable recovery has played a critical burden on household confidence, unwilling to part with savings to invest in property against the sector’s depressed backdrop, weighing heavily on the broader economy.

This matter goes well beyond housing. Property weakness erodes household wealth, restrains consumption, detracts from local government tax revenues, and reduces upstream demand for construction-linked industry. The property sector sits at the centre of China’s macro malaise and demand demise. What is evident is that both the data and the sentiment indices highlight the absence of a sustained turnaround.

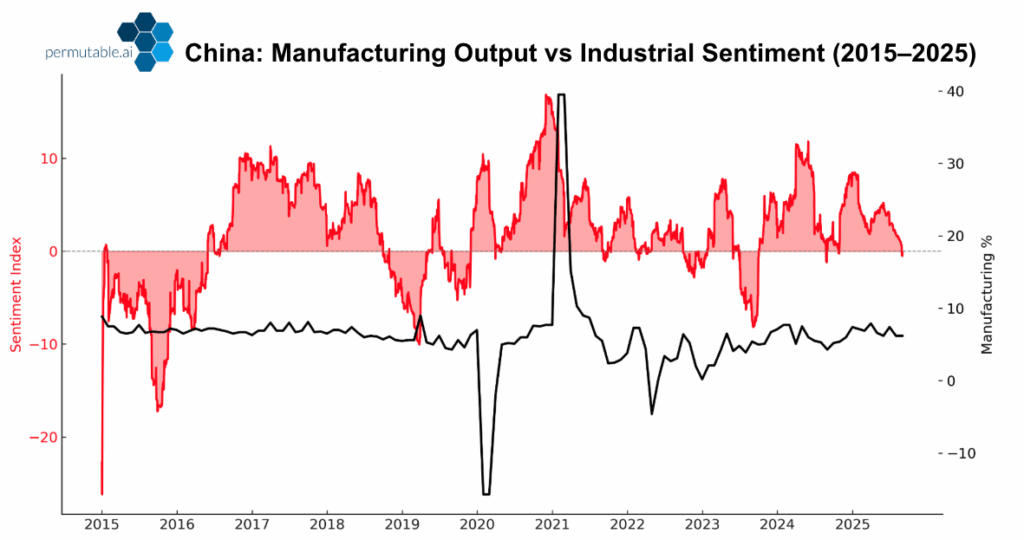

Manufacturing output has continued to expand. In August, production rose 5.7% y-o-y, supported by strategic industries such as EVs, shipbuilding, and high-end equipment where subsidies and fiscal support remain extensive. On paper, this suggests resilience.

But sentiment tells a different story. Our China Manufacturing Sentiment Index peaked in early 2024 and has been declining ever since. It fell further in 2025 as new US tariffs hit consumer electronics and labour-intensive exports, while property-driven overcapacity depressed demand for steel, cement, and machinery.

The divergence between solid output growth in manufacturing and weakening sentiment suggests markets view current strength as brittle, reliant on subsidies and front-loading ahead of tariffs rather than sustainable demand.

Over the past two years, this pattern has crystallized. The latest prints have been steady, propped up by state support and getting ahead of oncoming tariffs. Sentiment, however, has been broadly positive but the current trend of decline with fleeting jumps since mid-2024, echoes the doubts over durability, tariff risks, and producing over capacity to hit target could prove short-lived. Manufacturing output looks resilient, but the prevailing perception is that today’s growth will turn into tomorrow’s glut, pushing more goods into foreign markets at discounted prices. The effect of this could lead to more protection from importers to safeguard domestic industry as seen in the European EV sector.

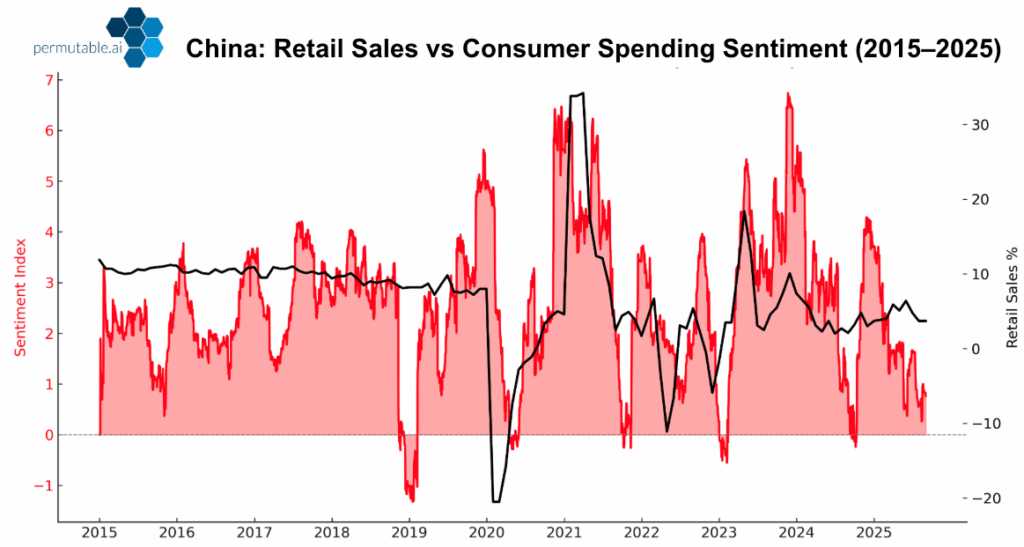

Beneath the resilience of the industrial base, household demand has continued to lag. Consumption remains subdued despite repeated policy interventions. Retail sales recorded modest gains in early 2025, supported by trade-in programmes, subsidies for household appliances, and a lift from affordable luxury purchases such as jewellery and fitness products. Yet these improvements have been narrow, short-lived, and heavily policy-driven, emphasising the persistent softness in domestic demand.

The government has placed increasing emphasis on this channel of support. In March 2024, Beijing launched an action plan for large-scale equipment renewal and consumer goods trade-in, designed to stimulate demand and encourage households to upgrade durable goods. With policymakers doubling down on this strategy, reinforcing the pledge by earmarking 81bn yuan through the transmission of ultra-long treasury bonds.

The expansion of the trade in program is aimed to offer subsidies across sectors for consumer trade in areas such as electronics, high-end intelligent equipment, and agriculture. The intentional position to lift consumption and domestic demand through state-backed renewal cycles, has undertones of propping up an economy lingering in malaise.

Yet our China Retail Sales Sentiment Index shows that households remain cautious over the last year. Sentiment has been modestly positive since mid-2024, with visible upticks in holiday periods but is retreating as of late. Weak income expectations, limited wealth effects from housing, subdued income and cooling labour market conditions continue to bear a burden on confidence.

The divergence between policy-driven consumption and sentiment is telling. While retail sales growth can be manufactured through subsidies and trade-in programmes, households are not yet convinced by the recovery. Without a stabilisation in property and stronger income growth, spending momentum will remain fragile, and retail sentiment highlights that consumption is unlikely to become a self-sustaining engine of growth unless underlying fundamentals change.

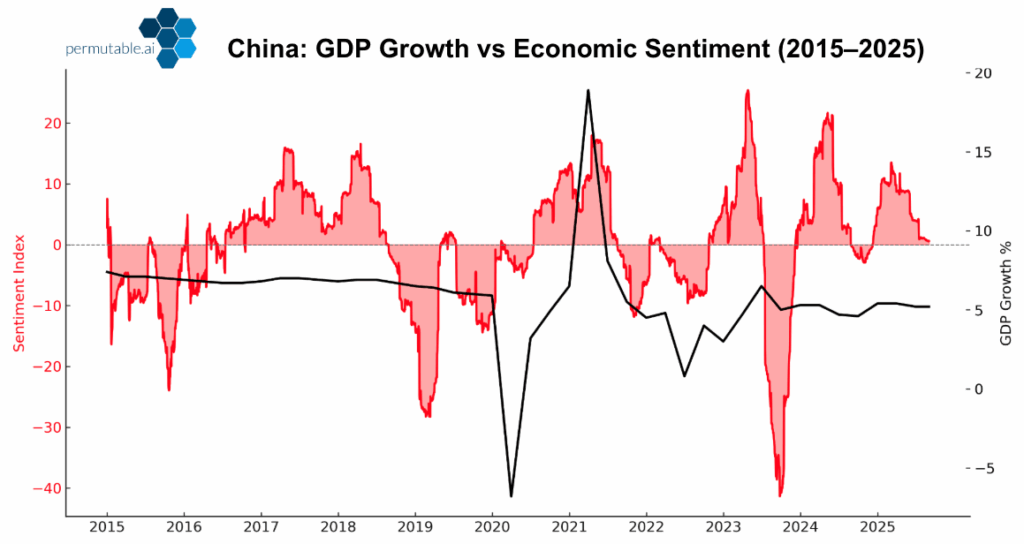

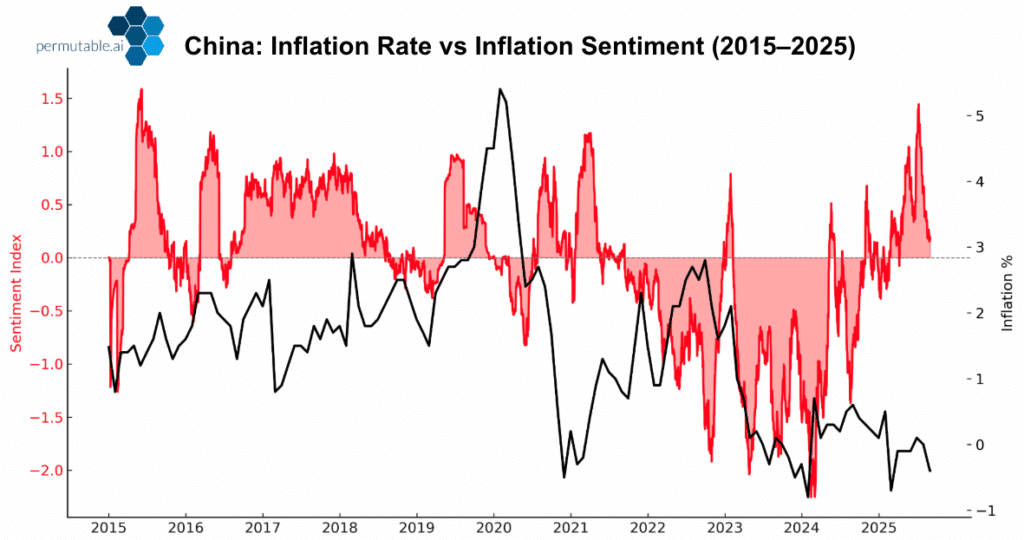

Moving to growth, China GDP continues to hold its course in and around 5%, a remarkable reoccurring feat, underpinned by manufacturing and exports momentum, whilst attributing to a pivot from consumer goods to high-end manufacturing. Yet our China GDP Sentiment Index reveals a degree of volatility. Over the past two years, sentiment has swung sharply with the policy and trade cycles. Optimism in early 2024, sharp pessimism later that year as tariff risks returned and property weakness deepened, and now a sharp turn around in sentiment in 2025.

While the growth figures appear on firm footing, sentiment reveals the fluctuation in confidence cycle that defines China’s economic growth story today. At present, the sentiment is reeling in, becoming less positive, as the cracks are appearing, painting a picture of renewed pessimism in the growth path. What this suggests is that markets, industrial base and households are once more losing faith in the recovery, even as the growth target is being met.

Exports remain central to absorbing China’s industrial overcapacity. But China trade numbers show growing distress. The early-2025 boost from front-loading ahead of tariff deadlines has faded, loopholes are being closed, and exports to the US have fallen off a cliff in August, sliding -33%. Export growth has stalled to its weakest in six months, cracks are emerging as the deterioration in shipments drags on. The focus for Chinese exports has shifted to Europe and the rest of Asia in order to claw back a recovery.

Unlike 2019 trade tension, rerouting options have hit a bump in the road. The US has tightened its grip on trade agreements with China’s close partners, targeting re-exported Chinese goods and closing off many of the channels that once allowed exporters to bypass tariffs. As a result, only a small fraction of lost exports to the US have been redirected via Mexico or ASEAN economies. With partners unwilling to be drawn into proxy battles, the buffer that once was, has dissipated.

This shift is visible in our sentiment data. Markets no longer assume that rerouting can soften the blow, and our regional macro indices point to growing concern that China’s surplus output will meet greater resistance abroad, fuelling deflationary pressures and geopolitical friction.

Yet the broader picture is not wholly one of gloom. In the short term, Chinese exporters continue to compete effectively on price, leveraging technological upgrading, scale efficiencies, and state-backed investment to preserve the exporting base. Tariffs, in many cases, have proved less disruptive than feared, in essence more of a periodic paper tiger than looming threat. Over the longer term, the sheer depth of China’s manufacturing base and its relentless push into advanced technologies may underpin renewed competitiveness, with potential to shift sentiment more positively if innovation begins to offset the drag from trade barriers.

The central government has set its largest deficit target in decades, but most of the funds will be absorbed by local fiscal shortfalls and state-backed firms. With austerity persisting at the local level, the growth impulse will be limited.

On the price front, deflationary pressures are entrenched, with August inflation at -0.4% y-o-y and flat on a m-o-m basis. Higher global energy costs from geopolitical tensions have not fed through domestically, where weak demand, falling food costs and overcapacity continue to suppress inflation pressures. Sentiment indices confirm this, pointing to expectations of further price weakness and doubts over policymakers’ ability to reignite demand.

Looking forward, the combined picture from data and sentiment points to three enduring themes:

What we do know is that China will hit its 5% growth target again in 2025, but the quality of growth will remain modestly skewed, carried by core sectors. For households, conditions will still feel mired in pessimism; for private firms, margins will remain squeezed; and for global trade partners, the continued flow of cheap exports will uphold growth but sustained could add to further friction owing to the implications on domestic producers. By using sentiment, our regional macro indices capture the outlook more clearly than just observing official data.

China’s economic growth story in 2025 mirrors the patterns of 2024, but with slight inflections. Property remains in retreat, manufacturing continues its robust run, household demand remains subdued, and deflationary pressures persist. But what has changed is the clarity with which sentiment captures these dynamics.

Our China macro sentiment indices offer more than a measure of mood, they provide a sharper lens on the economy’s underlying condition. Where official data smooths the edges, sentiment exposes the fragility, the scepticism, and can add conviction behind the headline numbers.

In this sense, sentiment functions as the economy’s heartbeat, capturing shifts in confidence that official statistics often smooth away. It is not merely a reflection of mood, but a lens on what is happening beneath the surface, an early signal of strain long before the data reveal it.

See how our China Sentiment Indices work in practice: request a demo at enquiries@permutable.ai

Analysis

30 Jul 2026

US growth and policy outlook Q2 2026: Q2 bought the Fed time. July may take it back

Read more >

Analysis

29 Jul 2026

South Korea economy: the chip windfall is outrunning domestic growth

Read more >

27 Jul 2026

The tide turns on Russia inflation outlook as drone strikes spread from refineries to warehouses

Read more >