How our real-time Brent crude intelligence signalled a shift in ceasefire sentiment before the oil selloff

06 May 2026

06 May 2026

This case study explores how Permutable’s real-time Brent crude intelligence identified a reversal in ceasefire and de-escalation sentiment before Brent crude sharply repriced geopolitical risk. Designed for hedge funds, commodities traders, and macro research teams, the article examines how narrative intelligence and source-traceable sentiment analysis are reshaping institutional energy trading workflows.

Brent crude’s sharp reversal this week did not begin with price action. It began with a shift in geopolitical narrative momentum that markets started repricing hours before the broader selloff accelerated.

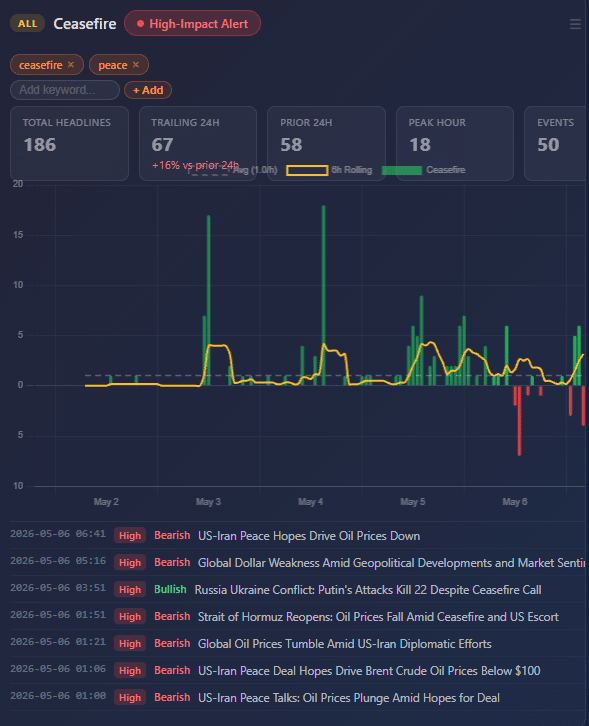

At Permutable, our customised 24-hour Brent crude sentiment tracker identified the first clear reversal in ceasefire-related sentiment before midnight on 5 May, well before crude moved sharply lower during the morning session.

At that stage, peace-deal headlines, Hormuz de-escalation narratives, and weaker disruption-risk signals had already begun clustering across the market. The tracker showed Brent’s read-through shifting away from supply-risk escalation and toward geopolitical risk-premium unwind before the move became fully visible in futures pricing.

By the time the broader repricing appeared on trading screens, narrative conditions inside the market had already changed materially.

Above: Permutable AI’s customised Brent crude sentiment tracker identified a sharp reversal in ceasefire and de-escalation narratives before oil markets rapidly unwound geopolitical risk premia.

Beneath the surface, Permutable’s system identified several important transitions developing simultaneously:

The move that followed reflected a rapid unwind of geopolitical risk premia across oil markets.

Reports of paused US Strait operations, alongside growing optimism around a potential US-Iran agreement, changed how traders assessed near-term supply disruption probabilities. As those narratives strengthened, Brent crude rapidly repriced lower.

At one stage Brent briefly approached the $98 level as markets aggressively reduced exposure linked to escalation risk.

The selloff was not caused by one headline alone. Instead, the move developed through the accumulation of multiple de-escalation signals entering markets simultaneously:

This distinction matters because modern commodities markets increasingly trade on changing probability distributions rather than static fundamentals alone.

That is precisely the reason we have been seeing institutional demand for Permutable’s real-time Brent crude intelligence accelerating across macro hedge funds, systematic, commodity and energy trading desks.

The market is no longer simply reacting to whether supply is tight or loose. It is continuously repricing the probability of future disruption scenarios. In this case, the system isolated the dominant driver clearly. This was not generic oil-news weakness. It was a ceasefire-driven repricing of geopolitical risk.

One of the more important aspects of this week’s move is that the underlying physical backdrop remained relatively supportive throughout the selloff.

Large inventory draws, constrained supply conditions, and persistent structural tightness continue to sit underneath the market. Under different geopolitical conditions, those factors could easily have pushed crude higher.

But markets temporarily prioritised diplomatic momentum over physical scarcity. That divergence highlights how oil markets increasingly behave during periods of geopolitical volatility. In practice, sentiment can overpower fundamentals in the short term, particularly when positioning becomes heavily concentrated around a single macro narrative.

Many conventional commodities research workflows still rely heavily on static news monitoring, delayed analyst interpretation, or document-level sentiment scoring. The problem is that narrative transitions rarely happen cleanly.

They emerge gradually through thousands of interconnected signals before becoming consensus positioning. By the time the narrative appears obvious through price action alone, a large portion of the move may already be complete.

During this Brent reversal, sentiment progressively rotated away from:

toward:

The reversal itself began before midnight, long before ceasefire optimism became the dominant market narrative during the following trading session.

In our view, this is one reason first-generation sentiment systems increasingly struggle during periods of geopolitical stress. Many remain overly dependent on isolated document scoring and fail to capture how narratives evolve collectively across markets.

This case study reflects a broader structural shift taking place across commodities and macro trading.

We are already seeing institutional investors are moving beyond simple positive or negative sentiment classification toward systems of the kind we have built here at Permutable capable of modelling:

The distinction is important.

Modern commodities markets increasingly move in stages:

For systematic trading teams, the challenge is identifying those narrative transitions before they become consensus market positioning.

That requires more than headline ingestion. It requires infrastructure capable of understanding how narratives spread across entities, regions, policy developments, and macro assets simultaneously. At Permutable, our real-time Brent crude intelligence is increasingly becoming part of that workflow.

The recent Brent reversal is a useful reminder that oil markets increasingly function as geopolitical probability markets layered on top of physical supply dynamics. Inventory data still matters. Supply discipline still matters. Physical tightness still matters.

But short-term price discovery is increasingly dominated by how quickly markets reassess future geopolitical outcomes. That reassessment process now happens at machine speed.

For macro systematic funds, commodities trading desks, and cross-asset research teams, the ability to monitor narrative momentum in real time is becoming increasingly important for:

The firms likely to adapt fastest are not necessarily those consuming the most headlines. They are more likely to be those capable of identifying narrative inflection points before those shifts fully propagate through markets.

For Brent crude specifically, the shift was unusually clear:

At Permutable, we provide source-traceable narrative intelligence and real-time sentiment infrastructure for institutional trading and research workflows across commodities, macro, FX, rates, and digital assets.

Our platform supports:

Our custom real-time Brent crude intelligence sentiment trackers allow trading teams to monitor the narratives that matter to their book, configure targeted alerts, and identify when market-moving themes begin to turn in real time.

To request a walkthrough of our real-time Brent crude intelligence or discuss trial access, contact the team at enquiries@permutable.ai.

Analysis

27 Jul 2026

Saudi supply risk and import costs drive energy inflation sentiment higher

Read more >

Analysis

15 Jul 2026

The Price of Passage: How Geopolitical Sentiment Led the Repricing of Gulf Crude-Flow Risk

Read more >

Analysis

22 May 2026

Brent volatility: Tracking Brent’s three-month sentiment shift

Read more >