Best news-to-signal APIs for hedge funds and quantitative investment strategies in 2026

20 Apr 2026

20 Apr 2026

This article examines the leading real-time news-to-signal and sentiment intelligence APIs used by hedge funds in 2026, comparing providers across macro, commodities, and FX workflows. It is aimed at quant researchers, systematic trading teams, and institutional data professionals evaluating low-latency, explainable market intelligence infrastructure for quantitative investment strategies and cross-asset trading environments.

Systematic hedge funds are no longer competing on access to information alone. The competitive edge increasingly comes from how quickly firms can transform unstructured global events into structured, tradable signals suitable for quantitative investment strategies.

That shift has accelerated demand for alternative data and sentiment intelligence APIs for hedge funds, particularly across commodities, FX, and macro trading workflows where geopolitical developments, central bank rhetoric, and supply disruptions can move markets within seconds.

In 2026, the market for real-time market intelligence APIs is far more mature than it was even two years ago. Traditional news analytics providers are now competing with LLM-powered narrative intelligence platforms capable of modelling relationships across entities, markets, and macro themes in real time.

For hedge fund researchers and data teams, the challenge is no longer finding information. It is identifying which APIs can deliver signal integrity, low latency, point-in-time consistency, and explainable outputs that hold up in both research and live production environments.

The rise of automated macro trading and quantitative investment strategies has fundamentally changed how institutional firms consume news and alternative data.

A raw news feed is no longer enough. Hedge funds increasingly require structured outputs that integrate directly into research pipelines, portfolio models, and execution systems. In practice, that means modern news-to-signal macro trading APIs are expected to provide millisecond-level event detection, historical replay capability, point-in-time reconstruction, and traceable signal generation.

This has become especially important in commodities and FX markets, where macro narratives can propagate across assets rapidly and unpredictably.

Several buy-side teams have discovered that historical sentiment archives can diverge subtly from live production feeds. In some cases, cleaned or backfilled datasets created misleading backtest results that failed to replicate in live trading. That issue has pushed institutional firms to scrutinise how vendors manage historical reconstruction and revision handling.

Operational reliability has also become more important. During periods of geopolitical volatility, some APIs may experience schema inconsistencies, delayed event propagation, or throttling issues precisely when systematic models require stable delivery.

The providers gaining traction are those capable of explaining not only what happened, but also why it mattered across connected macro narratives.

At Permutable, we are a relatively new entry to the space and as such, one of the more differentiated providers in commodities and FX alternative data feeds, particularly for quantitative investment strategies focused on macro and geopolitical intelligence.

Unlike traditional sentiment data vendors that rely heavily on document-level scoring, at Permutable AI, our focus is on source-traceable narrative intelligence and event causality modelling. Its platform is designed to convert geopolitical developments, central bank commentary, supply chain disruptions, and macroeconomic shifts into structured signals in real time.

One of our platform’s defining characteristics is its multi-entity modelling architecture. For macro systematic desks, this is increasingly important because market reactions rarely remain isolated within a single asset class. An oil supply disruption may simultaneously influence inflation expectations, FX markets, sovereign risk, and industrial equities.

Through our API, we also ensure point-in-time consistency. Researchers can reconstruct signals exactly as they appeared historically, which is vital for quantitative investment strategies attempting to avoid hidden lookahead bias.

This is an area where some first-generation sentiment platforms still face criticism. Several systematic teams report that historical archives do not always perfectly replicate how signals appeared live, particularly during periods of fast-moving geopolitical developments.

At Permutable AI, our positioning as a leader of LLM-powered narrative intelligence is also notable. Rather than simply assigning positive or negative scores to individual documents, our system attempts to model evolving market narratives and identify how sentiment propagates across related entities and macro themes.

For commodities and macro funds, this approach is increasingly relevant during periods where policy shifts and geopolitical developments dominate cross-asset price action.

RavenPack remains one of the most established sentiment data vendors serving institutional finance.

The company has spent years building a mature event and entity analytics ecosystem widely adopted across quant equity and event-driven workflows. Its strengths remain broad market coverage, structured event classification, and deep historical archives.

For many quantitative investment strategies, particularly in equities, RavenPack continues to provide reliable sentiment and event infrastructure integrated into existing research environments.

Bloomberg remains deeply embedded across institutional trading infrastructure.

For discretionary macro desks and multi-asset hedge funds, Bloomberg continues to serve as the operational backbone for pricing, news, research, and execution workflows. Its breadth and reliability remain difficult to match.

That said, Bloomberg’s strengths are integration and global coverage rather than specialised narrative intelligence or low-latency news-to-signal delivery. Leading systematic firms are now beginning to supplement Bloomberg infrastructure with more specialised alternative data and sentiment intelligence APIs for hedge funds focused on quantitative investment strategies.

AlphaSense has become increasingly popular among discretionary and hybrid research teams.

The platform’s strengths lie in transcript analysis, document discovery, and AI-assisted search across filings, earnings calls, and broker research. It has benefited significantly from institutional interest in generative AI research workflows.

For quantitative investment strategies, however, AlphaSense is generally more valuable as a research augmentation layer than as a production-grade low latency signal API. Its capabilities are strongest in thematic analysis and information retrieval rather than real-time event intelligence.

Polygon.io continues to gain traction among systematic trading teams focused on low latency infrastructure.

The platform specialises in real-time delivery across equities, options, forex, and crypto markets. Many firms use Polygon.io as the streaming infrastructure layer within broader quantitative investment strategies.

While it is not primarily positioned as a sentiment intelligence provider, it is often paired with narrative intelligence APIs to create integrated event-driven trading architectures.

For teams prioritising developer flexibility and streaming performance, Polygon.io remains a strong infrastructure-focused option.

One of the clearest trends in 2026 is the institutional demand for explainability.

Hedge funds increasingly want to understand not just whether sentiment changed, but what caused the change and how the narrative evolved over time. That is particularly important for quantitative investment strategies operating in macro and commodities markets where causality matters more than isolated headline sentiment.

This is where LLM-powered narrative intelligence platforms are beginning to differentiate themselves from earlier generations of sentiment analytics.

The ability to trace signals back to source events, identify causal relationships, and reconstruct evolving narratives is becoming increasingly valuable across systematic macro trading.

The best alternative data and sentiment intelligence APIs for hedge funds ultimately depend on strategy design, infrastructure priorities, and workflow requirements.

Equity-focused quant funds may prioritise mature event classification and broad historical coverage. Macro systematic desks may care more about narrative propagation, geopolitical intelligence, and cross-asset relationships. High frequency trading teams may focus primarily on latency stability and streaming resilience during volatile market conditions.

But what is increasingly clear is that institutional demand has moved well beyond basic news aggregation.

The providers leading the market in 2026 are those capable of transforming fragmented global information into explainable, low latency, and backtest-ready signals suitable for modern quantitative investment strategies.

To explore how our source-traceable sentiment intelligence and real-time macro APIs support quantitative investment strategies, contact our team at enquiries@permutable.ai to request a platform walkthrough or discuss trial access tailored to your research and trading workflows.

Analysis

09 Jun 2026

US inflation trends are proving stubborn – our Global Macro Sentiment Indices maps the pressure beneath them

Read more >

Guide

07 Jun 2026

Oil market sentiment analysis: turning narrative flow into signals

Read more >

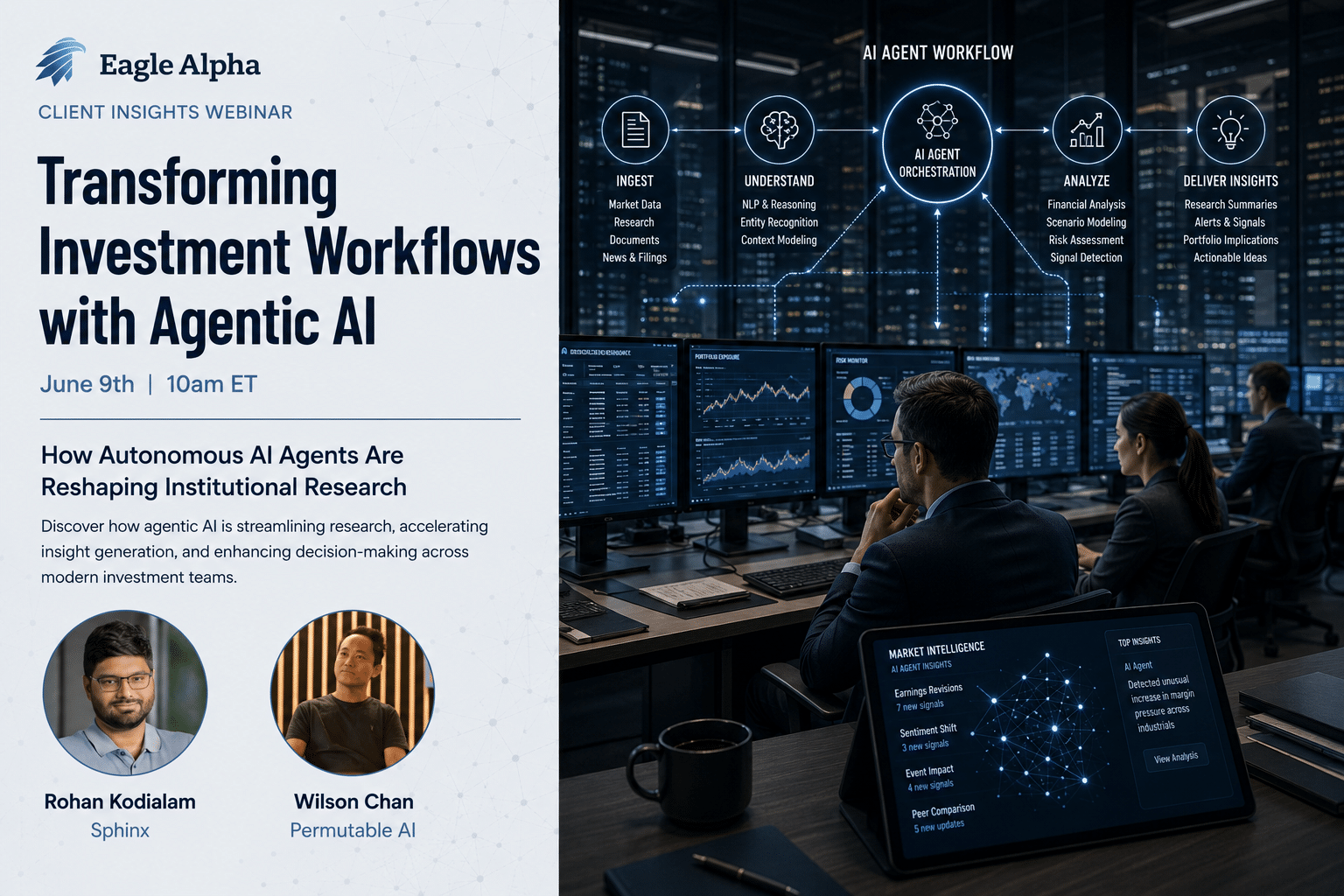

02 Jun 2026

Permutable joins Eagle Alpha webinar on the future of agentic AI and market intelligence

Read more >