Real-time macro intelligence – the missing layer in quantitative investment strategies

10 Apr 2026

10 Apr 2026

This article explores how real-time macro intelligence is transforming quantitative investment strategies by turning unstructured global information into actionable signals. It explores how Permutable AI converts narrative into structured, model-ready intelligence, enabling earlier positioning and improved decision-making. Aimed at hedge funds, quant teams, and institutional investors, it addresses the growing need for forward-looking, real-time market insight.

Quantitative investing has always been about one thing – finding signal before the market does. For decades, that signal came from structured data. Prices, volumes, and economic releases formed the backbone of most quantitative investment strategies. These inputs were reliable, testable, and scalable.

But markets have changed. Today, price formation is increasingly driven by information that sits outside traditional datasets – policy signals, geopolitical developments, and rapidly evolving narratives. By the time these forces appear in structured data, they are often already reflected in price. This has created a structural gap:

Quantitative models are still trained on what is measurable – while markets are moving on what is interpretable.

Our real-time macro intelligence is the layer designed to close that gap.

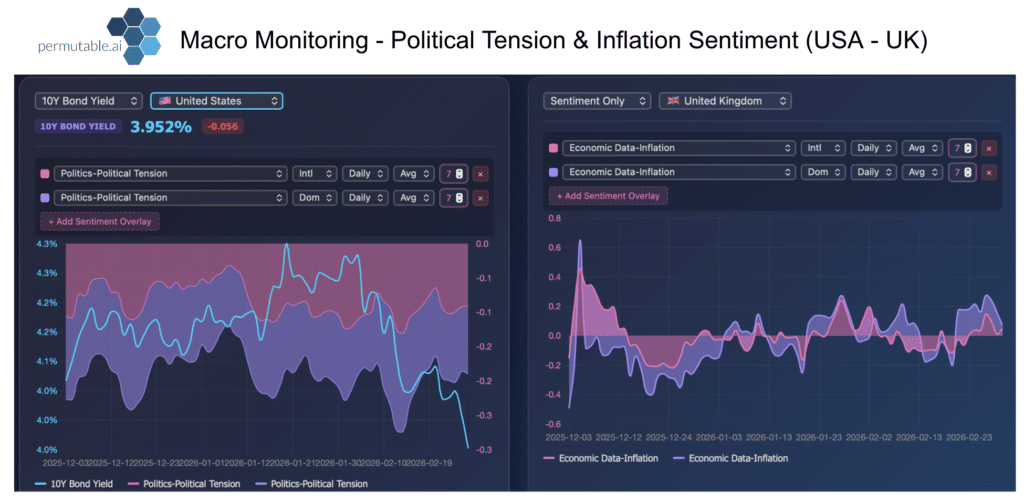

Above: Real-time macro sentiment reveals how political tension and inflation narratives evolve across regions, providing early insight into movements in bond yields and shifting policy expectations.

Most quantitative investment strategies still rely on a familiar set of inputs rooted in structured data. These include scheduled macroeconomic releases, price-based indicators, factor models, and historical correlations that have long formed the foundation of systematic investing.

While these inputs remain valuable, they share a fundamental limitation – they are inherently backward-looking. Macroeconomic data is released on fixed schedules, often reflecting conditions that have already evolved. Consensus expectations tend to be priced in ahead of publication, reducing their predictive power. Even high-frequency datasets, while faster, struggle to capture the broader context behind market moves.

At the same time, the volume of unstructured information has expanded dramatically. Markets now respond in real time to central bank communication, geopolitical developments, supply chain disruptions, and shifts in narrative momentum. Yet most quantitative systematic strategies are not designed to process this type of information at scale. As a result, a significant portion of market-relevant signal remains untapped.

Modern markets are increasingly driven by narrative formation rather than isolated data points. It is no longer sufficient to know what has happened. Investors need to understand what is being said, how sentiment is evolving, where expectations are shifting, and which narratives are gaining persistence.

This is where real-time macro intelligence shows its true value. Instead of waiting for structured confirmation, it focuses on tracking how information is interpreted as it emerges. It captures the transition from raw information to market-moving narrative, and ultimately to price.

Building real-time intelligence for quantitative investment strategies

Permutable was built specifically to address this shift. Founded by a former quant trader, our platform has been designed around a simple but powerful insight. Traditional data shows what has happened, but the real edge lies in understanding what is happening now.

By applying institutional-grade AI and natural language processing to global information flows, we convert unstructured data into structured, decision-ready intelligence. This allows quantitative investors to access signals that were previously inaccessible to systematic models.

At its core, the our intelligence engine continuously processes vast volumes of global inputs in real time. These inputs span financial news, policy communication, geopolitical developments, and sector-specific signals that influence markets across asset classes.

Rather than presenting this information as raw data, our system transforms it into machine-readable outputs designed for direct integration into quantitative investment strategies. Headlines are structured, enriched with sentiment and thematic context, and translated into signals that can inform positioning.

This creates a seamless pipeline from information to action. What begins as fragmented narrative becomes structured data, which is then converted into signals that can be deployed within models.

A central component of Permutable’s offering is our real-time macro intelligence framework. Our system tracks over fifty global economies and monitors twenty-six macroeconomic themes, including inflation, growth, labour dynamics, and policy developments.

Unlike traditional macro datasets, which are tied to scheduled releases, our macro indices update intraday as information flows. This enables investors to capture expectation shifts as they form, rather than after they are confirmed.

For quantitative investment strategies, this creates a meaningful advantage. It allows for earlier identification of changes in policy expectations, provides visibility into divergence between domestic and global narratives, and enables cross-asset analysis across FX, rates, and commodities.

The result is a forward-looking view of macro conditions that traditional models struggle to replicate.

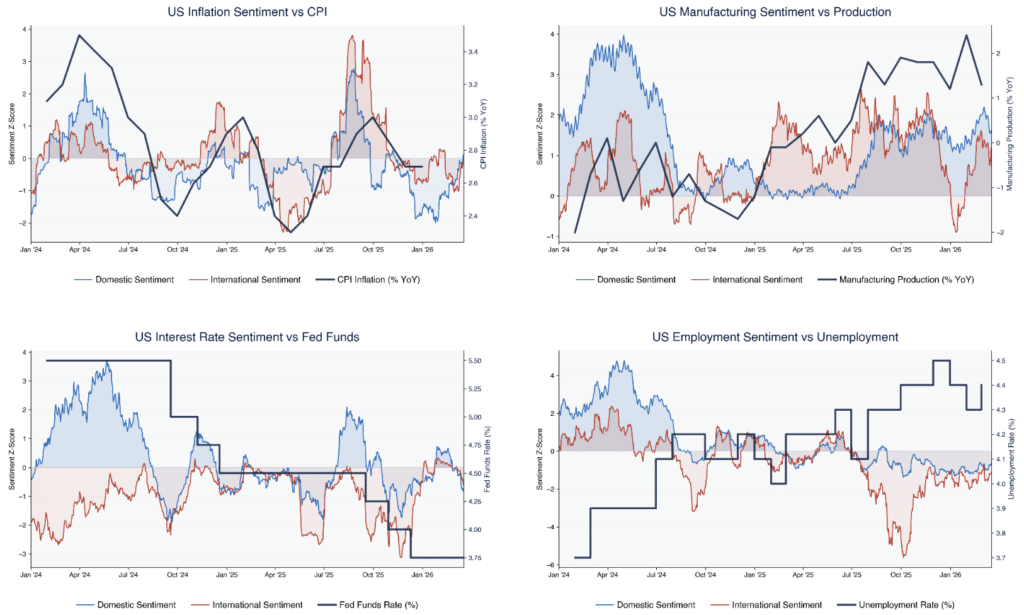

Above: Charts comparing US macro sentiment scores with CPI inflation, manufacturing production, interest rates, and unemployment, showing sentiment trends versus official economic data.

Beyond macro intelligence, we also deliver asset-specific data intelligence across commodities, currencies, and other key markets. Each asset is modelled individually, ensuring that signals reflect how that market responds to information in practice.

This includes directional sentiment indicators, topic-level drivers such as supply and demand or geopolitical risk, and multi-layer sentiment that combines macro and asset-specific inputs. By structuring signals in this way, the platform ensures that outputs are not only data-driven but also context-aware.

This distinction is perhaps one of the most important. In fact, not all sentiment is market sentiment. However, by filtering and weighting information through asset-specific logic we ensure that signals align with actual price behaviour, making them far more actionable for quant strategies.

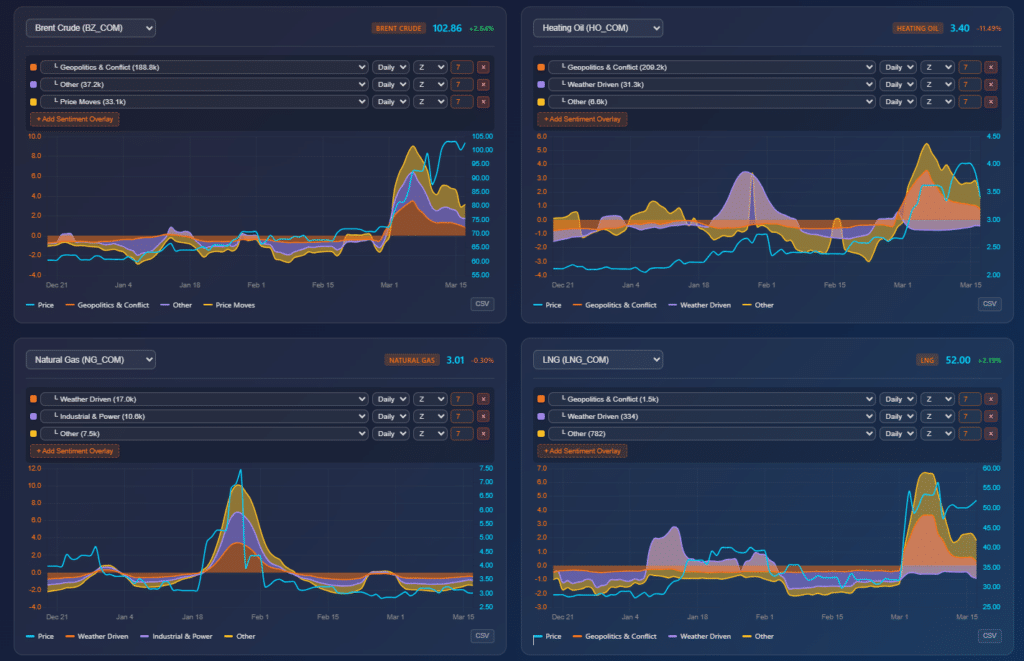

Above: Each asset responds to a distinct mix of narrative drivers, with real-time sentiment decomposition revealing how geopolitics, weather, and market structure shape price behaviour.

A defining strength of our real-time macro intelligence is the ability to integrate it directly into quantitative workflows. The platform delivers machine-readable signals in consistent formats, ensuring compatibility with existing models and systems.

It also provides both real-time and historical datasets, including point-in-time data that supports rigorous backtesting and validation. This ensures that signals can be tested, refined, and deployed with confidence.

For quantitative systematic strategies, this removes a key barrier. The transition from insight to implementation becomes seamless, enabling faster deployment of new signals into live trading environments.

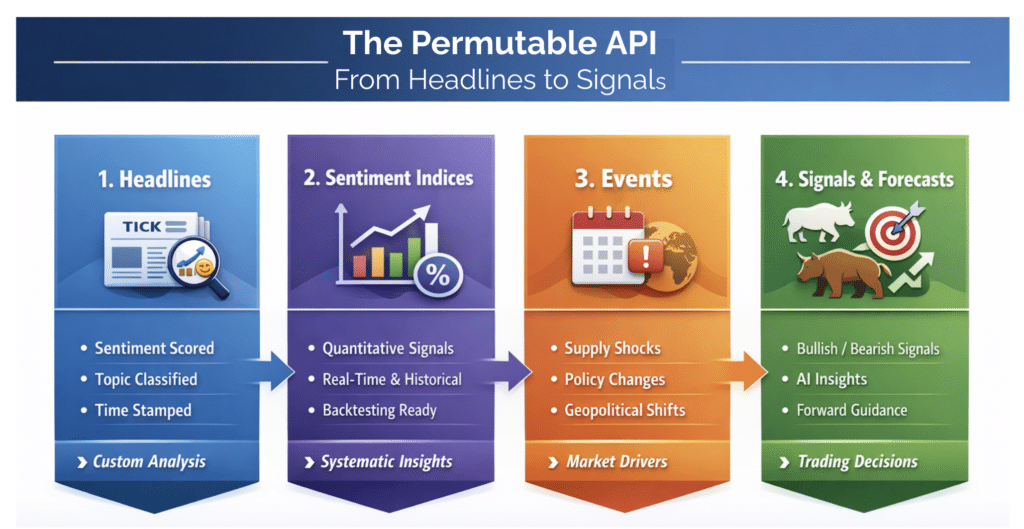

Above: Permutable’s pipeline transforms unstructured global information into structured, model-ready signals, enabling seamless integration into quantitative trading strategies.

Markets generate a constant stream of information, but not all of it is meaningful. One of the most valuable aspects of our real-time intelligence is its ability to distinguish between short-term noise and structural change.

We achieve this by continuously monitoring thousands of sources, analysing multiple themes simultaneously, and tracking how signals evolve over time, identifying when sentiment is persistent and when it is merely reactive.

The ability to separate noise from genuine regime shifts is crucial for investors, enabling more confident decision-making and reducing the risk of reacting to false signals.

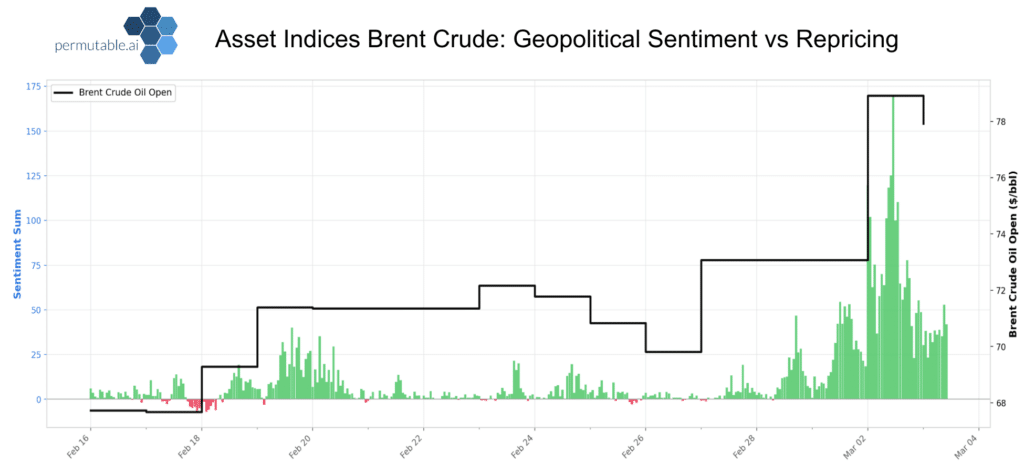

Above: Sharp increases in geopolitical sentiment coincide with step-changes in oil prices, demonstrating how persistent narrative shifts drive structural market repricing rather than short-term noise.

For hedge funds, incorporating our real-time macro intelligence provides a significant advantage. It enhances quantitative hedge fund strategies by introducing forward-looking signals that improve timing, positioning, and risk management.

By capturing shifts in narrative and sentiment before they are fully reflected in price, these signals allow funds to act earlier and with greater conviction. They also provide additional context for traditional models, improving their ability to adapt to changing market conditions.

This is particularly valuable in markets where macro and geopolitical factors play a dominant role, such as commodities and foreign exchange. See our live performance track here.

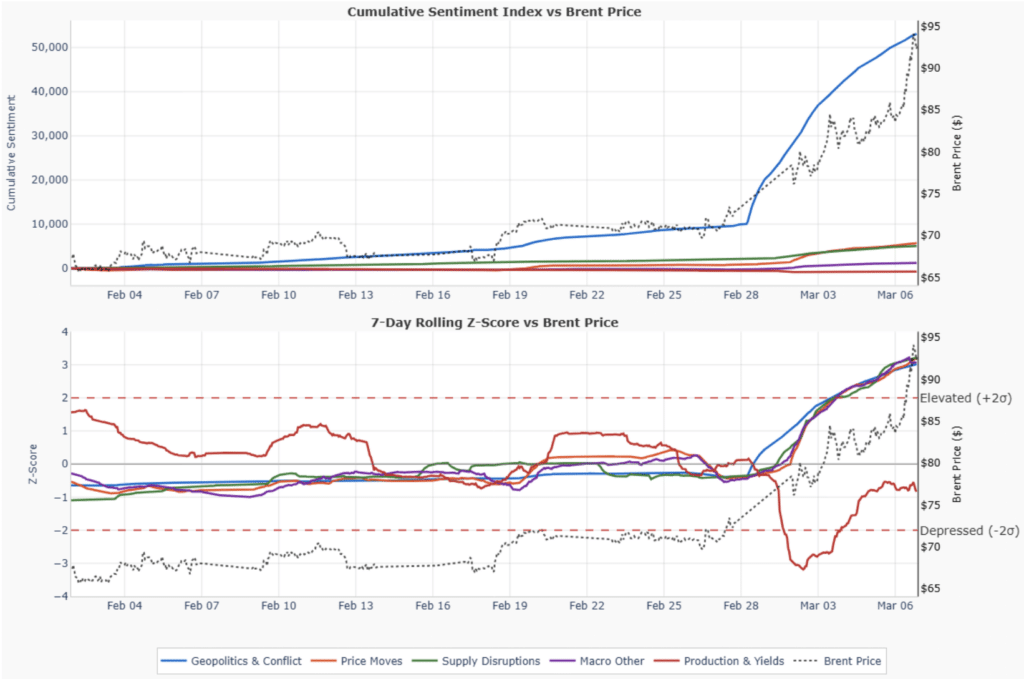

Chart above: Real-time sentiment signals begin to shift before Brent price reacts, with Z-score extremes highlighting inflection points where narrative transitions into market repricing.

Quantitative investing is undergoing a structural transformation. The industry is moving away from reliance on purely structured data and towards models that incorporate real-time, unstructured information.

This shift reflects a broader change in how markets operate. Information flows are faster, narratives evolve more quickly, and decision cycles are shorter.

At Permutable, our real-time macro intelligence is not a replacement for traditional data. It is a complementary layer that adds context, timing, and forward-looking insight. For modern quantitative investment strategies, it is becoming an essential component.

The edge in quantitative investing is no longer defined by access to more data. It is defined by the ability to understand markets as they move.

At Permutable, we deliver this capability by transforming global information flows into structured, actionable intelligence, enabling investors to identify shifts earlier, act with greater confidence, and stay ahead of the market.

In an environment where timing is everything, the ability to move from narrative to signal is no longer optional. It is the edge.

For a deeper look at how these signals behave across markets, explore our latest editions of Permutable Perspective. Each issue breaks down real-time macro intelligence, asset-level insights and live market dynamics, showing how narrative translates into signal and signal into positioning.

Discover more at Permutable Perspective and see how our intelligence performs in practice.

Analysis

08 Jul 2026

US inflation sentiment signal shows shift from energy shock to sticky services risk

Read more >

Analysis

07 Jul 2026

Testing GMSI US monetary policy sentiment as a short-end rates signal

Read more >

Analysis

01 Jul 2026

Global Macro Sentiment Indices: Turning point-in-time macro sentiment data into live systematic workflows

Read more >