The Price of Passage: How Geopolitical Sentiment Led the Repricing of Gulf Crude-Flow Risk

15 Jul 2026

15 Jul 2026

In this article, we examine how Brent’s risk premium evolved between June and July 2026. Permutable’s Brent crude sentiment indices show that the market’s pricing of conflict shifted from the probability of escalation to the viability of the routes carrying Gulf crude. The signal turned bullish before Brent repriced, while the mid-July attacks on the corridor used to bypass Iran’s restrictions help explain why the premium may prove slower to unwind.

Brent broke past the $86 mark on 14 July, the prompt market catching up with a divergence that had already been confirmed in the sentiment data. The overnight strikes on ADNOC’s Al Bahyah and Mombasa B inside Omani territorial waters did more than add a fresh war-risk premium. They ended the market’s complacent relief trade by demonstrating what it had been resting on. For the best part of June, traders had treated the Gulf’s deteriorating security as a passing headache; that view has now capitulated.

Our energy market sentiment indices told the true story in real time. Geopolitics & Conflict turned bullish, followed closely by Policy & Regulation, and the two climbed in tandem as blockades, transit levies and state-guided escorts pressed on the same shipping corridor from opposite directions. The price of passage no longer rests on whether the oil exists, but on whether it can move on terms that underwriters, charterers and shipowners will accept.

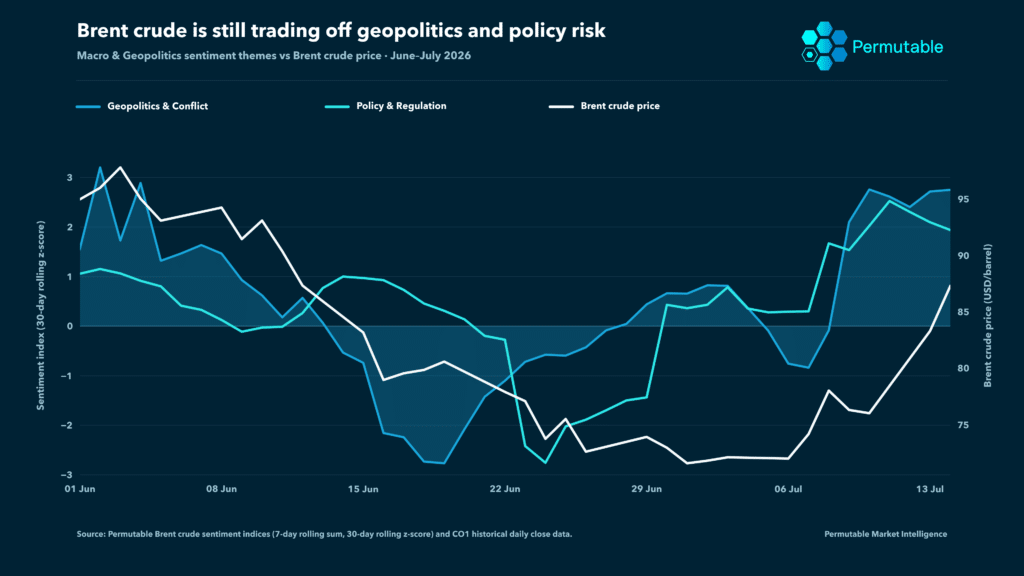

Caption: Brent sentiment began turning bullish in late June while the crude price remained close to its lows. Geopolitics & Conflict recovered first, followed by Policy & Regulation as blockades, tighter transit conditions and attacks on shipping converged on the same export corridor. Brent repriced only after both themes had moved above their recent baselines.

The chart sets two price-directional Brent sentiment themes against the CO1 daily close: Geopolitics & Conflict and Policy & Regulation. Positive readings are bullish for Brent; negative readings are bearish.

A tanker strike is operationally damaging. For Brent, it is bullish when it raises the probability that internationally traded crude will be delayed, rerouted or withheld from the market.

The spring premium was already leaking away like air from a valve by early June. Brent sat in the mid-$90s and Geopolitics & Conflict stood nearly three standard deviations above its trailing norm, but both drifted lower as cargoes kept moving and the disruption looked manageable. Policy & Regulation barely stirred, leaving the premium concentrated in the immediate risk of another strike rather than a lasting restriction on deliverability.

By late June, that relief trade had run its course. Both sentiment themes had fallen close to the bottom of their recent ranges and Brent had eased towards the mid-$70s.

The next turn appeared first in the information flow. Geopolitics & Conflict recovered, followed by a sharper rise in Policy & Regulation as missile strikes, blockade measures and tighter transit conditions accumulated. Brent remained close to its lows, with the market still treating diplomacy as sufficient to contain the disruption.

For several sessions, Brent sentiment became more bullish while the price remained anchored. The indices did not identify the exact day or size of the eventual move. They showed that the ground beneath a $75 Brent was beginning to give way.

The adjustment came in two jolts rather than a glide. Brent jumped 9.6% on 13 July after Washington announced a renewed blockade, then moved above $86 the following day as attacks on shipping and direct US-Iran escalation forced the market to reassess Gulf export capacity.

The more durable shift sat beneath the price. Geopolitics & Conflict pushed sharply above its baseline, capturing the immediate threat to shipping, while Policy & Regulation climbed with it as blockades, transit arrangements and state-guided passage became part of the same trade.

For the first time in the period, both themes were bullish and moving together.

June’s premium rested mainly on the probability of military escalation, a risk that diplomacy can remove quickly. By July, the premium also reflected the terms on which crude could still move: insurance cover, escorted passage, transit restrictions and the willingness of owners to commit vessels.

The price recorded the adjustment. The sentiment indices showed what it was made of.

The two crude carriers struck in the Strait of Hormuz were not trying to break Iran’s restrictions. They were using the route designed to work around them.

ADNOC’s Al Bahyah and Mombasa B were hit by Iranian cruise missiles in the southern lane inside Omani territorial waters. Both vessels caught fire before the blazes were brought under control.

The ships belonged to the ADNOC fleet used to shuttle Gulf crude for transhipment off the UAE and Oman. ADNOC has been among the most active participants in the US military-led effort to keep the southern corridor operating. CENTCOM said the wider operation had facilitated more than 800 vessel transits and over 400 million barrels of crude through the strait during the previous two months.

By striking there, Iran extended the disruption from the main passage through Hormuz to the system sustaining flows around its restrictions.

Traffic data show how narrow that system has become. Since the 12th July, roughly 14 ships of all types crossing Hormuz, as of the 13th this has fallen to 9 ships. When you compare with close to 130 passing the strait a day before the war, it shows the sheer magnitude of the disruption. Within that total, six visible oil and gas tanker transits were recorded, the lowest visible tanker count since late May.

AIS switch-offs mean the observed figures somewhat understates total traffic volumes, but the fall remains severe. More of the surviving flow now depends on escorted movements determined by Trumps levies policy, controlled routings and transfers outside the Gulf.

The southern lane may remain open in a legal or military sense, but commercial access is decided elsewhere. Owners must be willing to nominate vessels, charterers must absorb the extra cost and underwriters must continue providing cover on workable terms.

A lane can remain open on the map while quietly closing on the chartering desks.

An escalation premium can fade in a handful of sessions on a ceasefire, renewed talks or a pause in attacks. Route risk unwinds through evidence: repeated safe transits, falling war-risk premiums, normal fixture activity and clearer rules around the blockade, Iranian transit demands and US-guided passage.

Keeping the two indices separate becomes useful during that unwind. Geopolitics & Conflict captures the immediate probability of attack. Policy & Regulation tracks the framework governing whether crude can continue moving once the immediate threat recedes.

If the conflict signal turns bearish while policy sentiment remains bullish, the premium has not left the market. It has moved into restrictions on deliverability.

Saudi Arabia’s East-West pipeline to Yanbu and the UAE’s link to Fujairah remain the main operational alternatives to Hormuz, but neither can replace the volume that moved through the strait before the crisis.

They shift regional exposure rather than remove it. Yanbu moves crude towards the Red Sea, where renewed Houthi activity has raised the risk around shipping and infrastructure, while Fujairah remains close to the wider conflict zone.

The Cape of Good Hope answers a different problem. It allows vessels to avoid the Red Sea and Suez Canal, but tankers loading inside the Gulf must still pass through Hormuz before beginning the longer journey south.

Flows can be rerouted. The geography they cross cannot.

The downstream system had little slack before the latest attacks. European diesel margins and US refining cracks were at record levels, while Asian diesel, jet-fuel and fuel-oil margins continued to strengthen.

Hormuz is adding pressure to an existing constraint. Russian export restrictions, limited refinery capacity and depleted product inventories had already reduced the market’s ability to absorb another disruption.

The inventory cushion has thinned as well. Global stocks fell sharply between March and June, while combined US crude and product inventories are at their lowest since 2003. The spring shock was cushioned partly through stock draws. That option remains available, but from a weaker starting point.

Who is sailing will matter as much as how many are moving through. A corridor sustained mainly by escorted or state-supported movements would offer weaker evidence of normalisation than the broad return of commercial tankers and LNG carriers.

Brent sentiment can mark the stages of that unwind. Geopolitics & Conflict turning bearish while Policy & Regulation remains bullish would show the immediate threat receding while restrictions on deliverability lingering. Both indices rolling over together would point to broader normalisation.

Until traffic rebuilds, insurance terms soften and the ordinary business of chartering resumes, route risk will remain in the Brent premium.

A Brent move driven by military escalation does not persist in the same way as one reinforced by blockades, transit restrictions and impaired shipping routes.

Permutable’s Energy Indices separate those drivers within the Brent information flow, helping trading, research and risk teams see what is moving the price, how the signal is changing and what would begin to reverse it.

Analysis

22 May 2026

Brent volatility: Tracking Brent’s three-month sentiment shift

Read more >

06 May 2026

How our real-time Brent crude intelligence signalled a shift in ceasefire sentiment before the oil selloff

Read more >

27 Apr 2026

Philippines: Energy Inflation Risk and the Monetary Policy Trilemma

Read more >