Philippines: Energy Inflation Risk and the Monetary Policy Trilemma

27 Apr 2026

27 Apr 2026

This article examines how Permutable’s Regional Macro Indices captured the return of energy inflation risk in the Philippines, and how that shift is now reshaping the country’s macro outlook. The central argument is straightforward: the Bangko Sentral ng Pilipinas is being forced into a narrower and less forgiving policy choice between inflation control, currency stability and growth support. For investors and policymakers alike, the wider significance is that narrative data can often detect regime change before it appears in the official numbers.

The BSP has returned to tightening, raising its target reverse repurchase rate by 25 basis points to 4.50%, while lifting the overnight deposit and lending facility rates to 4.00% and 5.00% respectively. The move marks a decisive break from the easing bias that still framed policy earlier this year, and is a reminder of how quickly conditions can revert when an external energy inflation shock meets currency pressure and limited room for manoeuvre.

The bank’s message was plain. The inflation outlook has worsened, underlying pressures are broadening, and early action is required to preserve price stability. This is no longer fine calibration at the margins. It is defensive policymaking in a harsher environment, where imported inflation is rising, the peso remains exposed, and growth momentum is fading.

This is the trilemma now confronting the BSP: contain inflation, support the currency, and avoid tightening into weaker growth. The latest move should be read not as routine adjustment, but as recognition that policy space has narrowed sharply.

The BSP may yet prove less an outlier than an early warning. The immediate lesson is domestic: imported energy pressure, currency fragility and softer demand have already pushed policy from easing bias towards defensive tightening. The broader risk, however, lies in persistence. A short disruption may add only modestly to headline and core inflation. A longer shock could keep energy prices elevated, push headline inflation nearer a percentage point higher, and begin to seep into core prices.

In that setting, central banks that only recently moved from easing to pause may find themselves weighing rate rises into weakening activity. What looks today like a policy trilemma in Manila could, if the shock endures, become a policy trap for larger economies as well.

Permutable’s Regional Macro Indices track the tone and intensity of macro-relevant coverage across economies and themes. They are not designed to mirror official releases in real time. Their value lies in identifying when the narrative backdrop is shifting before that turn is visible in conventional data.

That matters in the Philippines, where the macro story is no longer moving through a single channel. Inflation pressure has re-emerged, the external conflict shock is feeding domestic costs, the peso remains vulnerable, rates have repriced higher, and the growth narrative has softened. Across the chart pack, those pressures appear in the narrative first and in the hard data later.

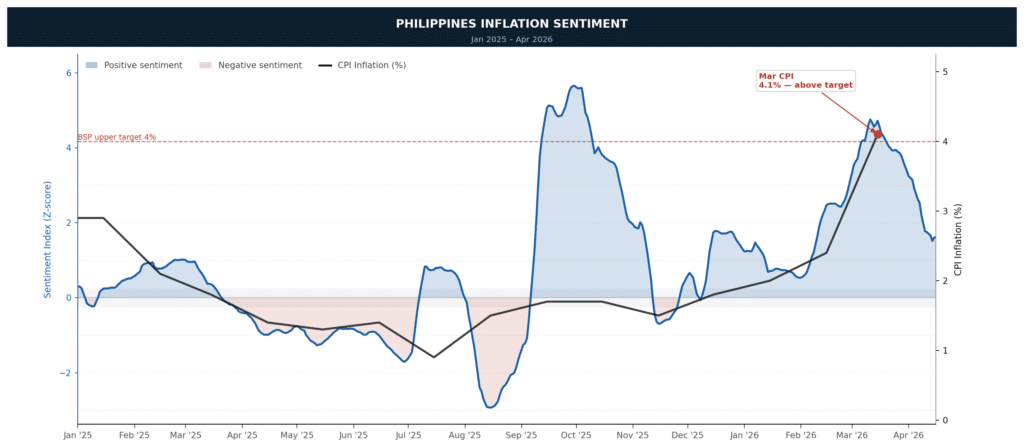

The inflation data gave the BSP a strong basis for acting. Headline inflation rose to 4.1% in March from 2.4% in February, moving above both the BSP’s 2% to 4% target band and its own March forecast range. Average inflation for the first quarter still came in at 2.8%, but the monthly acceleration was sharp enough to alter the policy tone. Core inflation also rose, to 3.2% from 2.9%, suggesting that the pressure is no longer confined to the initial fuel shock. The burden is also becoming more visible at the household level, with inflation for the bottom 30% of households accelerating to 4.2% in March.

Permutable’s inflation sentiment index captures this shift in narrative. It moved out of the deeply negative territory seen in mid-2025 and into clearly positive ground by the first quarter of 2026. In that sense, the narrative around price stability had already deteriorated before the March CPI print broke above target. The official data did not initiate the story. It confirmed a change that was already visible in the discourse. When inflation coverage becomes consistently more alarmed, it may point to a broader change in regime rather than a one-off disturbance.

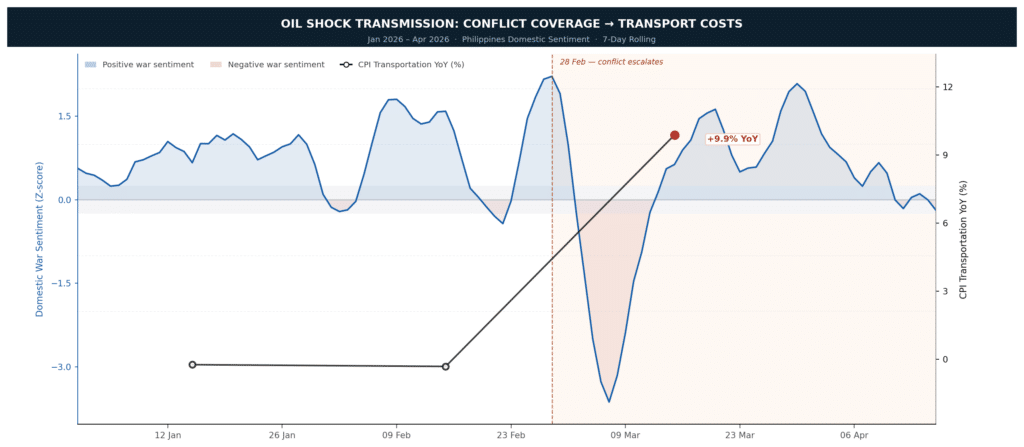

The March inflation breakdown helps explain why the pass-through matters. PSA data show that the acceleration was broad rather than isolated, with transport, housing and utilities, and food all contributing. Transport inflation rose 9.9% year on year. The housing, water, electricity, gas and other fuels category increased 4.5%. Food inflation also picked up as rice prices turned higher. Higher domestic petroleum prices have lifted transport and logistics costs, electricity charges have risen, and fuel costs are now feeding into the food chain through farmgate, post-harvest and distribution channels.

Domestic conflict coverage in the Philippines is therefore not simply a proxy for geopolitical anxiety abroad. It also reflects a domestic lens on energy exposure, shipping disruption, logistics strain and remittance corridor risk. That narrative intensified sharply through late February and into March. The transmission into hard data then followed quickly rather than gradually. Transport CPI, which had been quite through January and February, rose to 9.9% YoY in March. The sentiment signal did not provide a forecast of the precise number, but it did highlight the direction of risk and the likely transmission channel before the official release made the pass-through visible.

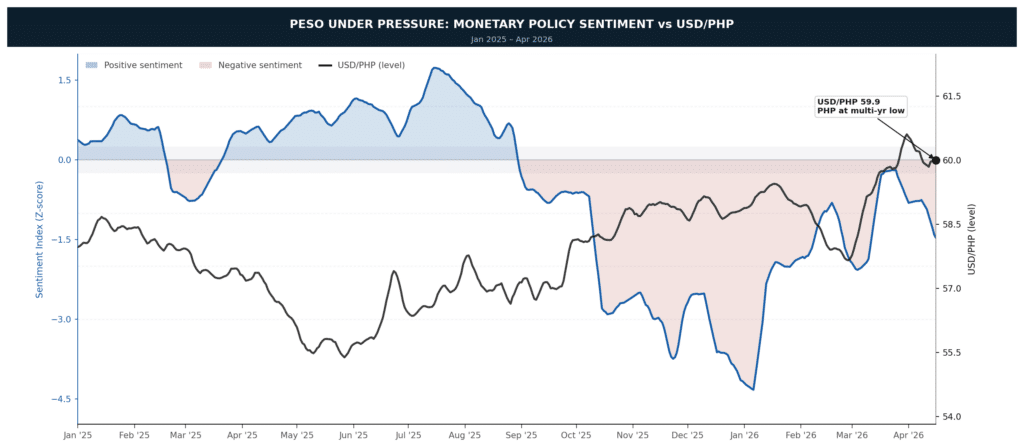

This is also an FX story. For the Philippines, tighter policy is not only about the inflation forecast. It is also about limiting the extent to which peso weakness adds to imported price pressures. March’s balance of payments deficit widened to US$2.6 billion, taking the cumulative first-quarter deficit to US$5.3 billion. Gross international reserves fell to US$106.6 billion at end-March. That still represents a meaningful external buffer, covering 7.0 months of imports and around 3.9 times short-term external debt on a residual maturity basis, but it still points to a somewhat softer external picture than the BSP would ideally face during an oil shock.

The peso remains an important part of that transmission chain. A rate increase may help limit near-term downside pressure, but it does not remove the underlying vulnerability of an economy heavily exposed to Middle Eastern oil and to external financing conditions. A negative monetary policy sentiment score should not be read simply as a signal of easier policy expectations.

In this context, it points more to a policy narrative marked by concern, constraint and limited room for manoeuvre. Negative sentiment here suggests constrained optionality rather than accommodation. Read that way, the chart alongside USD/PHP reflects the strain created by a more difficult policy mix in which the BSP is trying to contain inflation risks, defend credibility and lean against imported price pressure at the same time.

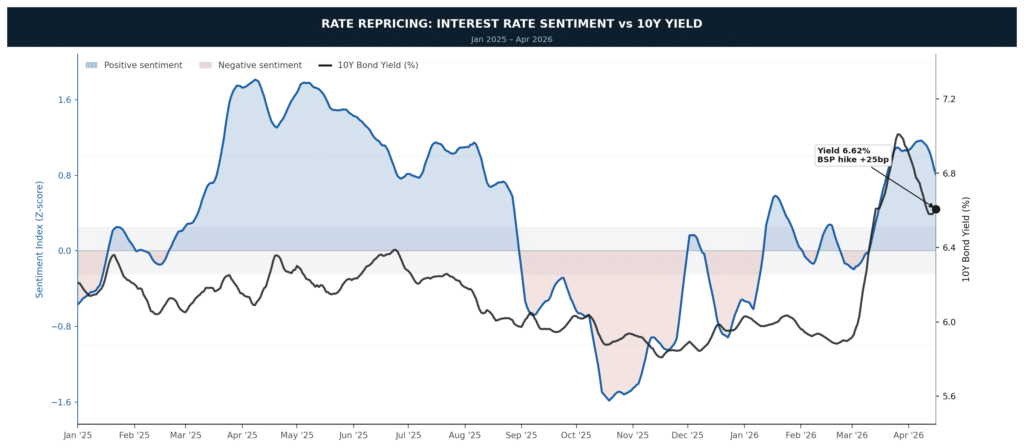

Permutable’s interest rate sentiment shows the relationship to the 10yr yield variable it is plotted against. When negative commentary around BSP policy becomes more sustained, the bond market has tended to reprice within days rather than weeks.

That is the pattern visible through the first quarter of 2026. By the time the BSP delivered its 25 basis point hike, the hawkish narrative was already established and the 10yr yield had already moved higher. A yield around 6.62% does not appear consistent with a market assuming that inflation pressures will fade quickly. Rather, it appears consistent with a market that sees the central bank as having to respond defensively to a backdrop it does not fully control.

The broader context complicates the policy calculus further. Fitch affirmed the Philippines’ BBB rating but revised the outlook to negative, reflecting the economy’s exposure to the global energy shock and the drag from scandals disrupted public investment. Growth is still expected to hold up better than in some peer economies, but the medium-term outlook is softer, with 2026 GDP growth seen below the government’s 5% to 6% target range. The BSP is therefore tightening into a weaker growth backdrop, not because it is seeking to suppress demand for its own sake, but because the risk of allowing an oil shock to feed through into core inflation, food prices and the exchange rate has increased.

That softer backdrop is also visible in the GDP sentiment chart. The index is not collapsing, but neither is it offering much reassurance. A reading close to neutral during a tightening phase is rarely an entirely benign signal. Neutral growth sentiment suggests that the market narrative has become less willing to reinforce the official growth story. It has not turned clearly pessimistic, but it has become less supportive. That distinction matters. The growth narrative has lost conviction, not collapsed. Even so, that alone is enough to make the policy mix more difficult if inflation and FX pressures continue to build.

A further complication is the broader dollar environment. Safe-haven demand has supported the dollar again as tensions around Iran and the Strait of Hormuz persist, while discussion around swap lines and dollar funding conditions has added another layer of pressure for oil-importing economies trying to stabilise their currencies. That does not alter the BSP’s domestic mandate, but it does make the external setting less forgiving and narrows the room between inflation management and growth support that the central bank would ideally want to preserve.

Taken together, this looks less like a routine 25 basis point hike and more like a defensive move aimed at limiting risks across several fronts at once: inflation expectations, peso stability and second-round effects. The BSP is no longer simply fine-tuning policy. It is responding to the risk that an external oil shock could become a broader domestic inflation and FX problem.

That is also the core message of the charts. These indices are not mechanical forecasting tools. They show when the narrative around a macro theme has shifted before the official data fully reflects it.

In the Philippines, the signals are starting to line up:

The official data is now moving in the same direction, but with months lag.

For investors and macro teams looking to track sentiment can give you an insight into evolving policy risk, inflation dynamics and cross-asset transmission in real time, Permutable’s macro sentiment offers a structured view of how narratives are shifting across markets. For access or further information, contact enquiries@permutable.ai

27 Jul 2026

The tide turns on Russia inflation outlook as drone strikes spread from refineries to warehouses

Read more >

Analysis

27 Jul 2026

Saudi supply risk and import costs drive energy inflation sentiment higher

Read more >

Analysis

22 Jul 2026

UK inflation fell to 2.6% after Permutable’s Global Macro Sentiment Indices saw it coming

Read more >