In this article, we analyse USD/JPY through the lens of domestic US and Japan rates sentiment, testing whether FX has kept pace with the compression in the 2-year spread. For discretionary macro and systematic desks, we combine bond market pricing with cross-sectional policy analysis to assess whether the next regime shift is already underway, or still playing catch up.

The Old Regime Ends a New One Begins

For a decade, USD/JPY was the clearest expression of monetary divergence and the carry trade. Japan in monetary anaesthesia. The US in perpetual motion. The carry machine hummed away, the yen absorbed the adjustment, and the spread did the explaining.

That regime has faded into a distant memory. The rate differential has compressed, yet FX has only partly followed. The question now is whether USD/JPY will finally move with the new spread reality, or continue to chart its own course.

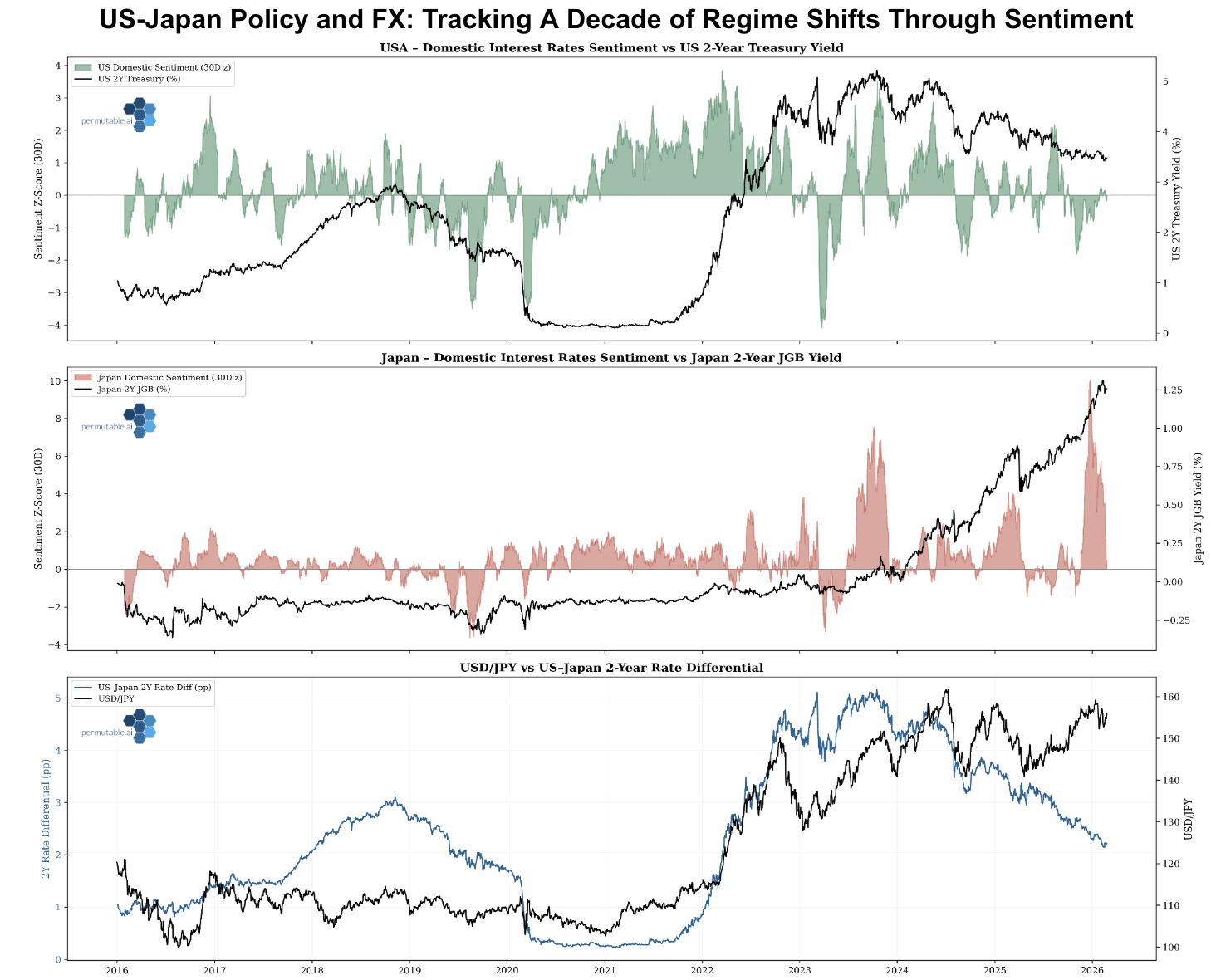

The 2-year US-Japan rate differential has compressed by nearly 300 basis points from its 2023 peak. Japanese domestic rate sentiment has reached levels unseen in the prior decade, a structural shift, not noise. Yet USD/JPY remains in the mid-150s, pricing a divergence regime the bond market has already left behind.

The framework here is cross-asset and cross-sectional. We focus on the 2-year point of the curve, where policy is transmitted most directly, and draw on domestic interest rate sentiment from Regional Macro Indices spanning more than a decade and 50+ countries. Hard data confirm what has already occurred. Sentiment identifies what is building.

From financial repression, through the divergence peak, to today’s early convergence, USD/JPY has moved through three clear regimes. What stands out now is the gap between what the front end is pricing and where FX is trading. It is not just a narrative mismatch, but a meaningful skew for the path ahead.

Chart 1 – Full Cycle View (2016-2026). US and Japan domestic rate sentiment (30D z-score), 2Y yields (%), USD/JPY spot, US-Japan 2Y rate differential

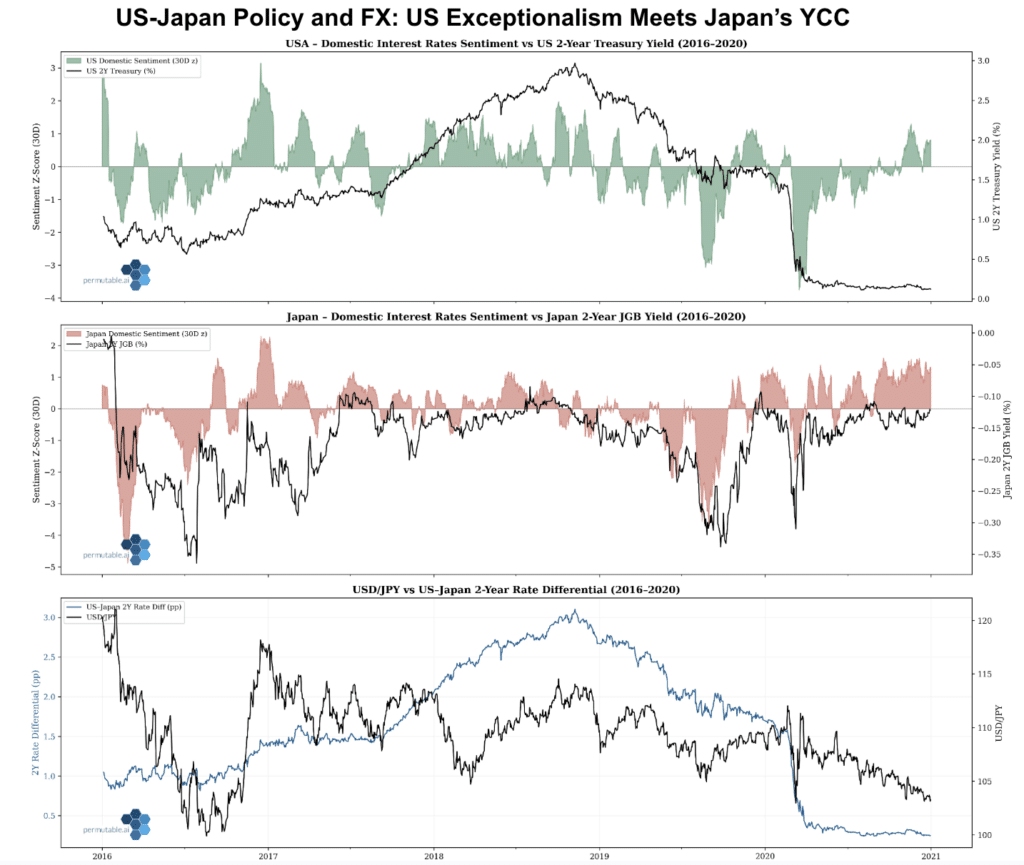

The Divergence Regime: 2016 – 2020

Between 2016 and 2020, asymmetry defined global macro. The Federal Reserve operated within a conventional tightening and easing cycle. The Bank of Japan remained committed to Yield Curve Control and negative rates. Japan functioned as the world’s monetary ballast, stable, suppressed, and predictable.

The 2-year JGB traded as though policy had been fixed in place. Yields hovered near or below zero. The 10-year was actively managed. Domestic rate sentiment in Japan was not merely subdued, it was dormant. For most of the period, readings clustered near zero with little sustained deviation. The market had stopped pricing the possibility of change.

The Fed, by contrast, tightened into 2018, pivoted in 2019, and maintained a structural yield premium over Japan even during easing phases. USD/JPY tracked the 2-year differential closely. The transmission was straightforward: wider spread, stronger dollar. Japan was the funding currency. The carry trade dominated positioning logic.

US rate narratives oscillated with growth and inflation cycles. Japanese narratives barely moved. That asymmetry underpinned a profitable yen-funded carry environment, and the sentiment data from this period show just how absolute Japan’s rate inertia was. The z-score of Japanese domestic rate sentiment barely surfaced above zero for the entire 2016-2020 window.

The Shock and Repricing: 2020 – 2023

The pandemic disrupted the regime. US yields collapsed in 2020, with the 2-year Treasury falling below 0.2%. Japan barely moved, policy was already fully compressed. There was nowhere lower to go.

The inflation shock of 2021-2022 reversed the dynamic with violent speed. US domestic rate sentiment did not just turn positive, it ignited. The hiking cycle arrived not as a gentle recalibration but as a four-alarm fire. The 2-year Treasury repriced by more than 400 basis points in under eighteen months. USD/JPY followed the spread like a compass finding north. The carry machine was running at full throttle with the handbrake off.

Japan kept the lights off. Yield Curve Control held. The yen became the world’s preferred funding currency, borrowed cheaply, sold freely, and recycled into everything with a yield attached. USD/JPY moved above 150 and approached 160. Divergence reached its most extreme expression.

Yet even at the divergence peak, the tone was beginning to shift. Japanese domestic rate sentiment started to rise in 2023 as inflation proved more persistent and policy debate intensified. The carry remained intact, but momentum was no longer one-directional. Sentiment registered the turn before spreads fully adjusted.

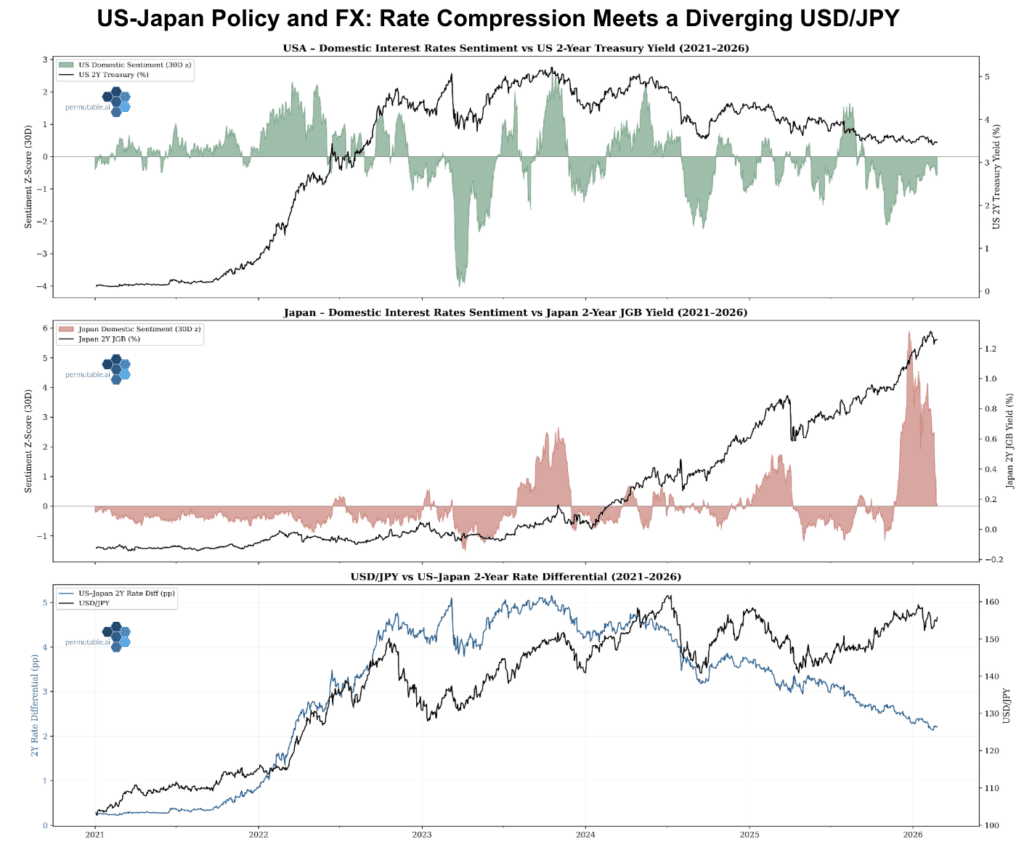

Chart 3 — The Repricing and Convergence (2021-2026). Japan rate sentiment z-score breaks above +5 in late 2025, a level with no precedent in the prior decade, as the US-Japan 2Y differential compresses from 5pp to just above 2pp.

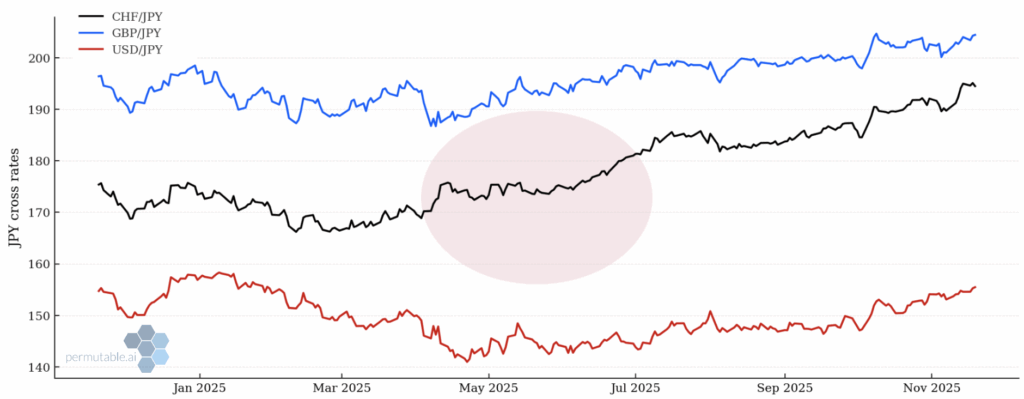

Exit from YCC and Compression of the Spread: 2023 – 2026

Yield Curve Control was first adjusted, then dismantled. The 2-year JGB, anchored below zero for years, moved above 1.2% by early 2026. In absolute terms that level remains modest. Relative to the prior decade, it represents a structural shift.

Japanese domestic rate sentiment reinforces this notion. By late 2025, the 30-day z-score exceeded +5, a reading without precedent in the prior cycle. This was not incremental adjustment. It marked the end of the ultra-loose policy era.

In the US, the hiking cycle ended and expectations shifted toward gradual easing. The 2-year Treasury rolled from its 2023 peak toward the mid-3% range. Rate sentiment cooled steadily from its extreme positive readings toward neutral.

After retreating from near 160 during the January 2026 intervention episode, USD/JPY stabilised in the mid-150s. FX remained elevated relative to the new spread regime. The adjustment process is incomplete.

February 2026: Policy Signalling vs Pricing

By late February 2026, the US-Japan complex reflects various overlapping dynamics. Their interaction defines the near-term range and the medium-term direction. What appears noisy at the surface is, underneath, a story of gradual convergence constrained by politics and policy tripwires.

1. The US Curve: Moderation Without Capitulation

The 2-year Treasury sits near 3.45%, consistent with modest easing expectations. The 10-year trades around 4.05%, the 30-year near 4.7%. The curve has steepened as the fiscal materialises. Cuts are being priced in, but not as aggressively as thought with the incoming appointment of Warsh being the next Fed chair .

US domestic rate sentiment reflects that shift. The tone of 2022-2023 has faded toward neutral. The US is no longer widening the differential. It is contributing to compression of the rate differential.

2. Japan: Normalisation with Political Spillover

The yen has softened on reports that Prime Minister Takaichi is uncomfortable with further rate rises, and on the nomination of incoming BoJ board members leaning more towards a dovish stance. Yet in reality the centre of gravity towards normalisation may not shift as far as the headlines imply.

Additionally, against Japan’s new fiscal backdrop, this adds a further dimension debate. The LDP’s commanding lower-house majority following the February 2026 snap election gives the government capacity to push fiscal support, household tax relief and defence spending. With public debt still swelling above 200% of GDP and debt-servicing costs rising as yields lift from their decade-long floor, markets are assessing whether fiscal activism and monetary normalisation can coexist in the same breathe. They potentially can, but not without periodic friction.

The base case in the market still points to a June hike taking the policy rate to 1.0%. The structural trajectory has not shifted on the policy side. Inflation remains elevated beyond historic norms. Wage growth is accelerating. The debate now sits around the pace pace, not reversal.

3. FX Intervention ?

USD/JPY has consolidated since January’s rate-check episode. The 157 high from early February is within reach again. A clean break higher returns intervention risk to the foreground. The 155-160 range now functions as a political hurdle.

The asymmetry is structural: upside faces a political ceiling from the optics of currency weakness and rising import costs.

Three forces lead to the FX misalignment. The US is cooling. Japan is normalising. The question is not whether convergence continues, it is how much longer FX diverge from the the front end.

What the Sentiment Data Reveals

Traditional macro data confirm developments with delay. CPI validates disinflation after it occurs. GDP confirms output trends a quarter late. Sentiment captured in real time across 50+ economies reflects the early change in tide, the signal that the market is forming before it appears in price.

Three points stand out from the Regional Macro Indices for the current setup. First, US domestic rate narratives have cooled steadily since mid-2025, a directional fade from extreme positivity, not a collapse. Second, Japanese rate narratives have strengthened materially since 2023, reaching z-scores with no precedent in the prior decade. Third, and most important: the sentiment gap has moved in Japan’s favour even as USD/JPY remains near 155. Narrative momentum is fading in the US and building in Japan.

Cross-sectionally, Japan’s shift stands out across G10. While the Fed debates cuts and the ECB edges toward neutral, Japan alone is transitioning from ultra loose to policy normalisation. That cross-sectional divergence in sentiment strengthens the convergence thesis in rates. Rates, historically, pull FX. Yet the FX has broken away.

Discretionary and Systematic Use Cases

For macro desks, domestic rate sentiment provides a live read on policy direction before it is fully embedded in front-end pricing. It clarifies whether moves reflect cyclical noise or structural transition, between heat without light and a genuine directional shift.

In the current environment: if US tone continues to soften while Japan’s remains elevated, further compression is the base case. A re-acceleration in US inflation could temporarily re-widen the spread, a reflex rally in rate expectations, not a structural reversal. The carry machine does not announce when it is losing torque. Sentiment does.

For systematic investors, sentiment functions as a regime filter alongside yield differentials and volatility, identifying when the spread-FX relationship is stable versus when it is fraying under structural rotation. As a cross-sectional factor, it locates where policy narratives are turning first and fastest, before the price signal is clean.

The current read: Japan’s normalisation narrative is cross-sectionally dominant across G10. US sentiment has faded to near-neutral. The spread-FX gap is wide. The inflection is audible. Pricing is behind the story.

The Old Anchor Has Lifted

From financial repression to divergence peak to convergence phase, the US-Japan complex has transitioned across three distinct regimes. Bond markets moved first. Policy language confirmed the shift. FX is recalibrating from a position of meaningful overvaluation relative to the spread that has historically explained it.

The convergence story is asymmetric. Political sensitivity constrains upside in USD/JPY. Downside, if spread compression continues, faces fewer structural limits. The next phase is defined by conditional convergence, not sustained divergence. Hard data will confirm it later. Sentiment is already pricing it now.

The JGB has surfaced from a decade below zero. US rate narratives are cooling. The 2-year spread has compressed by nearly 300 basis points. The rubber band has been stretching for eighteen months. The carry machine is running on borrowed time.

USD/JPY is the last instrument in the complex to not have got the memo. And when it does, the move will not feel gradual to those who waited for the data to confirm it.

Monitor the Regime in Real Time

The Regional Macro Indices track domestic policy narratives across more than 50 economies, capturing shifts in rate expectations before they are fully reflected in front-end pricing. For further information on integrating the indices into discretionary frameworks or systematic models, get in touch at enquires@permutable.ai

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.