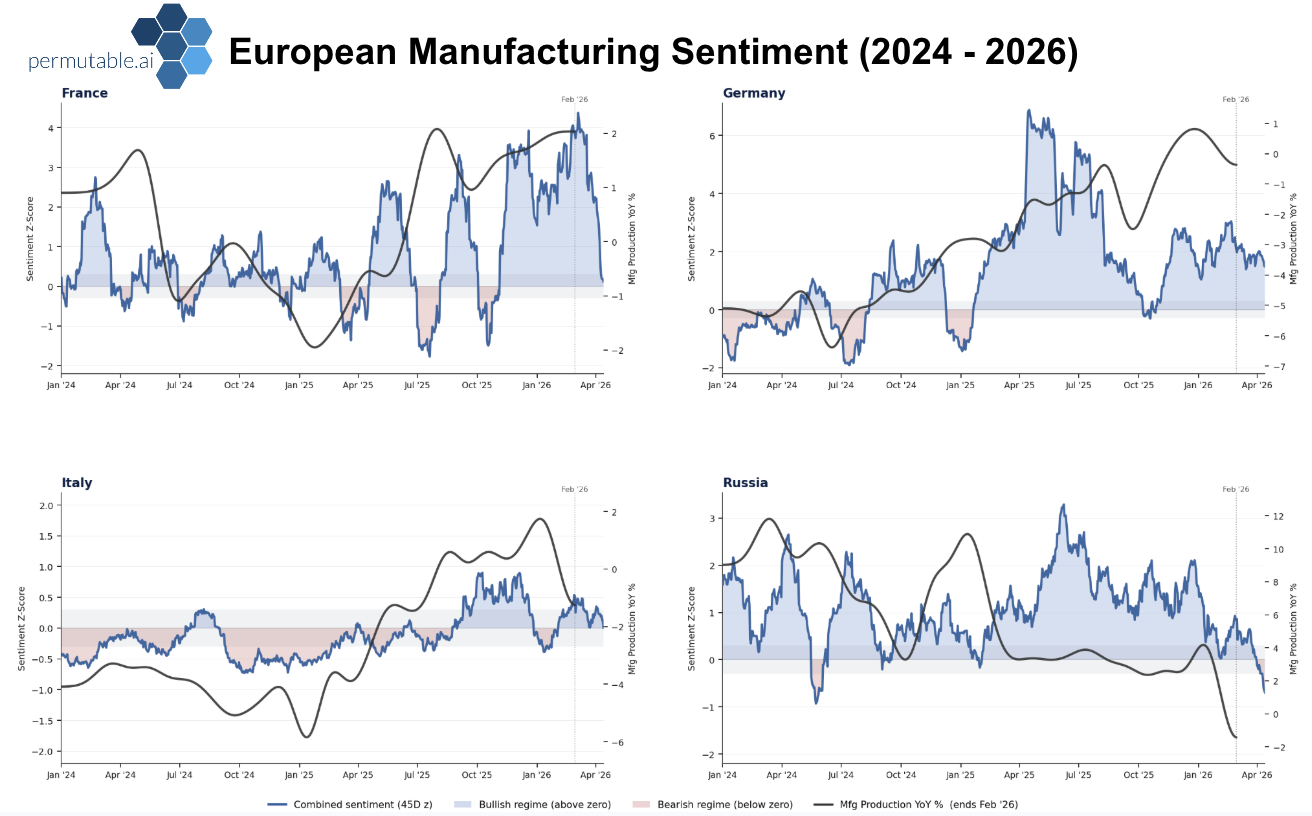

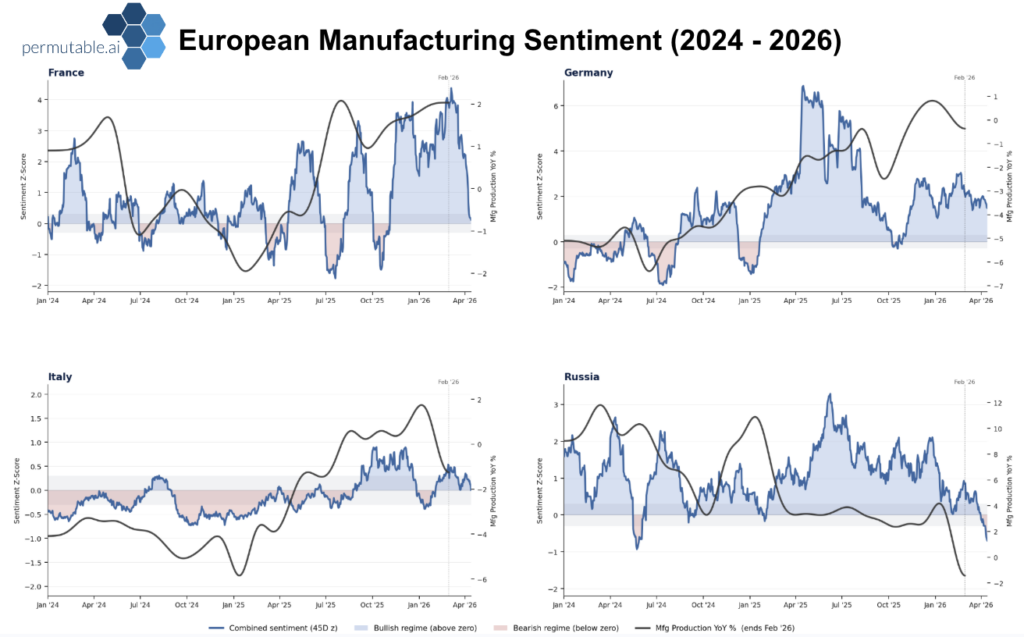

This article explores whether improving European manufacturing sentiment marks the start of a durable industrial recovery, or merely a welcome pause after a long period of stagnation. European manufacturing sentiment in April 2026 shows the sector has moved beyond its downturn, led by Germany and supported by Italy, but the recovery remains uneven and not yet broad-based across the region.

Germany has led the turn. Italy has improved steadily. France remains hesitant. Russia has weakened again.

Taken together, the picture is clear enough: European manufacturing is no longer in retreat, but nor has it yet entered a broad-based upswing.

There is a stage in every cycle when the headlines improve faster than the foundations beneath them. Output begins to rise, surveys return to expansion, and markets start to anticipate better days ahead, even as firms remain cautious on hiring, investment and forward demand.

That is where European manufacturing stands in April 2026.

For much of the past two years, Europe’s factory sector was defined by shrinking orders, weak production, falling inventories and poor confidence. The question was not when growth would accelerate, but whether the industrial base could stabilise at all. That phase has now changed.

Production has improved. Export demand has steadied. Permutable data shows sentiment has turned higher across much of the region. Yet the charts also show that this is not one story, but several national cycles unfolding at different speeds. That distinction matters. Recoveries are judged less by whether they begin than by whether they broaden.

The most sensible reading of the current data is that the industrial trough has come to an end.

What looks less certain is the strength of what comes next.

Across Germany, France and Italy, European Permutable’s data showed manufacturing sentiment improved before hard output data fully responded. That is often how turning points look. Expectations stabilise first, firms become less defensive, then production follows. But several features of the current rebound still warrant caution.

Input costs have risen again. Energy remains an active macro risk. Financing conditions are tighter than in previous recoveries. Employment behaviour across industry is still subdued. These are not yet the hallmarks of a confident, self-sustaining expansion.

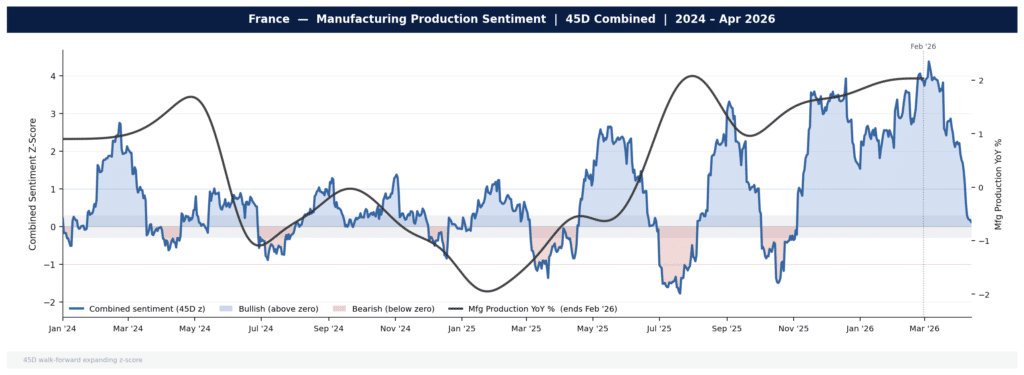

The charts reinforce the point. Germany remains positive, but below earlier peaks. Italy is improving, but moderately. France has recovered, though with unstable conviction.

Europe has moved off the floor. Whether it moves onto firmer footing remains to be consistently seen.

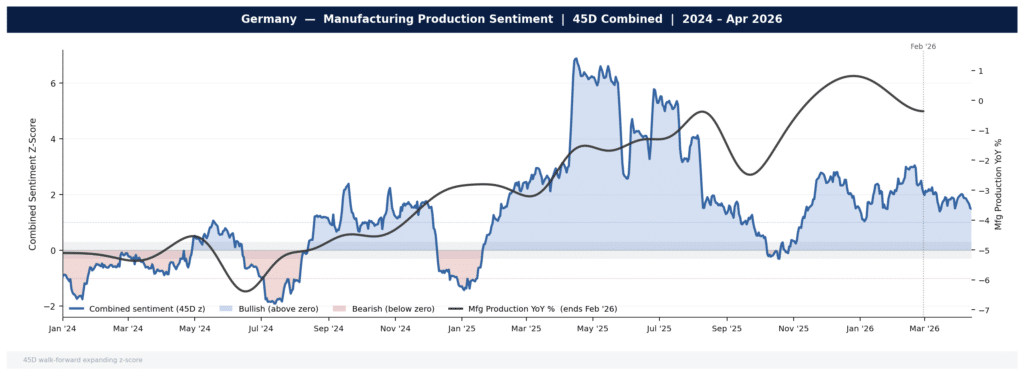

Germany remains the clearest cyclical leader in the region.

Its chart shows the strongest positive shift in manufacturing sentiment of the major economies, with momentum building through 2025 before cooling into 2026. Even after that moderation, conditions remain materially better than a year ago.

That pattern is familiar. Germany tends to respond early when global trade steadies, capital goods demand improves and external manufacturing conditions recover. But the latest phase also reveals the limitation of the rebound.

The first leg appears to have been driven largely by exports, inventory rebuilding and improving global conditions rather than a clear domestic acceleration. Consumption remains cautious. Corporate investment is selective. Energy-intensive sectors continue to operate under a structurally higher cost base than before 2022.

Germany has led the turn, but still on external terms. The next phase depends on whether domestic demand begins to participate.

What to watch: export orders, capex intentions, industrial hiring, China demand trends.

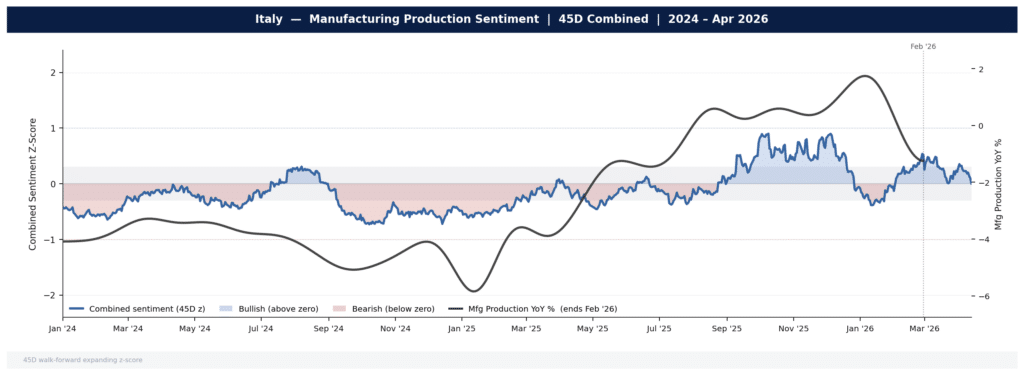

Italy offers one of the more constructive stories in Europe, though with less fanfare.

Manufacturing sentiment has improved in a steadier and more orderly fashion than in Germany. Rather than a sharp surge, the chart shows a gradual climb from depressed levels into modestly positive territory through late 2025 and early 2026.

That often signals a healthier repair process.

Industrial production has also improved, suggesting the turn is not merely rhetorical. Yet the recovery still appears lightly built. Fresh demand has lagged output in places, implying some firms are still working through backlogs or benefiting from regional spillovers rather than enjoying a powerful domestic upswing.

Italy is also more exposed to financing conditions and margin pressure among smaller firms, where higher borrowing costs and rising inputs are felt more quickly. Italy has repaired more cleanly than loudly. It is participating in the cycle, not yet defining it.

What to watch: new orders, SME credit conditions, input costs, spillover demand.

France remains the least convincing of the major Western European stories.

Manufacturing sentiment has improved sharply from the lows, and at times reached some of the strongest headline readings in the group. Yet the path has been more volatile, marked by repeated reversals rather than sustained momentum. That matters.

A volatile recovery often reflects episodic improvement rather than broadening strength. Output has stabilised, but forward demand still looks softer than in Germany, while the domestic economy has yet to generate a convincing industrial impulse.

France is also less exposed to the machinery and capital goods categories that benefit most from global restocking cycles. It therefore needs more help from domestic consumption and private confidence, both of which remain only partial supports. France has stopped falling. It has not yet started moving with conviction.

What to watch: household spending, business confidence, export demand, private investment.

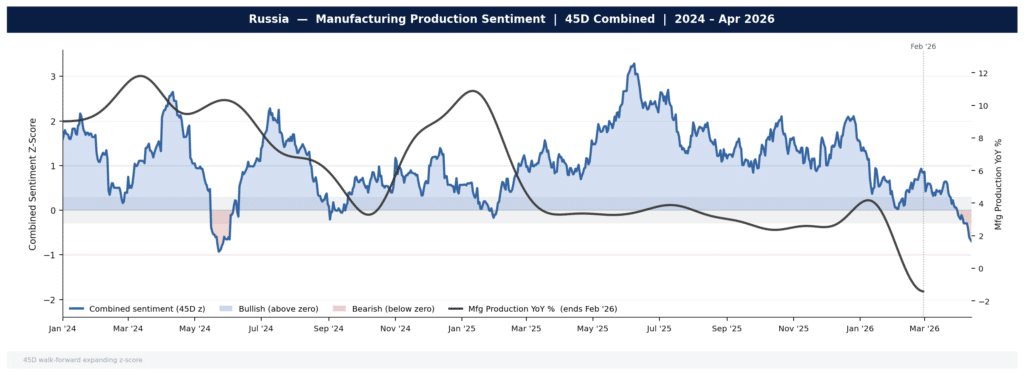

Russia should be viewed separately from the rest of the region, not merely because it has become detached in more ways than one, but because it is now operating within a materially different industrial cycle.

Its chart has deteriorated materially into 2026, with manufacturing sentiment turning lower again after a more resilient period through 2024 and 2025. That aligns with a weaker civilian industrial backdrop.

Russia is operating with a widening divide between state-directed production and the broader private economy. Public-sector industrial demand can support selected areas, even as ordinary manufacturers face high rates, softer purchasing power and impaired investment conditions.

Russia is not following the broader European manufacturing turn. It is operating within a structurally different and increasingly fragile cycle.

What to watch: inflation, credit conditions, state spending composition, private demand.

The key question is no longer whether European manufacturing has improved. It has. The more distinct question is whether that improvement is broadening, becoming self-sustaining, and spreading across countries in a robust way.

Official data will answer that eventually. Sentiment tends to get there first.

That is where Permutable’s sentiment data has value. It shows not only whether conditions are improving, but whether the move has breadth, persistence and conviction.

For discretionary desks: Permutable’s macro sentiment provides a timely and uncluttered read on whether Germany’s leadership is broadening across the region or remaining narrowly contained.

For systematic investors: As a model input, our sentiment data serves as an effective regime filter, helping distinguish between false dawns, periods of stabilisation, and genuine industrial recoveries.

Used properly, sentiment is not a substitute for hard data. It is an earlier signal of regime change, capturing shifts in the cycle before they are fully visible in the official numbers.

The current European manufacturing sentiment signal suggests the downturn has likely passed, but the recovery remains selective and vulnerable to cost pressure, weaker global demand and uneven domestic participation.

For markets, this implies:

A Germany-only rebound is a narrower market story. A broader turn across Germany, Italy and France would carry more force.

European manufacturing sentiment suggests the current turn is more than a temporary bounce, but not yet strong enough to be treated as a mature recovery. The next phase depends on whether improving sentiment translates into stronger orders, firmer hiring and more confident capital spending across the region.

That has direct implications for ECB expectations, equity leadership, FX positioning and cross-asset allocation.

Permutable’s Regional Macro Indices track domestic and international economic narratives across 50+ economies in real time, helping desks identify turning points before they are fully visible in traditional data.

For access or integration enquiries, contact us at enquiries@permutable.ai

European manufacturing sentiment measures how positive or negative economic narratives are around industrial activity across countries such as Germany, France and Italy.

Sentiment data suggests the downturn has passed, but the recovery remains uneven and not yet fully established.

Germany benefits from global trade exposure and capital goods demand, which tend to recover earlier in industrial cycles.

Analysis

29 Jul 2026

South Korea economy: the chip windfall is outrunning domestic growth

Read more >

27 Jul 2026

The tide turns on Russia inflation outlook as drone strikes spread from refineries to warehouses

Read more >

Analysis

27 Jul 2026

Saudi supply risk and import costs drive energy inflation sentiment higher

Read more >