Point-in-time datasets for macro backtesting: Reducing look-ahead bias in systematic strategies

14 May 2026

14 May 2026

This guide explains how point-in-time datasets improve macro backtests by reducing look-ahead bias, preserving historical data availability and supporting more realistic systematic strategy validation. It is aimed at quantitative researchers, macro hedge funds, systematic trading teams and institutional investors using macro, sentiment or alternative data signals in backtesting, model development and regime analysis.

Testing a macro trading strategy against historical data sounds straightforward until the data contains information that was not available at the time. This problem, known as look-ahead bias, can inflate backtest results and lead to disappointing live performance.

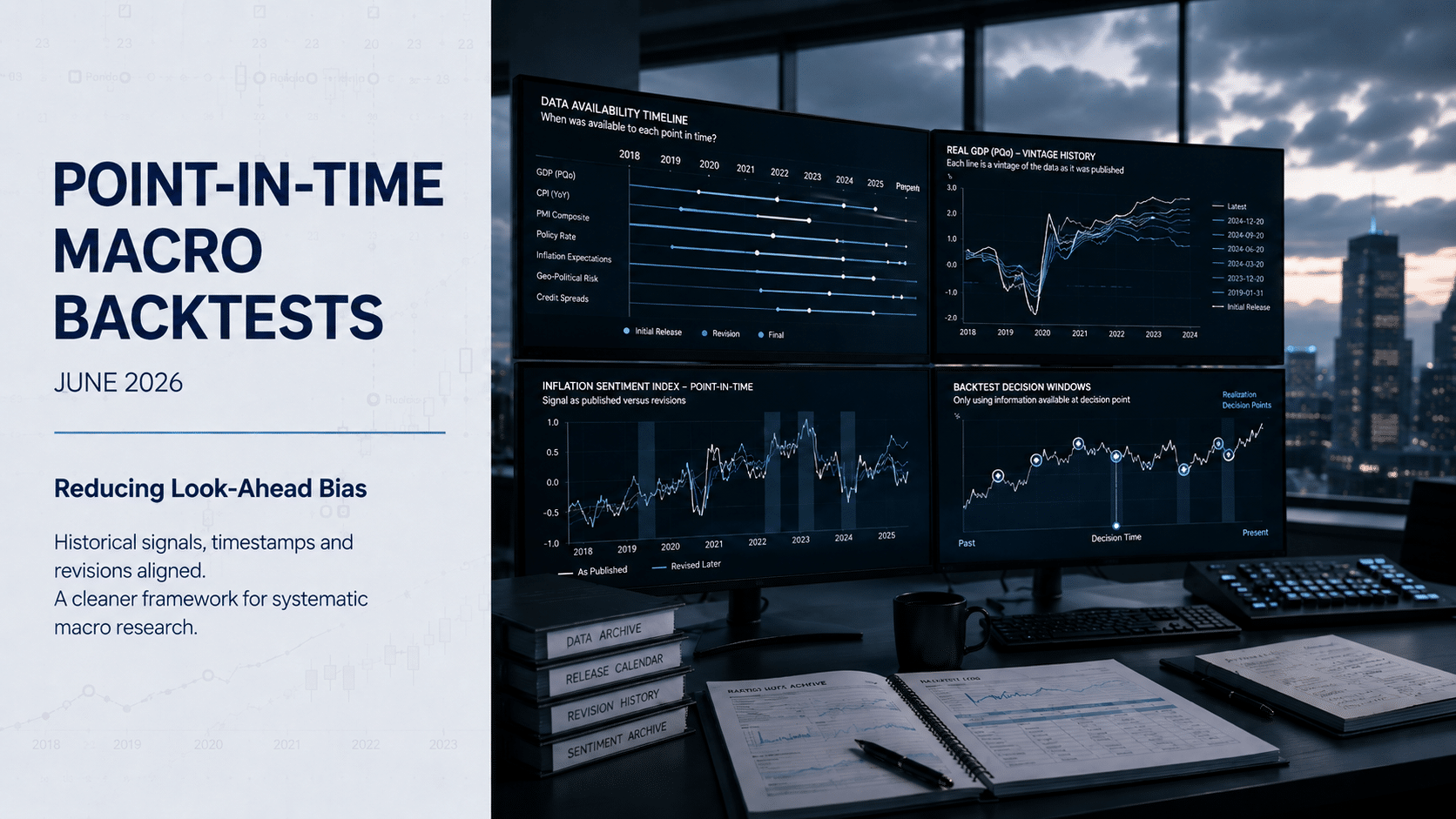

Point-in-time datasets improve macro backtests by ensuring that each historical simulation only uses information available at the time of the trading decision. This helps reduce look-ahead bias, avoids overstating strategy performance and gives researchers a more realistic view of how macro signals would have behaved in live conditions.

For institutional investors, point-in-time discipline is especially important when working with macroeconomic releases, sentiment signals, news-derived indicators and alternative data. These datasets often evolve as new information is published, revised, corrected or reclassified.

Permutable structures its sentiment and macro indices with point-in-time research requirements in mind, helping quantitative teams reconstruct the signal environment that would have been observable at a given historical decision point.

Point-in-time data is historical data stored with the values, timestamps, revisions and availability status that existed at a specific moment. In macro backtesting, it helps researchers avoid using revised or future information that would not have been available when a trading decision was made. In practice, point-in-time data answers a simple but critical question:

What would the strategy actually have known at the time?

That question matters because many datasets are cleaner in hindsight than they were in real time. Economic figures are revised. Company universes change. News coverage develops. Sentiment signals evolve as new sources are published.

A realistic backtest should reflect the data environment that was observable to a properly configured strategy at the relevant decision time.

Macro strategies often depend on information that changes over time. Inflation data may be revised. GDP estimates may be updated. Labour-market numbers may be restated. Central bank communication may be interpreted differently as new speeches, minutes and policy decisions are published.

If a backtest uses the final revised dataset rather than the version available at the time, the strategy may appear more accurate than it would have been in live trading. This is particularly important for macro and sentiment-driven strategies because many signals are time-sensitive. A narrative around inflation, policy tightening, geopolitical tension or supply disruption may be highly relevant for a short period before later information changes the interpretation. Point-in-time preservation helps researchers understand whether a signal was genuinely observable, tradable and useful at the time.

Look-ahead bias occurs when a model uses information that was not available during the historical period being tested. The effect can be material. A strategy may appear to anticipate turning points, regime shifts or drawdowns when, in reality, the data used to generate those signals was only available later.

Consider a macro strategy that reacts to inflation sentiment. If the backtest uses revised sentiment scores, corrected source classifications or later-published information, the model may appear to identify inflation pressure earlier than it could have done in real time. The same issue applies to official macroeconomic data. A strategy tested on final GDP releases may behave very differently from one tested on first estimates, because the final numbers may include revisions that investors did not know at the original decision date.

To reduce look-ahead bias, every input should be aligned to its actual availability timestamp, not only the economic period or event date it refers to.

Survivorship bias occurs when a historical dataset only includes entities, assets, sources or instruments that still exist today. In macro and alternative data, it can mean excluding discontinued sources, historical data providers, countries during crisis periods or assets that are no longer actively tracked.

For macro researchers, survivorship bias can create an artificially stable view of the past. If a dataset only includes the sources, countries or instruments that survived, the backtest may understate the uncertainty investors faced at the time. Point-in-time datasets help address this by preserving the historical universe as it existed, including sources and entities that may later have disappeared, changed classification or become unavailable.

This gives researchers a more realistic view of the opportunity set and information environment that existed at each point in history.

It is useful to distinguish between two related but different data challenges.

Point-in-time macroeconomic data concerns official releases and revisions. For example, a GDP figure may be published as an initial estimate, then revised several times. A backtest should use the figure that was available when the strategy made its decision, not the final revised value.

Point-in-time sentiment data concerns signals derived from information flows such as news, policy documents, speeches, market commentary or geopolitical reporting. These signals can change rapidly as new sources are published and narratives evolve.

Both types of data require timestamp discipline, but the operational details differ. For macroeconomic data, the key issue is release and revision timing. For sentiment data, the key issue is source availability, signal generation time and whether later information has been backfilled into the historical record. A robust macro backtest should account for both.

At Permutable, we capture macro and sentiment signals with timestamps designed to support historical reconstruction. For research and backtesting workflows, this means index values can be aligned to the time they were generated and the information available at that point. This helps researchers avoid using later updates, revised classifications or future source material when testing historical signals.

In a point-in-time framework, a sentiment signal should be evaluated according to what would have been observable to the strategy at the decision time. This may include:

This structure is especially important for market sentiment analysis because narratives can change quickly. A geopolitical event may cause a sharp sentiment move for several hours before later reporting moderates the signal. An inflation narrative may build gradually across local-language sources before it appears in mainstream financial coverage. A central bank communication shift may become visible in sentiment before it is reflected in consensus forecasts.

Without point-in-time preservation, those intraday or pre-consensus dynamics can be lost or distorted.

Building a systematic macro strategy around sentiment or narrative signals requires careful attention to data timing.

This is where many backtests unintentionally introduce bias. Even if the raw data is point-in-time, derived features can become contaminated if they are recalculated using the full historical dataset with hindsight.

Regime detection is one of the most important use cases for macro-focused quant teams. Investors may want to identify transitions between inflationary and disinflationary regimes, risk-on and risk-off environments, policy tightening and easing cycles, or commodity supply surplus and deficit phases.

Point-in-time data is essential for this work because regime labels are often obvious in hindsight but ambiguous in real time. A model trained on final, hindsight-informed regimes may perform well in a backtest but fail in production. A model trained on point-in-time signals gives researchers a more realistic understanding of how early, noisy and uncertain regime transitions actually appeared.

At Permutable, our Global Macro Sentiment Indices are designed to help researchers monitor narratives across themes such as inflation, growth, monetary policy, geopolitical tension and commodities. When preserved point-in-time, these signals can support regime analysis without relying on future information.

Even with the right data, implementation errors can reintroduce bias. Common pitfalls include:

Before relying on a macro backtest, researchers should be able to answer the following questions:

If the answer to any of these questions is unclear, the backtest may be overstating live-trading potential.

For institutional investors, backtesting is not only about finding attractive historical returns. It is about determining whether a strategy is robust enough to justify research time, capital allocation and operational implementation. Point-in-time discipline supports that process by making backtests more realistic.

It helps quantitative researchers avoid false positives. It gives portfolio managers more confidence in signal behaviour. It supports risk teams that need to understand how a model would have behaved under historical stress. It also improves communication between systematic and discretionary teams by making the evidence base clearer.

In macro investing, where data is revised and narratives evolve continuously, this discipline is particularly important.

Point-in-time datasets are not a technical luxury for serious quantitative research. They are a requirement for credible macro backtesting. Without point-in-time discipline, backtests may overstate performance, understate uncertainty and hide weaknesses that only appear in live trading. By structuring research pipelines around availability timestamps, revision history and historical source universes, investors can test strategies against the information environment that actually existed at the time.

At Permutable, we support this approach by delivering timestamped macro and sentiment data designed for institutional research workflows. For teams using narrative intelligence, macro sentiment or alternative data in systematic strategies, point-in-time preservation helps bridge the gap between attractive historical analysis and investable live signals.

The goal is not to build the best-looking backtest. The goal is to validate strategies that can withstand real-world conditions.

Point-in-time data captures information as it was available at a specific historical moment, including original values, publication timestamps, revisions and availability status. In finance, it helps researchers backtest strategies using only the information that would have been observable at the time.

Look-ahead bias allows a model to use information that was not available when a historical trading decision would have been made. This can inflate performance, improve apparent timing and make a strategy look more robust than it would have been in live trading.

Survivorship bias occurs when a dataset only includes assets, entities or sources that still exist today. This can make historical results appear stronger or more stable because failed, delisted, discontinued or unavailable entities are excluded.

Macro sentiment signals can change quickly as narratives evolve. Point-in-time preservation allows researchers to see what a sentiment index showed at the moment a decision would have been made, rather than using a later or revised interpretation.

The event date refers to the period or event a data point describes. The publication date is when that data became available. A macro backtest should use publication or availability timestamps, not only event dates, to avoid using information too early.

Quant teams can implement point-in-time data by storing availability timestamps, separating original and revised values, preserving historical source universes and ensuring all derived features are calculated only with information available at each decision point.

Permutable provides timestamped macro and sentiment indices designed to support institutional research workflows. These signals can be aligned with historical decision windows, helping researchers test macro and narrative signals without relying on future information.

15 Jun 2026

Permutable AI is now Permutable

Read more >

Opinion

15 Jun 2026

Permutable CEO Wilson Chan on AI agents in investment management, macro intelligence and commodities markets

Read more >

Announcement

10 Jun 2026

Permutable Wins Hedgeweek® Technology Provider of the Year: Innovation

Read more >