By early-2026, UK economic sentiment is still mixed, consistent with inflation risk easing but not fully cleared.

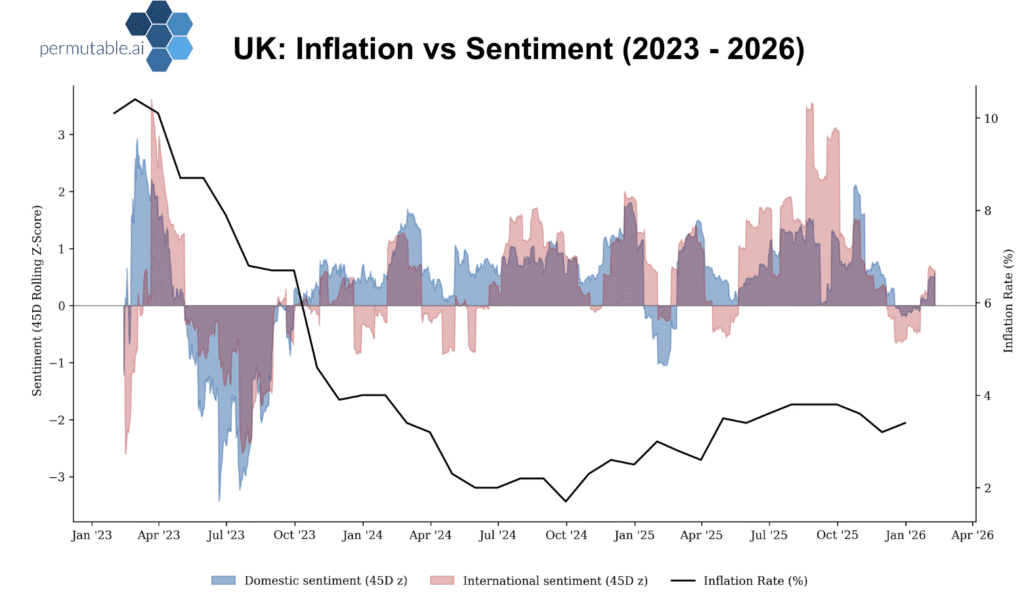

The inflation chart explains why the MPC still sounds restrictive. International inflation sentiment spiked in mid-to-late 2025 even as realised CPI moved only gradually. Expectations can reprice faster than the data, raising persistence risk. That keeps policy cautious.

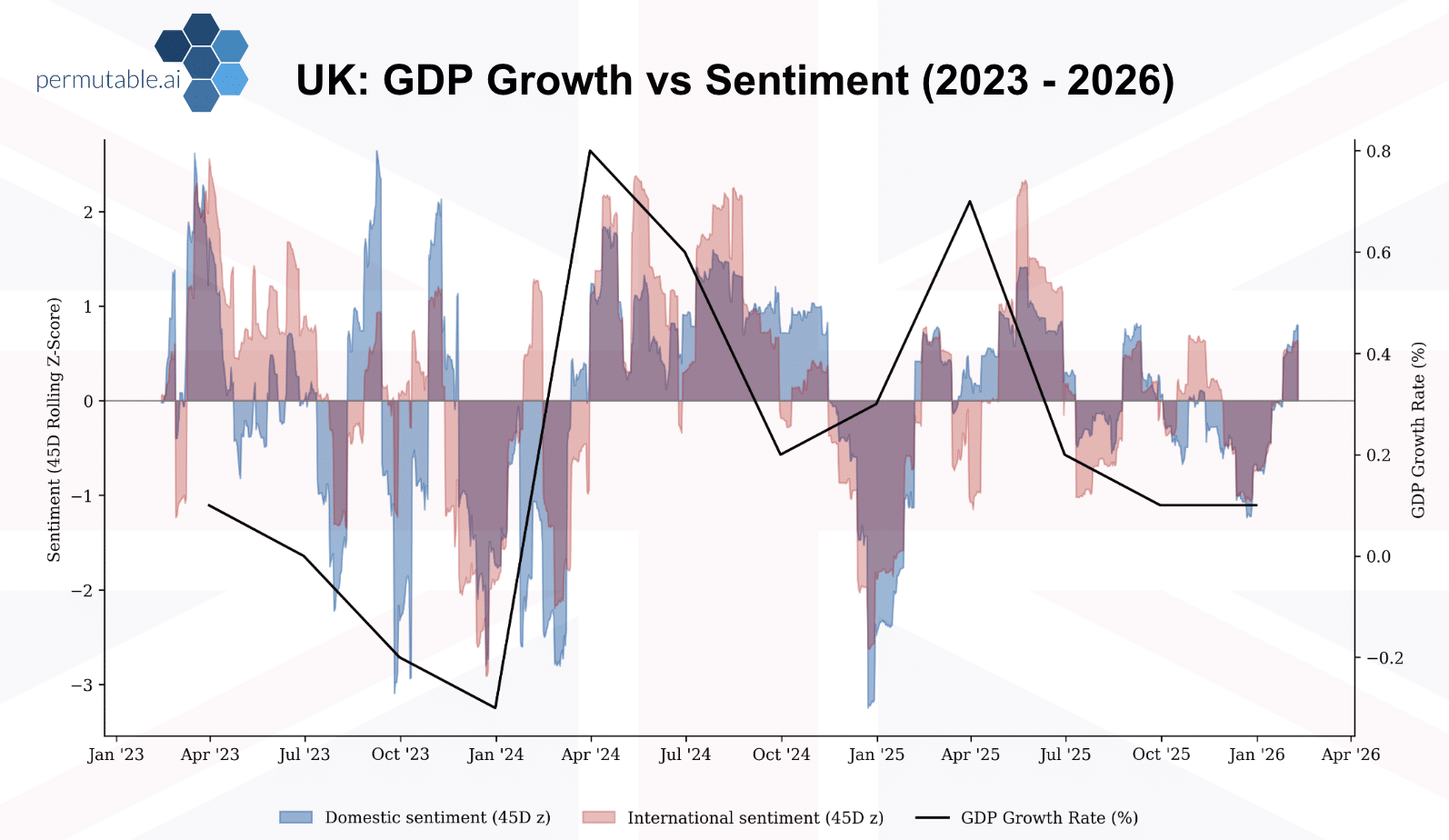

The central bank faces a classic dilemma. Cut too slowly, and rates continue to bite. Cut too quickly, and inflation expectations risk re-anchoring higher. In a 0.1% growth world, policy sensitivity increases.

The outlook for 2026

Several factors will persist in 2026. Household squeeze lingers. Public spending restraint intensifies. Investment caution stays. The result is an economy that may continue to post positive quarterly prints, but struggles to fly above the clouds.

That implies annual growth in 2026 potentially undershooting 2025 or staying put, unless policy impetus and economic sentiment improve materially.

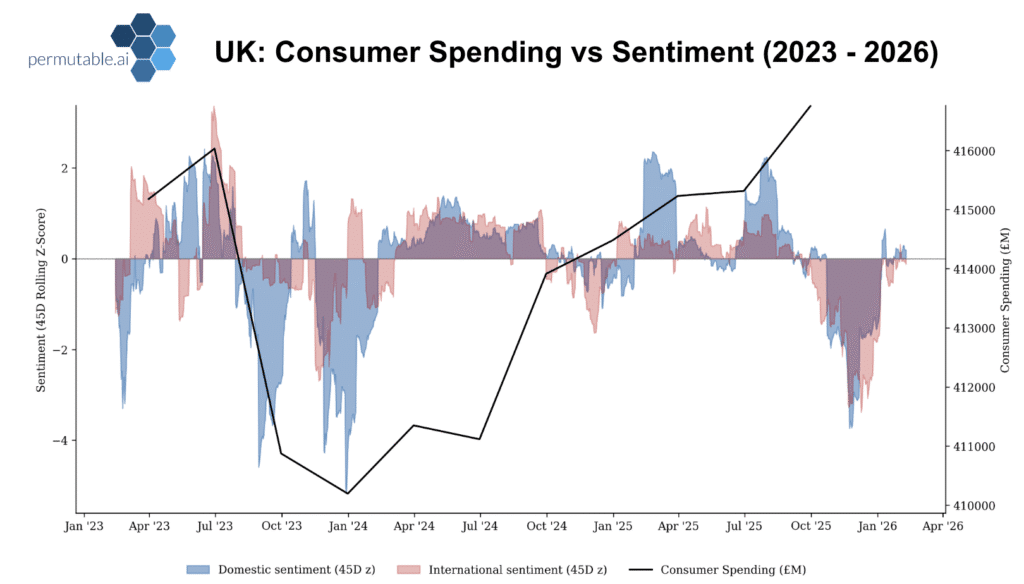

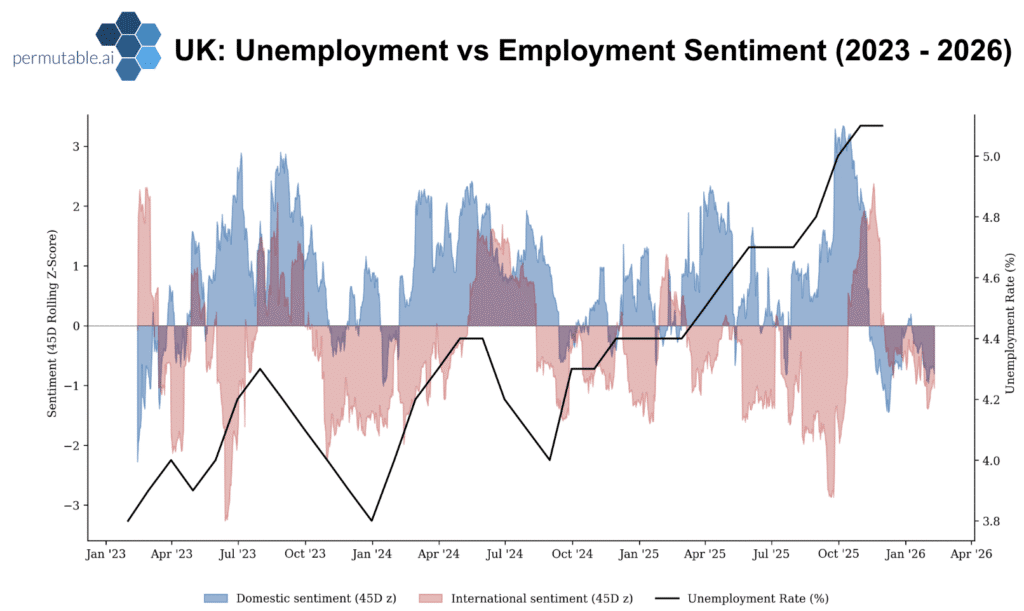

At present, UK economic sentiment remains fragile across domestic demand, hiring and investment narratives, reinforcing the base case of flat momentum rather than recovery.

Track the macro in real time

Our Regional Macro Indices are built as a top down read on macro heartbeat of the UK, a continuous hourly sentiment score. We ingest and group thousands of UK relevant narratives each day, then structure them into a hierarchy of signal layers:

Top down macro regime: politics, fiscal stance, monetary policy, growth and inflation framing.

Demand and activity: consumption, services momentum, discretionary versus essentials, confidence language.

Investment and labour: business intent, hiring and wage pressure, redundancy and cost cutting tone.

Cost of living and pricing power: food and energy price sensitivity, margin squeeze narratives, pass through language.

Transmission markers: whether stories describe intention, constraint, or realised activity, so we can separate noise from genuine turns.

Crucially, the indices also split domestic UK economic sentiment from international narratives about the UK. That separation tells you whether weakness is home grown (policy, demand, labour) or externally driven (global cycle, trade, financial conditions). Q4 simply validated what the sentiment layer had already confirmed with domestic lens rolled overing into negative during late 2025. The edge is seeing what is happening now in 2026, while hard data plays catch up.

What to watch next is the composition. If domestic sub pillars stabilise and begin to converge with international tone, that typically foreshadows a modest lift in services, investment and growth before it appears in ONS releases. If the domestic layer stays weak and fragmented, the UK remains in low gear. The signals are live, and any turn will show up in the sentiment first.

Want to see what Q1 is signalling before the ONS reports it? Our Regional Macro Indices give systematic teams and macro desks a real time edge on UK momentum. Get in touch at enquiries@permutable.ai or request a private institutional walkthrough below.