In this article we look at the market dynamics driving aluminium prices in Q4 and the outlook ahead for 2026. Aluminium enters Q4 on a firmer footing as prices rally to a three year high. What counts now is the price and availability of power, not the noisier swings in inventories. Aluminium supply is tightening quietly as policy constraints bite and logistics do only so much to lift output. Market sentiment has picked up at the margin and our Trading Co-Pilot captures that turn, even as the physical read stays firm. The stage for 2026 is one of scarcity, macro unease, segmentation and higher cost floors.

Table of Contents

ToggleQ4 prices: the message in the market

From the start of September to 9 October, the CME rose to $2,740/mt while the LME cash rose a little over 5% from roughly $2,610/mt to $2,786/mt. The 3-month minus cash spread narrowed from backwardation to almost flat by late September and has hovered near zero since, a configuration that points to tight conditions with potential for further squeeze. In China, the silver metal continues to be dearer: Shanghai metals market price sits around $2,940/mt versus $2,786/mt on the LME. FX, Tax and contract terms differ, yet the signal read stays consistent: domestic policy and power restraints keep China priced on the upside than the international benchmarks.

Stock signals

Inventories on paper have risen while prices advanced. The detail matters. LME stocks fell about 55k tonnes in September to 415k, then rose into early October, reaching 508k on 9 October 2025. Much of that build reflects warranting and reshuffling, not easier access to material. Looking past the headline stocks: regional premia and elevated cancellations are the truer read of dynamics in the aluminium market. Our Trading Co-Pilot captured the signal in real time, macro tone softened, logistics stayed tight, pointing to smoother mechanics rather than softer fundamentals.

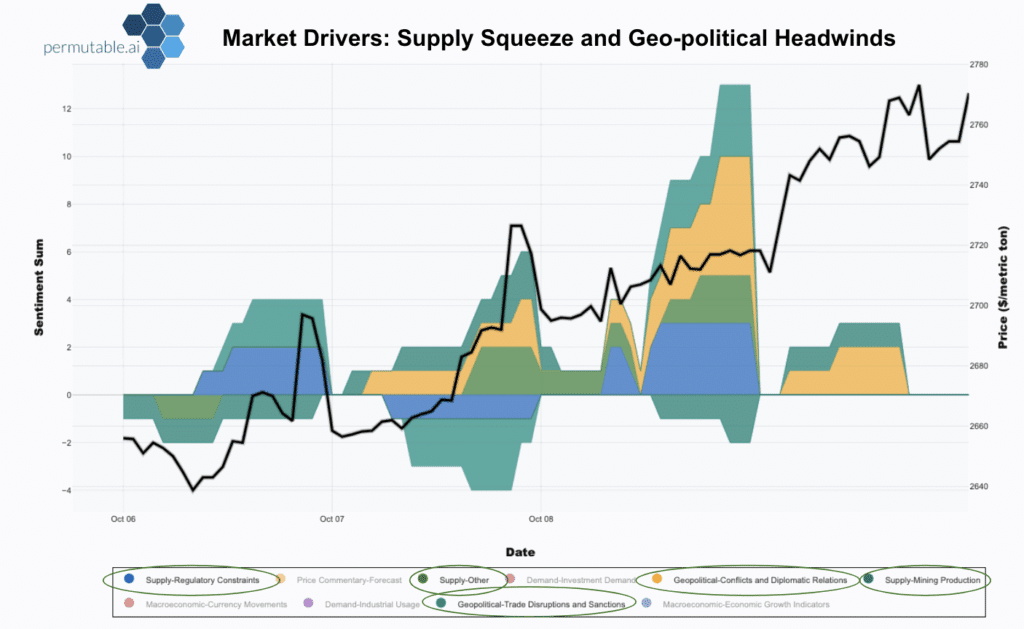

Supply constraints and trade headwinds

China’s policy mix is the main throttle on supply. Primary capacity is effectively capped near 45 million tonnes annually, with utilisation hovering close to 98%, leaving minimal headroom. Incremental output now depends on capacity swaps, requiring new smelters to be built only when an equivalent amount of old capacity is retired to meet energy-efficiency thresholds. Aluminium remains an electricity-intensive business. Hydropower regions wane with rainfall sparse; coal-heavy hubs faced with higher hurdles and environmental limitations restricting output. New projects are migrating to renewables-rich provinces in the west or bordering China, which demands grid investment and carries extra risk.

Outside China, India and Indonesia are adding capacity, but Europe still carries the scars of earlier curtailments with power costs and outages, keeping regional premia supported and input costs elevated. Trade barriers add another layer, US tariffs and China’s removal of the 13% export tax rebate on many aluminium products have reduced export elasticity and prolonged regional price gaps. In the aluminium market, that means the marginal tonne is increasingly determined by power availability rather than nameplate capacity.

Secondary markets

Inputs into aluminium, such as Bauxite, as well as Alumina have been a major swing factor. Alcoa’s Kwinana closure in Australia reflects ageing assets and diminishing bauxite grades, alongside persistent cost strain. FOB Australia alumina has fallen sharply over the last year, compressing refinery margins and muddying the mining outlook. Scrap is now pivotal. Tight raw-material availability and low grade inputs has pushed scrap and secondary alloy prices higher in step with primary.

Secondary producers are attempting to pass through higher costs, yet rising finished-goods inventories and cautious purchasing by downstream users suggest any further price gains will likely be more measured. October should stay firm, but the path beyond hinges on industrial demand and scrap availability. Our Trading Co-Pilot’s sectoral sentiment picked up persistent signals of bottlenecks and wider spreads in regional scrap markets, classic precursors of tighter secondary supply and stickier premia.

Demands structural pull

The upstream arises from cyclical demand, which appears to be gathering steam. Transport and consumer tech goods are growing modestly, construction is soft but not capitulating. What is clear is that the energy transition provides a durable pull via grid build-out, cables, solar and power equipment. The more recent thematic trend is the swift rise in data-centre investment. In the US, data centres are on track to double their share of electricity consumption by 2030, tightening local power markets and nudging aluminium’s long-run cost higher. That same build-out lifts demand for aluminium-intensive wiring, electrical gear, and cooling systems. Our Trading Co-Pilot picked up on the firming demand, orders and grid expansion, showing the aluminium market is increasingly tied to data-centre and energy intensive build-outs as well as transport and tech goods.

What our Trading Co-Pilot captures

- Macro accommodation: A sustained shift in Fed-related language, regional growth and risk appetite raised the outlook for metals market when fundamentals are tight.

- Prompt tightness: Clusters of references to cancelled warrants, firm premia and intermittent power curbs point to a physically constrained market even when headline stocks drift higher.

- Policy enforcement: Increased mentions of “replacement before expansion”, energy-intensity thresholds and relocation of hubs.

- Input strain: The awkward pairing of lower alumina prices with negative refinery margin remarks often foreshadows capacity attrition.

- Scrap stress: Persistent notes of tight scrap supply and secondary price pass-through, tempered by finished-goods inventory build, argue for firmness now but a shallower ascent without stronger end-use pull.

Themes to watch

- Energy shifts: Power cost, energy constraints and tariffs will set the tone of new metal production with refineries under pressure.

- Regional Premia: Trade and policy choices are segmenting markets; expect China’s and North American premia to remain sticky.

- Secondary markets: Ambitions for improved outlook for secondary metals market by 2026 hang in balance.

- Industrial Usage: Data-centres, green transition and EV growth competes for raw material and power demand, deepening industrial use for aluminium-heavy infrastructure.

- Input fragility: Watch alumina margins, bauxite quality, scrap flows and refinery utilisation for the next shift in market dynamics.

Outlook for 2026

Looking ahead, modest demand growth coupled with a supply squeeze should keep prices supported and regional premia sticky. Trade routes will continue to re-shape, with China near its capacity ceiling and power availability the decisive constraint across hubs. The near-term sentiment will hinge on three swing variables: alumina and bauxite supply (and refinery margins), renewables and power headwinds in smelting regions, and scrap availability across secondary circuits.

Our Trading Co-pilot will continue to pick up on signals and conditions through the market structure, cancelled-warrant share, regional premia and scrap flows, not headlines widely reported such as inventories, which can be distorted by warranting and reshuffling. On this path, a gradual move toward the low $3,000s in 2026 remains a reasonable central case, with setbacks if growth softens or energy costs ease.

Where signals meet strategy

With the Aluminium market in a fine balance between constrained primary supply and slow-burning structural demand leave the dynamics walking a tight rope. Our Trading Co-Pilot continues to show where market dynamics and sentiment are strengthening, or fraying, so our clients strategy can adapt in real time.

Stay ahead in aluminium and industrial metals. We turn real-time narrative shifts, macro, energy prices, policy constraints, and supply frictions – into actionable sentiment and insightful reads through our industrial metals intelligence. For institutional access to our API and Trading Co-Pilot contact us at enquiries@permutable.ai