In this article we examine the precious metals outlook, looking at the factors behind the latest sell-off, focusing on how shifting risk appetite has shaped price action and what lies ahead into 2026. At present, gold sits at $4,115/oz (9.6% m-o-m) and silver at $48/oz (10.0% m-o-m). Both remain near record territory despite this week’s shake-out, with gold and silver down 5.5% and 7.3% respectively as crowded longs were pared after a blistering run.

Gold and silver are attempting to steady after Tuesday’s retreat, having briefly dipped to $4,030/oz and $47.3/oz. Dip-buyers were active as prices neared around the psychological $4,000 range.

After an overheated climb to the $4,370 highs, the correction had room to run. The bigger swing factor is risk appetite. Renewed hopes that US-China talks will avert further tariff escalation have trimmed the safe-haven bid. Market chatter skews modestly bearish as participants digest the pullback. Yet the wider backdrop still carries constructive strokes. Policy easing expectations are alive, US fiscal headlines are messy, and geopolitics continues to hum in the background, keeping a layer of uncertainty in place. All told, the precious metals outlook points to consolidation at elevated ranges while policy and geopolitics keep a floor in place.

The upshot is a clear shift in positioning and risk appetite. The bias remains softer while the mooted double-top governs and traders orbit CPI and Fed guidance. Under the noise, dovish Fed expectations and macro-political unease still offer support to the precious-metals regime even as profit-taking plays out.

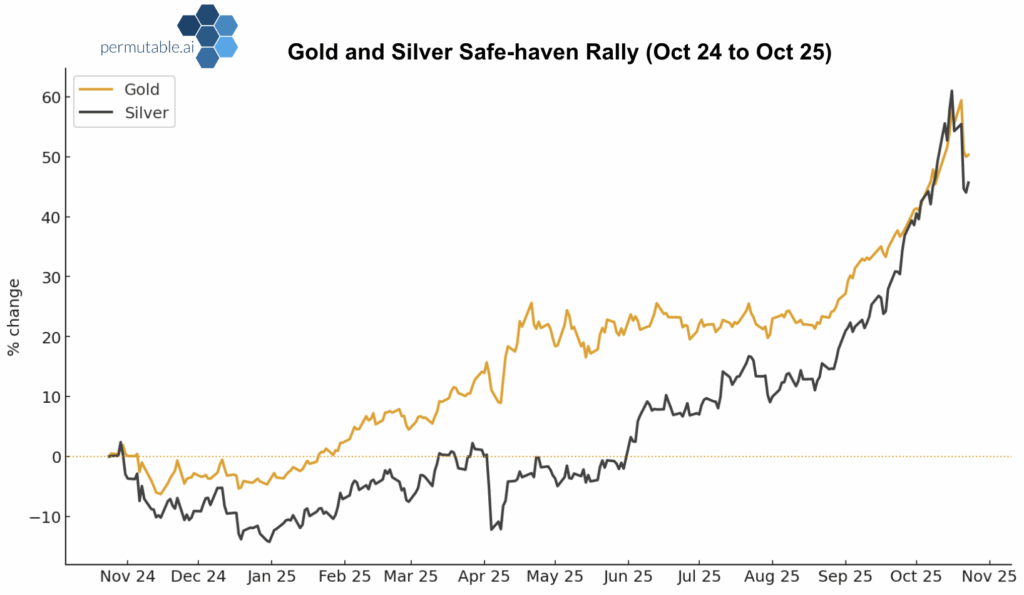

In our precious metals outlook, gold is doing the heavy lifting, with silver following. This is textbook cooling in risk appetite rather than a change in regime. A firmer dollar, a touch more confidence in risk assets on tentative US-China thaw signals, and straightforward profit-taking after recent Fed cuts have reduced the urgency of the safe-haven bid. Notably, the slide arrived while nominal and real yields edged lower, pointing to positioning and FX as the prime drivers. In short, this reads as resilience at higher ranges, not a thesis in retreat.

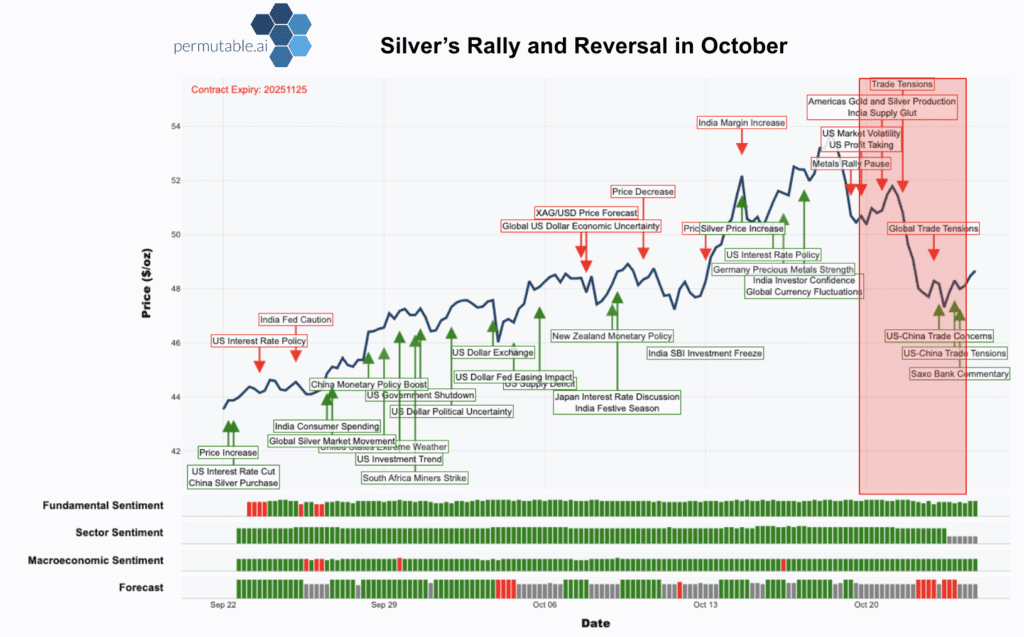

Our Trading Co-Pilot flagged the turn in real time. From early October, the Fundamental, Sector and Macroeconomic Sentiment layers flashed persistently green, clustering around rate-cut hopes, central-bank accumulation and trade tension as price momentum gathered. Into 19 October, headlines around a US-China thaw and easier policy coincided with a swift drawdown. The Forecast layer flipped from constructive to neutral, then to red across 21-22 October as global risk appetite pivoted and the dollar firmed. The Forecast layer captured the short-term downside cleanly, while the Fundamental Sentiment stayed broadly bullish, consistent with orderly de-risking of stretched positions rather than a break in underlying market tone. That sequence underpins our precious metals outlook for choppy but supported trade.

Silver mirrors gold’s macro impulse but with a firmer industrial spine. Demand from renewables, electrification and technology adds support, while higher beta amplifies the swings. At present it is trading around $47.60 to $48.80/oz after the week’s setback, roughly -8% below the $53.34/oz high set this month. The longer-term tone remains upbeat, solid industrial offtake and a fifth consecutive year of supply deficit continue to provide a floor.

What our Trading Co-Pilot Captured:

Attention has rotated from havens toward riskier growth. The speed of the drop simply reflects how extended the run had become, a correction, not a collapse. Even after the pullback, gold is up 50% y-o-y and silver 60% y-o-y, one of the strongest years on record. Prices have shifted to a higher plane and now swing more widely as sentiment toggles between growth and caution, exactly what our layers have mapped in recent weeks.

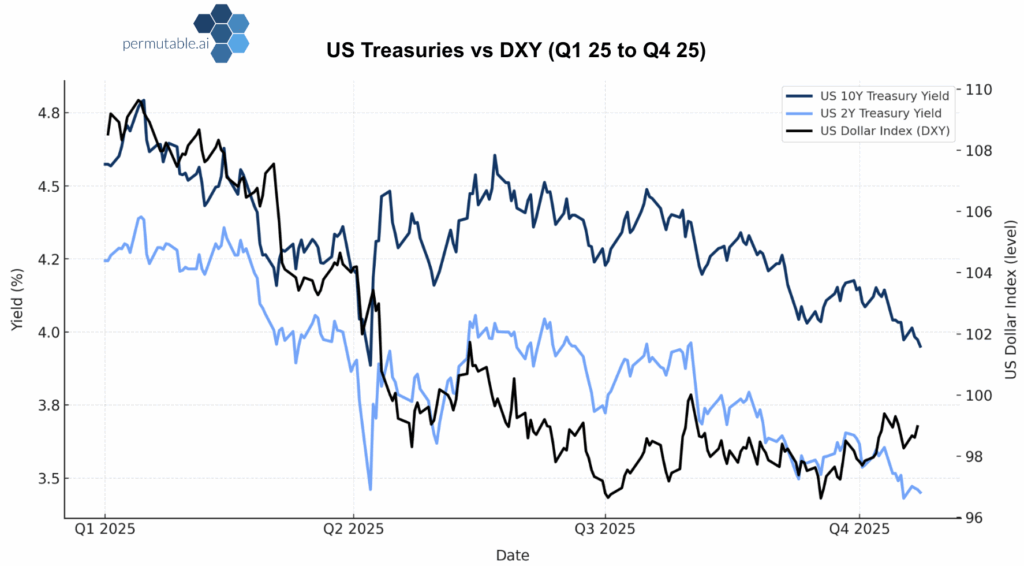

Falling US2yr and US10yr yields coupled with a softer DXY lower the opportunity cost of holding gold, supporting precious metals outlook. The late-Q4 dollar bounce helped tempered the precious metals outlook providing a tailwind: sustained USD strength or a snap higher in real yields would cap rallies, while softer US data and clearer Fed easing path would re-ignite upside.

Nonetheless, throughout 2025 investors have navigated slower global growth, lingering inflation pressure and a cautious policy path. In that setting, gold has acted as a portfolio backstop, absorbing capital when confidence wobbled and when the dollar softened. Crucially, strategic demand has done the heavy lifting. Central banks, including China, India, Poland, Uzbekistan and Kazakhstan, have continued to add to reserves as part of diversification and resilience building. These flows do not chase moves. They provide a structural floor.

A second dependable pillar of demand arises from the Asian retail and household buying, the part that does the quiet work. In India and China, seasonality and culture keep jewellery and bullion purchases alive on dips. When fast money stepped back, the patient bid did not; it leaned in, helping prices stabilise faster than in prior ETF-led pullbacks. The data bear this out. Shanghai Gold Exchange withdrawals rose to 118 tonnes in September 2025, while local ETF subscriptions and futures turnover reached fresh highs, evidence of active household participation alongside nimble trading. In India, bar and coin demand was about 7% higher through mid-2025 as families bought into festival and wedding seasons despite elevated prices. Flows are consistent with this pattern: a ten-month high in August imports and solid September ETF inflows point to a steady buy-the-dip rhythm that keeps the complex anchored.

Heading into 2026, the precious metals outlook is buttressed by a measured easing cycle, modest growth rather than a hard landing, and steady structural demand that should keep the long-term bullish hedge bid alive. Political and trade frictions are a drag on risk appetite and continue to tilt portfolios toward assets outside sovereign liabilities. Gold fits that brief. Silver tags along, with more uplift when industrial demand holds firm.

This week’s sell-off reflects a cooler, more balanced risk appetite, not a broken story. Strategic buyers have done the quiet work all year. Central banks and households have steered precious metals to new heights. Our Trading Co-Pilot captured the shift in real time, flagging near-term downside as the dollar firmed, while Fundamental and Macro layers remained supportive. Together, they point to a robust foundation for gold and, by extension, resilience across the precious-metals complex. For portfolios, the precious metals outlook argues for staying hedged while leaning into the structural bid.

We turn real-time narrative shifts across metals, macro, and FX risk into clear, usable signals that help clients stay on top of trading strategies.

For institutional access to our API and Trading Co-Pilot, contact enquiries@permutable.ai to request a demo.

01 May 2026

Aluminium and copper outlook 2026: Separating scarcity from demand risk

Read more >

30 Apr 2026

Commodity shock transmission: How real-time sentiment signals reveal market moves before price adjusts

Read more >

30 Apr 2026

Weekly current precious and industrial metals sentiment: Is bullish momentum returning or fragmenting across markets?

Read more >