Neural networks for trading systems – applications and use cases

25 Sep 2020

25 Sep 2020

Neural networks are artificially created structures built into programs that are loosely modelled on the human brain. Neural networks have a wide range of applications including medicine, customer services, self-autonomous driving, and increasingly sophisticated trading systems. They are used for solving many business problems including sales forecasting, customer research, data validation, and risk management.

Neural networks generally learn through supervised learning tasks by examining many examples of labelled data and building knowledge from that information. A neural network continuously “rewires” itself until it can solve a problem. Because a neural network is made up of neurons (much like the fundamental units in our brains) connected to each other, based on the data it learns from, these neurons will eventually change size to form a correct path. This path is the same as what people would call “understanding”.

Above: An example of a neural network typically used for image recognition, used for classification of trading patterns within a market data time series.

The financial markets have become one of the most exciting frontiers for neural network applications. Modern trading firms are leveraging these powerful tools to gain competitive advantages in increasingly sophisticated ways.

Neural networks, particularly recurrent neural networks (RNNs) and long short-term memory (LSTM) networks, are being used to predict short-term price movements, forecast volatility and momentum, and model non-linear dependencies in time series data. These models are trained on historical prices, order book data, macroeconomic indicators, and even alternative data sources like social media sentiment. The ability to process complex temporal relationships makes these networks particularly well-suited for financial forecasting where traditional linear models often fall short.

By feeding in structured and unstructured data – including news sentiment, trading volumes, and market microstructure data – neural networks can output buy/sell signals, probability-based forecasts for asset movements, and confidence-weighted directional signals for portfolios. This capability is fundamental to quantamental and AI-assisted systematic strategies that combine quantitative analysis with fundamental insights.

Advanced neural networks, often employing deep reinforcement learning models, are being applied to dynamically allocate capital across assets, manage exposure based on predicted risk levels, and simulate scenarios whilst adapting trading behaviour in real time. These systems can process vast amounts of market data to make split-second decisions about position sizing and risk management.

Transformer-based networks like BERT or GPT variants are extracting actionable signals from market-moving news headlines, earnings calls and financial filings, and social sentiment from platforms like Reddit and Twitter. These insights feed directly into quantitative models for event-driven trading and macro strategies, allowing traders to react to market sentiment before it’s fully reflected in prices.

Neural networks are being used to predict short-term order book dynamics, optimise execution to minimise slippage, and design smart order routing strategies. This application is particularly vital for high-frequency and low-latency traders who compete on microsecond advantages.

Improved Alpha Discovery: Neural networks excel at uncovering hidden, non-linear patterns that traditional models like ARIMA or linear regression often miss. This capability is crucial in markets where obvious patterns are quickly arbitraged away.

Adaptability: Deep learning models can retrain on new data, allowing for regime-aware strategies that evolve with changing market conditions. This adaptability is essential in financial markets where relationships between variables can shift dramatically.

Multimodal Input Integration: Neural networks can fuse structured data (price, volume) with unstructured data (text), unlocking signals across different domains and creating more comprehensive trading strategies.

Edge in Crowded Markets: In saturated quantitative spaces, neural networks can offer a differentiated edge when traditional factor models converge and become commoditised.

Overfitting: Due to their complexity, neural networks can learn noise instead of genuine signals, especially in low-signal-to-noise environments like financial markets where randomness is prevalent.

Interpretability: The black-box nature makes it difficult to explain decisions – a significant problem for compliance, risk management, and investment committees who need to understand model behaviour.

Data Requirements: Neural models require large volumes of high-quality data. In finance, reliable labelled data with ground-truth outcomes is often limited and expensive to obtain.

Regime Sensitivity: Models may perform excellently in one market regime but fail catastrophically when underlying dynamics shift, such as during financial crises or major structural market changes.

Operational complexity: Maintaining and retraining models, monitoring for drift, and integrating them into real-time infrastructure poses significant technical challenges for trading firms.

Traditional quantitative trading relied on linear regressions, factor models focusing on value and momentum, rule-based backtesting, econometric indicators, and manual feature engineering. The neural network-based approach has transformed this landscape through LSTMs and Transformers, learned latent representations, reinforcement learning combined with simulation, news and NLP-driven alternative data feeds, and automated feature extraction.

At Permutable, our team is at the forefront of applying neural networks to extract meaningful signals from global news and macroeconomic data for use in trading strategies. Our Trading Co-Pilot intelligence suite offers a practical case study in how deep learning is shaping modern systematic trading.

At Permutable, we use transformer-based neural networks – similar to BERT and GPT models – to process over 1 million global news articles per day. These models classify sentiment across multiple entities, asset classes, and topics in real time. For example, a spike in negative sentiment related to geopolitical instability in oil-producing regions can trigger risk-off signals in energy portfolios.

By combining sentiment layers with structured economic indicators, the neural network outputs can help traders anticipate market reactions before they become priced in — a significant alpha opportunity for systematic strategies.

Rather than analysing sentiment at the document or headline level, our neural networks employ multi-entity sentiment classification. This approach allows the model to distinguish between how different commodities and currencies, or companies are perceived within a single article. For instance, the same news story might generate a bullish sentiment for wheat and bearish sentiment for soybeans – critical granularity for commodities traders.

This fine-grained classification is used in our Trading Co-Pilot to deliver actionable intelligence directly into the hands of traders, analysts, and quants managing complex portfolios.

Our platform’s ability to continuously retrain on new data, using reinforcement learning and neural tuning, means it adapts to market regime shifts. Whether during periods of high volatility or calm, the models learn to weight different data sources and sentiment types appropriately – offering a regime-aware insight engine for trading operations.

Our models also include smart news filtering layers that suppress irrelevant or low-confidence content. This addresses a major challenge in neural network applications: noise reduction and model robustness. By enhancing signal clarity, traders gain a clearer picture of which events are likely to move markets – and which are not.

At the time of writing this update, the industry is moving towards hybrid models that combine traditional quantitative factors with deep learning overlays, providing the best of both approaches. There is a growing focus on making neural network decisions more transparent for both traders and regulators. Meanwhile, synthetic data generation is being explored to improve training datasets and reduce overfitting risks whilst edge deployment technologies are being developed for ultra-fast model inference in high-frequency trading environments.

In trading, neural networks are creating new possibilities for alpha generation whilst presenting unique challenges that require careful consideration and sophisticated risk management approaches. As these technologies continue to evolve, they will likely become even more integral to both business operations and financial market activities.

See how our neural networks turn global noise into alpha-generating intelligence with Trading Co-Pilot. Email our team at enquiries@permutable.ai to request a demo.

Analysis

15 Jul 2026

The Price of Passage: How Geopolitical Sentiment Led the Repricing of Gulf Crude-Flow Risk

Read more >

Analysis

08 Jul 2026

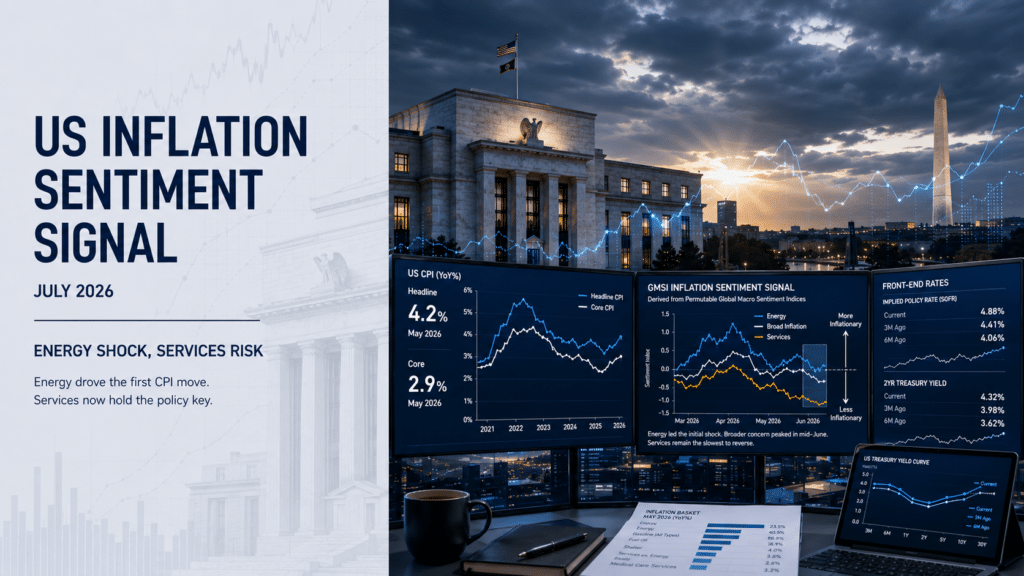

US inflation sentiment signal shows shift from energy shock to sticky services risk

Read more >

Analysis

07 Jul 2026

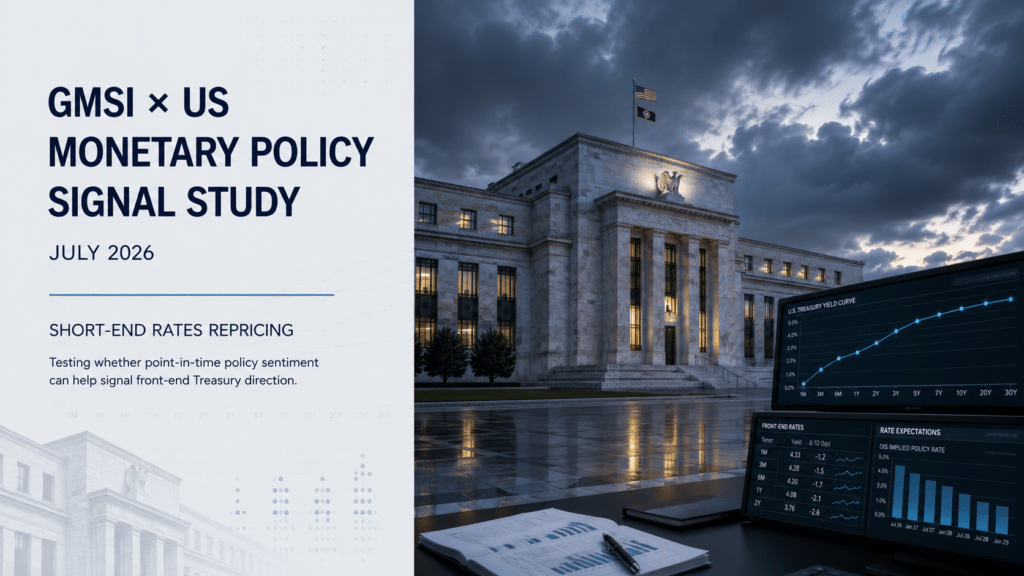

Testing GMSI US monetary policy sentiment as a short-end rates signal

Read more >