How our news sentiment indicators delivered consistent edge in 2025

19 Dec 2025

19 Dec 2025

This article explains how news sentiment indicators were operationalised in 2025 to deliver consistent, risk-adjusted performance in commodities markets. It shows how structured analysis of news, narrative and events improved entry and exit timing ahead of consensus. The article is aimed at quantitative funds, CTAs, and institutional investors exploring sentiment as a systematic trading input.

Over the past decade, systematic trading has become increasingly competitive. Faster execution, broader datasets and tighter spreads have steadily compressed traditional sources of alpha. By 2025, many commodity trading advisors were operating in an environment where returns were harder to extract and drawdowns more difficult to control. In this context, it became clear that relying solely on price, positioning and static fundamentals was no longer sufficient to explain short-term market behaviour.

Markets were increasingly moving on interpretation rather than on raw data. Narrative momentum, shifts in sentiment and changing perceptions of risk often began influencing price before policy actions or macro releases fully played out. This shift created the conditions for sentiment to move from a descriptive concept to an actionable trading input.

Sentiment has always existed in markets, but historically it was difficult to measure, structure and integrate into systematic models. What changed was not investor psychology, but the ability to capture narrative flow at scale and in real time. By 2025, advances in data ingestion and AI-driven classification made it possible to treat sentiment as structured signal data rather than subjective commentary.

Crucially, sentiment became valuable not as a standalone indicator, but when mapped explicitly to macro and fundamental drivers. When narrative intensity, tone and persistence began aligning with identifiable events such as policy shifts, supply disruptions or geopolitical escalation, sentiment could be used to anticipate market behaviour rather than simply explain it after the fact.

Our live systematic strategy powered by our news sentiment indicators was built around a simple but disciplined principle: trade events and narratives, not just prices. The strategy operated across highly liquid front-month commodities futures, allowing for efficient execution and scalability. Exposure was maintained in a balanced long-short structure, with no structural directional bias, ensuring that performance was driven by signal quality rather than market drift.

Signals were generated by mapping sentiment and narrative dynamics directly to macroeconomic, geopolitical and supply-side drivers. This ensured that each position reflected an underlying explanation for why a market was moving, rather than a purely statistical relationship. By anchoring sentiment to fundamentals and events, the strategy avoided the pitfalls of treating narrative as noise.

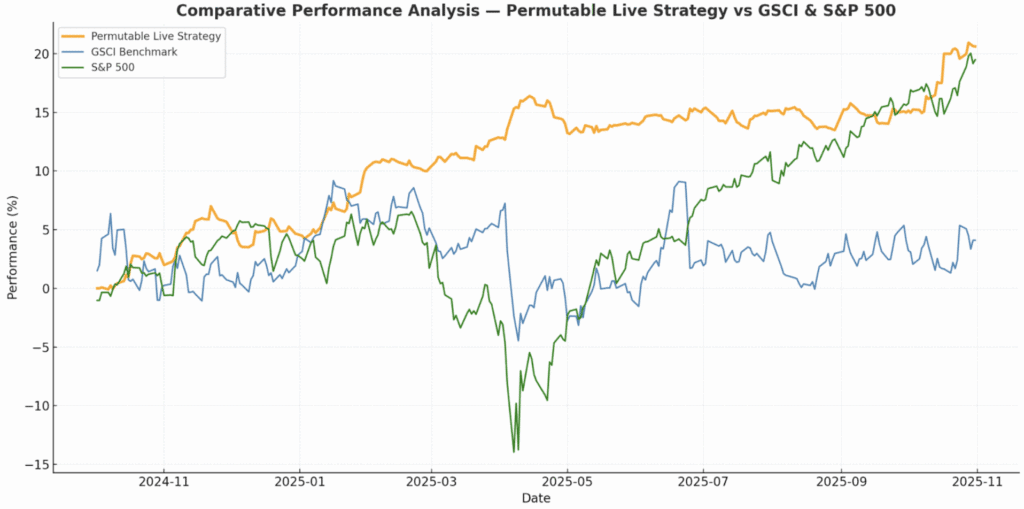

Across a twelve-month track record in 2025, the strategy delivered a Sharpe ratio of 2.85, with an annualised return of approximately twenty per cent and annualised volatility of around seven per cent. Maximum drawdown was limited to just over four per cent, while correlation to the S&P 500 remained low at roughly twelve per cent. In comparative terms, the strategy outperformed more than ninety per cent of CTAs, including widely followed benchmarks such as the S&P SGMI and GSCI.

The significance of these results lies not in the headline numbers themselves, but in their consistency and risk profile. Low drawdowns and low equity correlation reflected the ability to reduce exposure during periods of narrative instability, rather than reacting after volatility had already expanded. This behaviour is difficult to achieve using price-based signals alone.

Traditional systematic strategies often enter positions once confirmation has occurred, by which point trends are established and positioning may already be crowded. Sentiment-driven signals operate differently. They aim to detect the moment when interpretation begins to shift, when language becomes more urgent or more polarised, and when individual data points start clustering into a coherent story.

In practice, this allowed the strategy to identify entry points earlier in the lifecycle of a move and to exit positions as narratives became saturated rather than waiting for price reversals. This approach proved particularly effective in commodities markets, where moves are frequently sharp, reflexive and driven by event risk rather than gradual fundamental change.

The tradability of news sentiment signals depends entirely on data coverage and structure. Our signals are derived from more than 250,000 global sources, capturing real-time news, research, policy commentary and market discourse. AI models classify events, assess tone, measure severity and track persistence over time, allowing sentiment to be treated as a time-series input rather than a static label.

Equally important is the design philosophy behind the models. The system is built to think like an investor, focusing on tradability, timing relevance and cross-asset impact, rather than on media engagement or keyword frequency. This is what allows sentiment to move from context to execution.

Although the 2025 strategy focused on commodities futures, the same signal framework is already being applied across currencies, rates and short-term macro strategies. Funds integrating these signals are not replacing their existing models, but augmenting them with an additional layer that captures how markets interpret events, not just how they price them.

This has proven particularly valuable during periods of policy uncertainty, geopolitical stress and regime transition, when traditional indicators often lag changes in market behaviour. By capturing narrative shifts early, sentiment signals provide a complementary edge to price-based models.

As markets move into 2026, one conclusion is becoming increasingly clear. Reaction speed matters less than interpretation speed. Alpha is increasingly generated by recognising when sentiment becomes self-reinforcing, when narratives harden into consensus and when markets move not because fundamentals demand it, but because perception has shifted.

The results achieved in 2025 were not the product of leverage or chance. They were the outcome of a disciplined, event-driven approach to sentiment, grounded in data and structured for systematic use. As traditional edges continue to erode, understanding the story the market is trading is becoming a decisive advantage.

At Permutable AI, we deliver these real-time sentiment and narrative signals directly to clients via data feeds and APIs, and an increasing number of funds are adopting them as a core input to their trading and risk frameworks. For institutions looking to position effectively in 2026, sentiment is no longer peripheral. It is becoming essential.

For more information on how our news sentiment signals can be integrated into quantitative investment strategies for 2026, please get in touch to discuss use cases for the year ahead by reaching out to our team at enquiries@permutable.ai.

Analysis

22 Jul 2026

UK inflation fell to 2.6% after Permutable’s Global Macro Sentiment Indices saw it coming

Read more >

Analysis

21 Jul 2026

China growth: Q2 GDP lays bare the limits of industry-led expansion

Read more >

Analysis

15 Jul 2026

The Price of Passage: How Geopolitical Sentiment Led the Repricing of Gulf Crude-Flow Risk

Read more >