In this article, we examine China’s inflation outlook as producer prices break out of a three-year deflationary run. The headline points to reflation, but the composition points to a more awkward upstream squeeze. By setting official PPI and manufacturing data alongside inflation and manufacturing macro sentiment indices, we separate domestic demand recovery from imported cost pressure moving through the factory gate. For macroeconomists, rates and FX strategists, commodity analysts, equity investors and cross-asset allocators, the question is not simply whether China is reflating. It is what kind of inflation is doing the work.

Reflation, but not the right kind

After years of factory-gate deflation, a positive turn in producer prices might normally look like relief. April appears to offer exactly that: firmer CPI, a sharp PPI turn and the long deflationary run finally broken. Beijing had spent much of the past year calling for an “appropriate rebound in prices”. April delivered a rebound, but not the kind policymakers would have chosen.

The headline offers relief; the composition offers a warning. This is not a broad revival in domestic demand, nor a property-led recovery, nor clear evidence that pricing power has returned. The pressure is concentrated in energy, freight-sensitive inputs, metals and raw materials. China is not being pulled out of deflation by demand, but pushed out by costs.

The Iran conflict matters for China less as a foreign-policy event than as an energy-import shock. Middle Eastern flows still account for a large share of China’s imported crude and wider energy exposure. Disruption around Hormuz does not just raise oil-market volatility; it feeds into the cost structure behind China’s industrial prices.

Inflation: Price Turn, Demand Still Missing

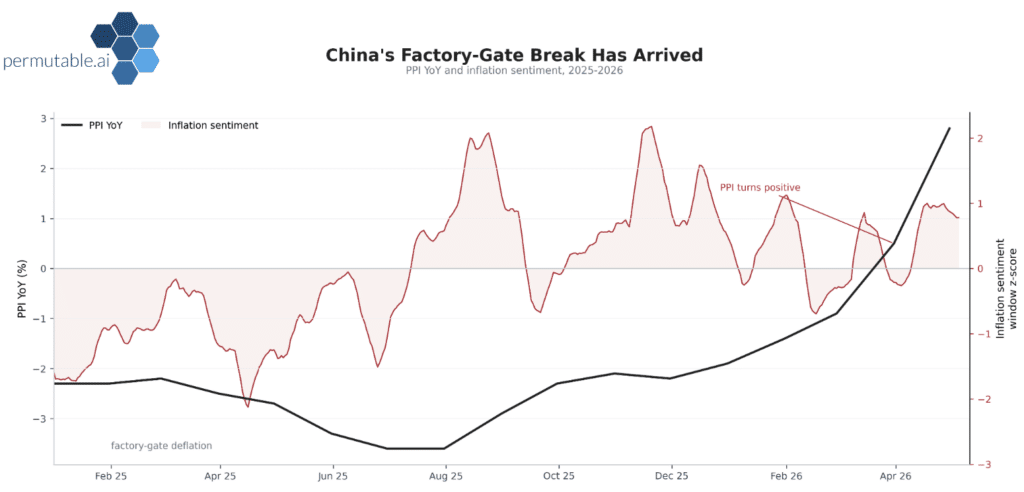

Since October 2022, China’s factory-gate data had been stuck on the wrong side of zero. By June 2025, PPI was -3.6% y-o-y, the 33rd consecutive month of decline and one of the longest deflationary runs on record. Coal, steel and ferrous metals were still grinding lower, with the property downturn acting less like a drag than an anchor.

The speed of the turn matters. PPI was still -0.9% y-o-y in February. In March, it moved back above zero for the first time since late 2022. By April, it had reached 2.8% y-o-y, a 45-month high. That is not the shape of a gradual demand recovery. It is the shape of a cost shock moving quickly through the upstream economy.

The consumer data are less dramatic, but they hum the same tune. CPI rose 1.2% y-o-y in April, up from 1.0% in March. Yet food prices continued to slide, with pork and fresh produce acting as disinflationary anchors. If this were a broad demand-led recovery, the household basket would be doing more of the work. Instead, energy-linked and non-food prices are firmer, while demand-sensitive goods remain soft. Core inflation remained contained. The price turn is real. The pricing power is not.

What changed was shipping and energy: the cost of moving, fuelling and feeding China’s industrial engine.

The chart shows why April matters. The black PPI line marks the official break, while the sentiment layer shows that pressure did not arrive out of nowhere. Language around energy, freight, metals and input costs had already tightened before PPI crossed zero.

Sentiment: Pressure Before the Print

Sentiment does not replace the print; it brings forward the question. Our inflation sentiment indicator had already picked up the shift months before PPI turned positive, with references to energy costs, freight, raw materials and pricing power clustering more forcefully through the second half of 2025.

In a cost shock, wording often moves before weighting. The print confirmed the break; sentiment had already traced the pressure forming beneath it.

Factory Gate: Reflation Without Repair

April’s PPI breakdown makes the imbalance clear. Oil and gas extraction rose 28.6% y-o-y, non-ferrous metal mining and dressing surged 38.9% y-o-y, and production-material prices rose 3.8% y-o-y. Consumer-goods producer prices, by contrast, were still -1.0% y-o-y. The pressure was upstream; the softness was still downstream.

The heat is not in the consumer basket. It is in the industrial furnace.

That is what makes this reflation uncomfortable. It lifts the headline but squeezes the producer: what firms pay is moving faster than what they can charge. Margins are where the shock is being stored.

Manufacturing: Firmer Sentiment, Uneven Output

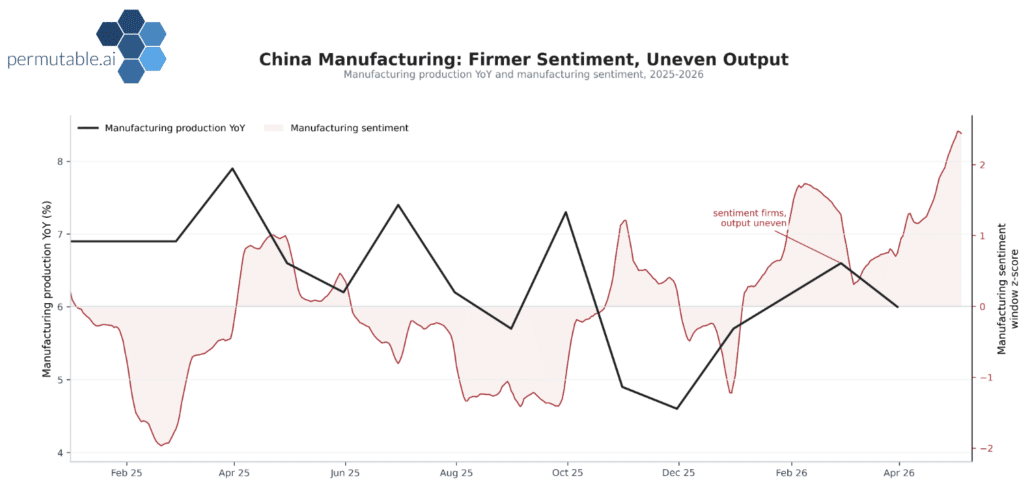

The manufacturing chart keeps the China inflation story honest. If April’s PPI break were a clean domestic reflation signal, hard activity would be confirming it more decisively. It is not.

Manufacturing sentiment has strengthened into 2026, suggesting the factory cycle is no longer dormant. But production remains uneven. The factory floor is moving, but not with enough force to turn upstream inflation into a demand story.

Trade, Shipping and Energy

April’s trade numbers look resilient on the surface. Exports rose 14.1% y-o-y, imports rose 25.3% y-o-y, and the trade surplus remained large at around $84.8bn. The headline says trade resilience. The cargo data says supply strain.

The energy data sharpen the point. Total crude imports over the first four months were still slightly higher y-o-y, so April’s weakness was not simply a China-demand story. It was route-sensitive. Customs data showed April crude cargoes at 38.47mn tonnes, around -20% y-o-y, while natural gas imports stood at 8.42mn tonnes, around -13% y-o-y.

Geopolitical risk becomes input-cost risk. The import data show the physical disruption. The PPI data show the price transmission. The Strait of Hormuz has moved from map risk to margin risk.

Policy: Easing Bias, Harder Optics

Beijing entered 2026 with a clear easing bias. Deflation, weak property, soft household demand and thin industrial margins all argued for lower financing costs. But stronger trade data and above-consensus inflation prints make aggressive near-term easing harder to justify.

The PBOC still has room to ease. It has less room to make that easing look costless. Inflation has not closed the door to easing. It has made the doorway narrower.

A deflation problem has become a margin problem. The data now pull in opposite directions: weak where policy wants strength, expensive where policy wants calm.

The Gulf is where the shock began. China is where it has become macro.

What to Watch

- PPI persistence: If energy, freight and raw-material costs fade, Beijing can look through April. If they hold, the producer-price turn becomes harder to dismiss.

- Pass-through into final prices: For now, the impulse is landing in margins, not household demand. Soft food and consumer-goods prices remain the key evidence point.

- PBOC communication: The easing bias remains, but April complicates the optics. The print is either a shock to look through or a constraint to manage.

Reading the Cycle Through Sentiment

Inflation sentiment does not replace CPI or PPI. It changes the timing of the question, showing where pressure is forming, whether it is broadening, and whether it is driven by domestic conviction or imported cost stress.

The inflation chart shows pressure building before the PPI break; the manufacturing chart shows why that break should not be mistaken for a clean industrial recovery. Together, they point to a more complicated China inflation picture: the economy is not simply reflating. It is absorbing an upstream cost shock while domestic demand and production momentum remain uneven.

For rates and FX, the question is whether imported inflation delays the easing path or merely complicates the communication around it. For commodities, the signal is whether China’s upstream cost pressure is broadening across energy, metals and freight before official price data catches up. For cross-asset allocators, the distinction matters: China is not just reflating; it is reflating in the wrong place.

For institutional access to our China Sentiment Indices and regional macro indicators, contact us at enquiries@permutable.ai