In this article, we examine why Germany’s macro stabilisation has not translated into market conviction, and what German political sentiment and German economic sentiment reveal about the disconnect. Inflation has cooled back towards target territory, delivering the first sub-2% print since late 2024. The European Central Bank has, for now, closed the tightening chapter. Bund yields have drifted back into a familiar range. On paper, it looks like normalisation.

Markets are not pricing it that way. Beneath the calmer prints sits an economy still stuck in low gear. The data says the shock has passed. The narrative, and the positioning, hum a different tune.

That gap between outcomes and sentiment is the story. Activity has not snapped back into a growth channel. Firms are still waiting, households remain cautious on spending, and rates markets oscillate between tentative calm and narrative-driven nerves. This is precisely the kind of environment where sentiment adds clarity the data alone cannot. When the data improves but conviction does not, you need a way to observe the macro pulse in real time.

This is where sentiment closes the gap. Tracking political tension, manufacturing and inflation together shows how narratives have moved in real time, often ahead of the data, over the past couple of years. Each sentiment indicator is drawn from news coverage and split into two lenses. The domestic lens is built from German-language and sources inside the country, capturing how stress is experienced, debated and implemented. The international lens reflects how Germany is framed from outside, through market-facing narratives and a global perspective. Read together, the two measures provide complementary information on how german economic sentiment and developments are interpreted domestically versus internationally, and how divergences between these perspectives influence market expectations.

Germany has moved from a sharp post-pandemic rebound into prolonged stagnation. The reopening bounce has long since faded and the economy has settled into a low-growth regime, with activity repeatedly failing to sustain momentum and output hovering around flat.

The inflation picture, by contrast, suggests the shock has largely run its course, with euro area price pressures being broadly contained, and underlying measures are easing, even if services remain the last pocket of stickiness. The direction is clear. The inflation problem has been defused.

Growth and lasting momentum are the missing pieces of the puzzle. Factory orders rose more than 5% m-o-m in November, but the series is often flattered by lumpy capital goods. Retail sales fell -0.6%, a cleaner read on domestic demand, and a reminder that disinflation has not yet translated into a willingness to spend. The macro backdrop is divided. There are pockets of resilience, but the economy is still behaving as if uncertainty is the binding constraint.

That mix helps explain why Bunds have crept up. Inflation is no longer the story, but growth, politics and policy credibility are. Sticky services and wages keep the ECB in wait-and-see mode, while markets have trimmed peak-rate expectations without pricing a clean easing cycle. The move back above 2.8% on the 10-year is better read as term premium and issuance risk being repriced into a weak-growth outlook, not as renewed inflation fear. Stabilisation is here, conviction has yet to arrive.

Into 2026, the base case is a modest pickup rather than a breakout. Forecasts cluster around 1.0-1.2% growth, supported by easier financial conditions, some fiscal impulse and a gradual export recovery. Even so, the uplift remains fragile, held back by high energy costs, political friction and cautious investment.

In a conventional cycle, cooling inflation and steadier activity should take the edge off uncertainty. The German story has not played along. The macro numbers suggest the landing is in sight, but markets are still asking for proof, not reassurance. That is where sentiment earns its keep, not as a replacement for the data, but as a live read on whether the transition is being believed.

Our Regional Macro Sentiment Indices are built from news flow and split by source geography. The domestic lens captures on-the-ground narratives: policy execution, coalition dynamics, labour and price pressures, and how households and firms are actually experiencing conditions. The international lens reflects the outside view, focusing on market implications, cross-country comparisons, and the moments when Germany is reframed as a broader European risk.

Germany’s coverage is overwhelmingly domestic, more than 80% of volume generated inside the country. That matters. It means the baseline signal is formed internally, while international narratives tend to act as accelerants rather than foundations, flaring around symbolic risk moments and market-relevant events. Put simply, domestic sentiment shows where stress is building. International sentiment shows when it starts to become a global factor.

This is where sentiment becomes genuinely useful for macro and quant teams. German political sentiment quantifies the slow build-up of governance strain, tracking shifts in fiscal credibility, institutional friction, protests, and domestic fragmentation in real time. German economic sentiment captures the macro pulse through household and business confidence. Together, they provide a sharper real-time read on the economic conditions through the narrative and framing, showing where momentum is building and often moving ahead of lagging releases, especially when credibility and follow-through are driving the cycle.

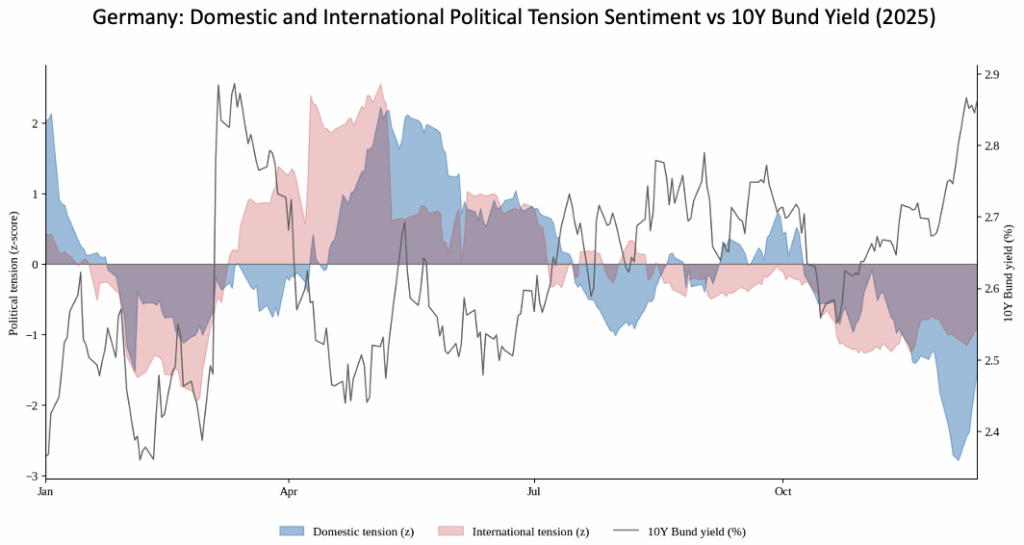

The political tension chart for 2025 suggests Germany is not in imminent crisis, but stuck in slow-motion stress, and markets are pricing that. As political tension sentiment turns more negative, Bund yields tend to rise because the market reads it as higher uncertainty around fiscal delivery, political friction and policy follow-through. That lifts the term premium and perceived risk rather than flight to safety.

Domestic tension builds steadily because German-language and domestic coverage tracks the accumulation of constraints and stress that make governing harder. Budget rewrites, debt brake friction, coalition misalignment, protests, and the rising pull of parties on both the right and the left all contribute to a more fragmented political sphere. International tension moves in sharper, event-led bursts around moments that travel to global investors: elections, polling, defence spending credibility, and doubts over whether Europe’s anchor economy can execute the shift from fiscal restraint to policy credibility.

In this regime, Bunds no longer function as a pure haven asset. When fiscal frameworks are contested and budgetary trajectories remain uncertain, investors price a higher term premium to hold German duration through periods of governance ambiguity. That dynamic has intensified as structural increases in infrastructure and defence outlays expand supply beyond levels markets absorbed comfortably in the previous decade.

Late 2025 marks an inflection point. Domestic political sentiment deteriorated steadily as narratives around coalition friction, policy execution risk and institutional strain gained traction in German-language and source coverage. That shift has transmitted directly into Bund pricing, the 10year yield rose as investors demanded additional compensation for elevated uncertainty around fiscal credibility and political cohesion. The correlation between sentiment deterioration and yield widening has tightened, reflecting markets’ reassessment of governance risk as a pricing variable rather than a tail event.

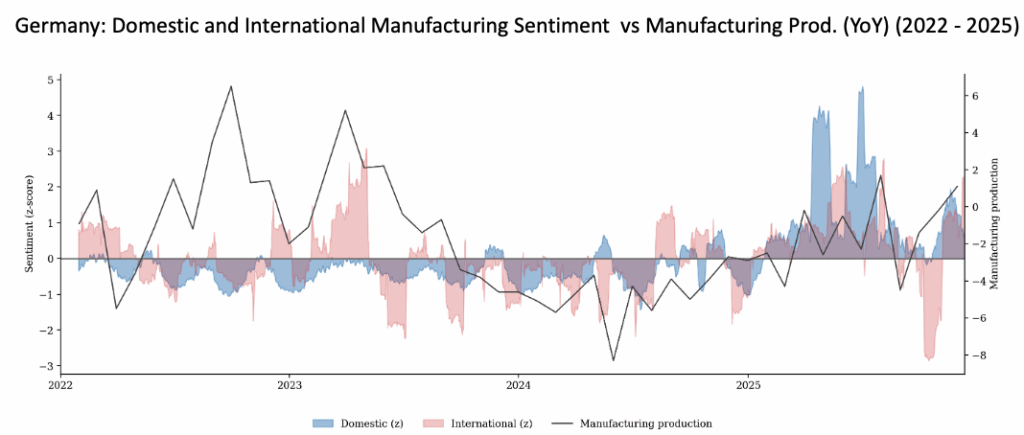

The manufacturing chart shows why Germany’s industrial slowdown has not been priced as a clean cycle. Domestic manufacturing sentiment deteriorates early in 2022 and stays there through much of 2023, tracking a narrative anchored in margin pressure, weak external demand and delayed investment. Even as supply chains ease and policy support arrives, the domestic tone does not confirm a lasting turn which helps explain why output struggles to regain momentum.

International manufacturing sentiment is more reactive and event-led. It lifts on global trade optimism or Germany-as-bellwether framing, then fades when production fails to deliver follow-through. The red series swings more sharply around the data, reflecting how quickly the outside narrative shifts when the recovery does not validate itself in hard numbers.

By 2025, the relationship moves closer to alignment. Domestic sentiment shows stronger positive bursts that coincide with, and at times slightly lead, the improvement in manufacturing production. International sentiment improves too, but less convincingly and its pullbacks line up with pauses in output momentum. The chart is not a month-to-month forecasting tool. It is a regime read. It helps explain why downturns persist, why recoveries hesitate, and why the eventual upturn is gradual rather than decisive.

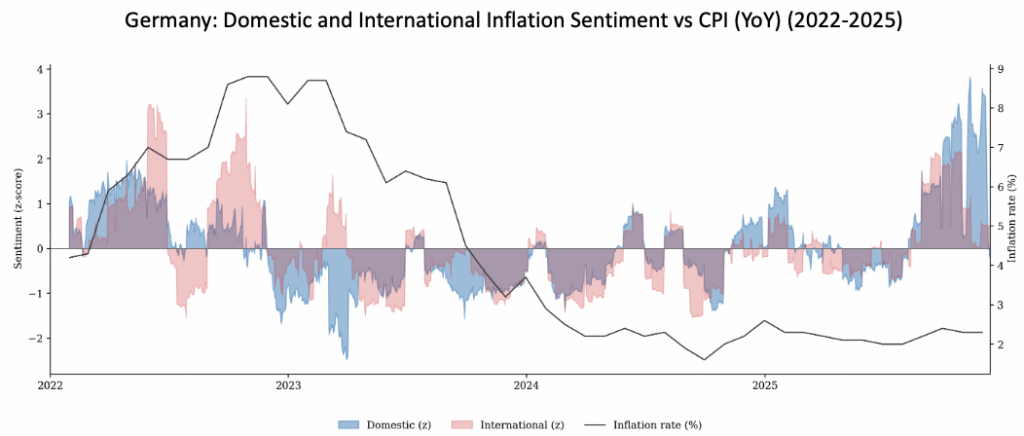

Inflation sentiment demonstrates how perception can diverge from measured data. Domestic inflation expectations rose sharply in early 2022 as households and firms experienced direct cost pressures. The lived experience of inflation, observed through utility bills, grocery expenses, housing costs, and routine purchases, shapes sentiment more immediately than official statistical releases, which typically arrive with a lag and may not capture full picture at surface level. Inflation sentiment peaked and rolled over ahead of realised inflation, highlighting how quickly lived pressure can turn before it appears in official releases. As the cost shock faded, domestic narratives eased, while international sentiment remained more sensitive to policy signalling and market implications.

Even as inflation returns towards target, sentiment volatility persists. That reflects lingering sensitivity around affordability rather than renewed upside inflation risk.

By 2024-25, inflation returned to the target range, yet sentiment remained elevated, likely reflecting relief that disinflation had occurred rather than expectations of renewed price pressures. While inflationary pressure has moderated, public perception remains sensitive to recent memory. This helps explain why relatively modest economic developments or policy discussions continue to influence expectations, even as headline CPI appears tamed.

Collectively, the three charts illustrate that Germany no longer presents an inflation headache for the ECB, though a convincing growth narrative has yet to emerge. Inflation has returned to target levels. Manufacturing activity remains suppressed by persistent structural headwinds. Political uncertainty continues to weigh on fiscal, business and consumer confidence.

Domestic sentiment tends to anchor baseline expectations, while international attention intensifies when Germany’s challenges are perceived to pose broader systemic risks.

In that setting, sentiment reinforces what the data alone cannot. It explains why improved prints have not been enough to change behaviour. The numbers have steadied, but the market pulse has not. Confidence is still conditional, investment remains on pause, and even modest shocks can move pricing because the recovery has not yet won belief.

This configuration is not unprecedented. Germany faced a similar pattern in 2014-2016: inflation normalised, growth remained weak, and sentiment stayed fragile. That episode resolved only when the ECB took the proper measures and external demand revived through Chinese stimulus. Neither catalyst appears to be coming to the rescue. The ECB has less room to ease and global demand remains subdued. That makes the domestic policy response, fiscal capacity, execution speed, political cohesion, more critical than in prior cycles.

Two developments would prove to shift the trajectory of the current outlook.

Until one of these shifts materialises, the regime remains fragile and economic environment is likely to stay constrained.

Hard data indicates Germany’s current position, while sentiment measures reflect how economic transitions are interpreted, debated, and incorporated into expectations. In manufacturing, sentiment captures signs of adjustment fatigue even when output recovery remains absent. In inflation, it demonstrates that price pressures have cooled substantially, though confidence in the sustainability of disinflation continues to be evaluated. In political tension, it captures the difference between episodic external concern and the steady accumulation of domestic strain that shapes expectations over time.

This is why sentiment becomes powerful at precisely this stage of the cycle. Improved macroeconomic indicators do not mechanically translate into behavioural change. Such shifts occur when expectations cease deteriorating and begin to consolidate around a more stable outlook.

To learn more about our Regional Macro Sentiment Indices and how they can support your strategy, contact enquiries@permutable.ai

Analysis

06 Aug 2026

Spotting macro regime shifts early: lessons from Japan, Turkey and Brazil

Read more >

Analysis

04 Aug 2026

Global industrial production sentiment: Canada, India and South Korea Gain as the UK, Germany and China weaken

Read more >

Analysis

30 Jul 2026

US growth and policy outlook Q2 2026: Q2 bought the Fed time. July may take it back

Read more >