This article uses Permutable AI’s oil analytics to examine the narratives currently driving Brent crude during the Middle East crisis. By analysing real-time sentiment across geopolitics, supply disruptions and macro signals, it shows how geopolitical risk is shaping oil markets. The piece is aimed at energy traders, market analysts, macro investors and institutions seeking data-driven insight into oil price movements.

Brent crude has moved from a relatively stable trading range in February into a high volatility geopolitical regime in March. Prices opened the period near $68.9 and gradually established a new floor near $71 before accelerating sharply in early March. Within days Brent surged through the low $90s and briefly spiked to $107.67 on 8 March before correcting rapidly to $93.81 by 10 March.

For traders and analysts, moves of this magnitude are rarely explained by supply and demand fundamentals alone. During geopolitical crises, oil markets are increasingly shaped by narratives around security risks, supply disruptions and policy responses.

This is where AI-driven oil analytics become essential. At Permutable, we analyse large volumes of global news coverage extracting topic level sentiment signals making it possible to quantify which narratives are driving price behaviour in real time.

Using our Brent Crude Topic Sentiment Indices – part or newly released Asset Sentiment Indices, our in house market analysis team examined how sentiment around key oil market drivers evolved during the escalation.

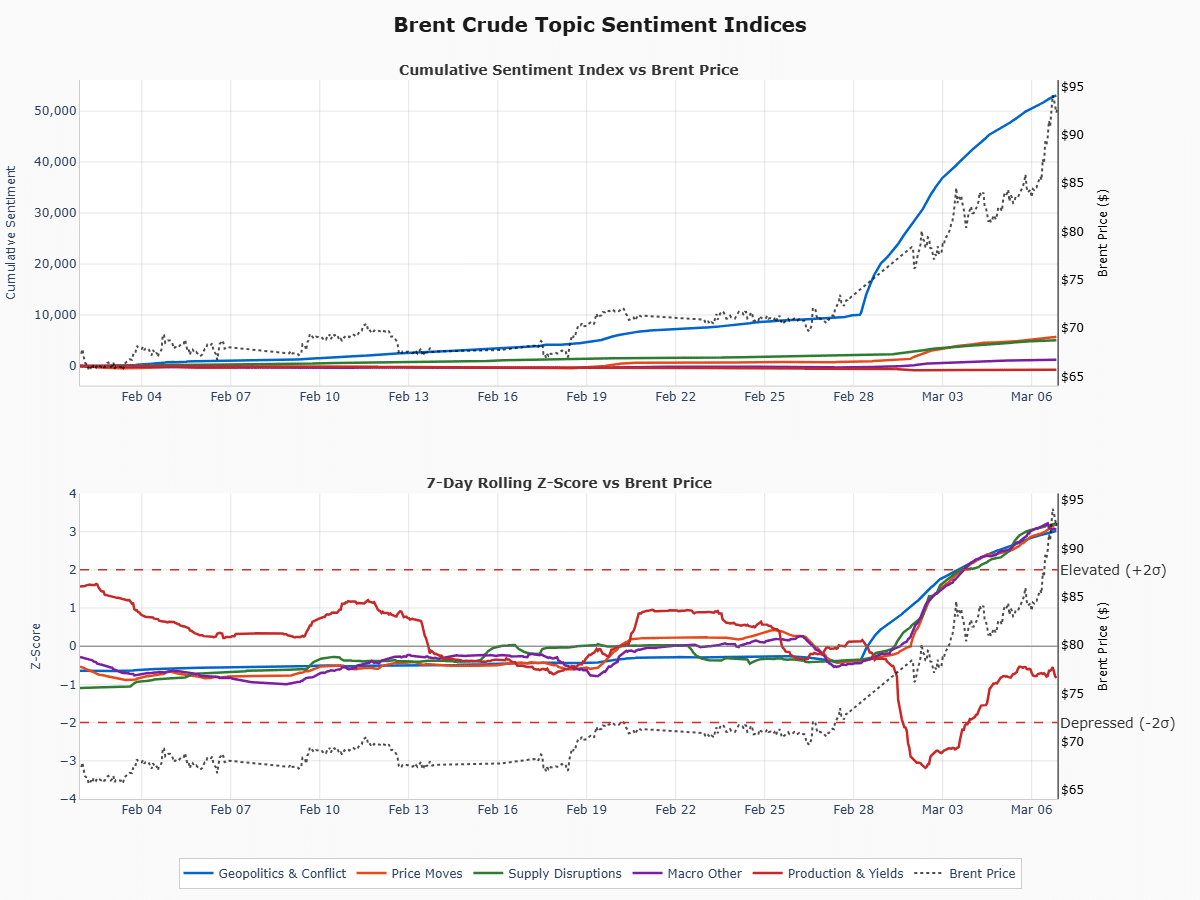

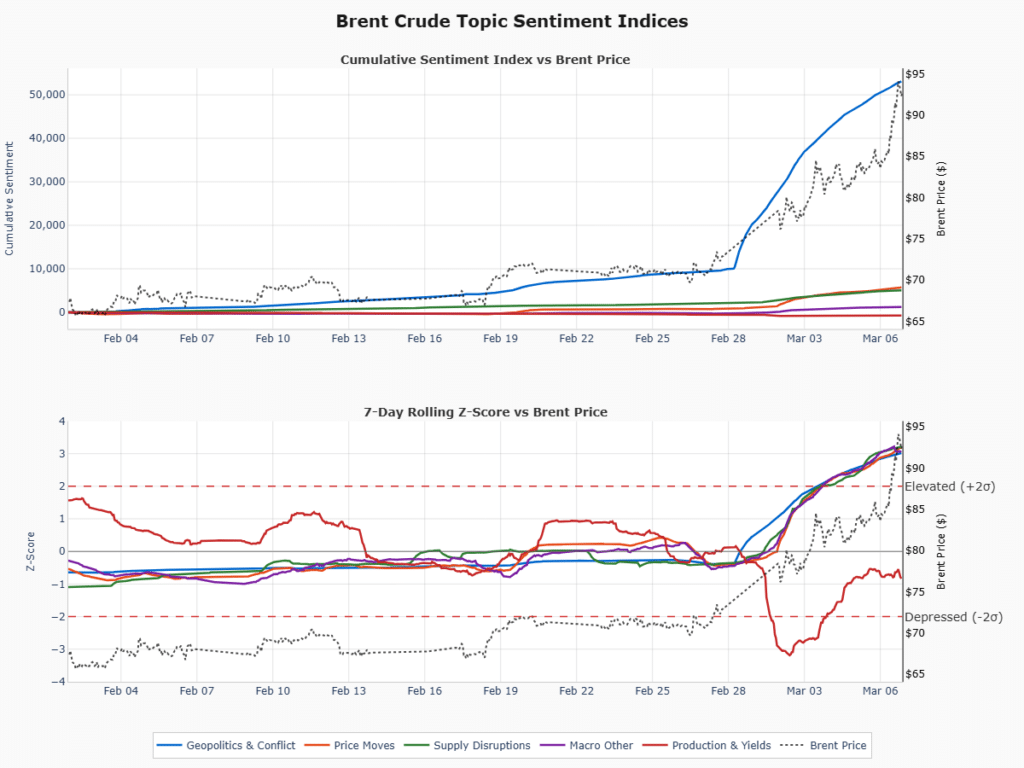

Above: Oil analytics – Sentiment signals behind Brent’s recent rally. Topic sentiment indices derived from global news coverage show a sharp surge in geopolitical risk narratives alongside rising supply disruption sentiment, coinciding with Brent crude climbing toward \$95 during the current Middle East crisis.

Table of Contents

ToggleIdentifying market drivers

The chart accompanying this analysis visualises how different news driven narratives influenced Brent crude during the crisis.

The top panel shows cumulative sentiment by topic alongside the Brent price. This reveals how narratives build over time and how they relate to price movements.

The lower panel shows a 7 day rolling Z score. This measures how unusually strong coverage of a given topic is relative to its recent baseline. When the Z score rises above roughly +2 or +3 standard deviations, it indicates a surge in attention that is statistically significant compared with normal levels of coverage.

The dotted black line represents the Brent crude price. Together these signals allow analysts to distinguish between background news flow and narrative shifts that are capable of moving markets.

During the recent crisis several key drivers became visible through our sentiment signals.

Geopolitics and conflict become the dominant driver

The strongest signal came from geopolitical sentiment, which began rising sharply from 28 February onward. This surge coincided closely with Brent’s breakout from the $70s toward the $90s. The rise in geopolitical sentiment reflected a wave of reporting around Gulf security risks, attacks on energy infrastructure and growing concerns around regional escalation.

When geopolitical sentiment reaches these levels the oil market often begins pricing in a risk premium. Traders respond to the possibility that supply flows could be disrupted even if actual production losses remain uncertain. In this case the increase in geopolitical risk coverage coincided with a rapid repricing of energy security risk across oil markets.

Supply disruption narratives reinforce the rally

Alongside the geopolitical escalation, our sentiment indicators showed a sustained rise in supply disruption narratives. Coverage linked to disruption risk increased steadily through late February and early March, with a rising Z score indicating a meaningful shift in the intensity of news coverage around potential supply interruptions.

Reports driving this shift included attacks on oil depots and refining infrastructure, shipping disruptions affecting tanker routes and maritime security incidents affecting energy transit corridors. There were also reports of export disruptions and production losses among Gulf producers, including interruptions affecting Iraqi output.

Even when physical disruptions are limited, the perception of supply risk can drive significant price reactions. This dynamic was visible in the early March rally, as traders moved to secure supply and hedge against the possibility of tightening near term balances.

Production narratives briefly push in the opposite direction

Our sentiment signals also captured a sharp negative shift in production related sentiment around 1 and 2 March. Coverage referencing production increases, spare capacity discussions and potential supply responses pushed the production sentiment Z score, representing an unusually strong shift in tone compared with its normal baseline.

In a calmer market environment this type of signal could place downward pressure on oil prices. However the production narrative was quickly overshadowed by the surge in geopolitical and disruption related coverage. The episode illustrates how crisis environments can temporarily shift market focus away from traditional supply demand signals and toward geopolitical risk.

Macro narratives and price momentum signals

Our sentiment indicators also detected a gradual rise in macro related narratives during the period. Coverage referencing economic growth expectations, inflation dynamics and global energy demand slowly increased. These narratives were not the primary catalyst for the rally but they provided supportive background sentiment.

At the same time price momentum coverage intensified as Brent rallied through the $80s and into the $90s. Financial media increasingly focused on the price move itself and on tightening energy markets. Importantly, momentum narratives tend to follow price movements rather than initiate them. However they can reinforce existing market trends by amplifying the sense that a structural shift in pricing is underway.

Crisis pricing and the March 8 spike

The most extreme move occurred on 8 March when Brent surged to $107.67. Our sentiment indicators during this period show an intense clustering of geopolitical and supply disruption narratives.

Reports described direct strikes on energy infrastructure, refinery damage and production losses among several Gulf producers. These developments briefly pushed the market into full crisis pricing mode as traders rushed to hedge against sustained supply outages.

Policy signals trigger a rapid unwind

The rally reversed sharply on 9 March when Brent fell to $92.54. This decline of roughly 14 percent in a single session reflected a sudden shift in narrative signals. Our senitment indicators show that the reversal coincided with a wave of diplomatic and policy related developments. These included discussions around potential strategic reserve releases and signals of coordinated responses among major economies.

Such signals reduced the perceived probability of a prolonged supply shock. Traders rapidly unwound positions and the geopolitical risk premium contracted just as quickly as it had formed. By 10 March Brent stabilised around $93.81 as markets attempted to balance ongoing regional risk with the possibility of policy intervention.

Current state of play

At time of writing, our crude oil sentiment indicators point to the fact the market remains in a highly reactive geopolitical regime. Gulf security risks and shipping disruptions continue to support an underlying geopolitical premium in prices. At the same time diplomatic engagement and the potential use of strategic reserves introduce a counterweight that may limit extreme price spikes. This combination explains the unusually high volatility observed between early March and the present.

How narrative-driven oil analytics provides edge during geopolitical crises

During geopolitical crises traditional oil market indicators often lag the speed at which information reaches financial markets. Inventory data, production reports and official statistics are typically released with delays, while energy markets respond immediately to emerging developments across geopolitics, security and policy.

This is where modern AI-driven oil analytics of the kind we provide here at Permutable prove their value. Rather than relying solely on lagging physical market indicators, our intelligence layer analyses large volumes of global news, policy signals and macro developments to detect shifts in market narratives as they occur.

Our approach to oil analytics focuses on transforming unstructured global information into structured market intelligence. By applying natural language processing and topic level sentiment modelling to thousands of daily news signals, the platform identifies which themes are gaining momentum across the global information landscape and how those themes relate to commodity price movements.

In the current Middle East crisis our analytics reveal how Brent’s volatility has been driven by a combination of escalating geopolitical risk, intensifying supply disruption narratives and rapid shifts in policy expectations. Tracking these narrative dynamics provides traders and analysts with an early view of when the market is beginning to price in new risks or unwind existing ones.

This type of insight allows the clients we work with to better navigate market volatility by helping them to identify the drivers shaping commodity price behaviour before those dynamics are fully reflected in traditional market indicators.