In this article we examine the interplay between UK inflation dynamics, policy credibility, and the long end of the gilt curve. Inflation has become the fault line for UK markets, with the long end of the yield curve now serving as the clearest test of policy credibility. The 30-year gilt has emerged as the market’s barometer of confidence in fiscal prudence and the Bank of England’s policy stance, with shifts in inflation sentiment increasingly offering an advance signal of repricing.

Table of Contents

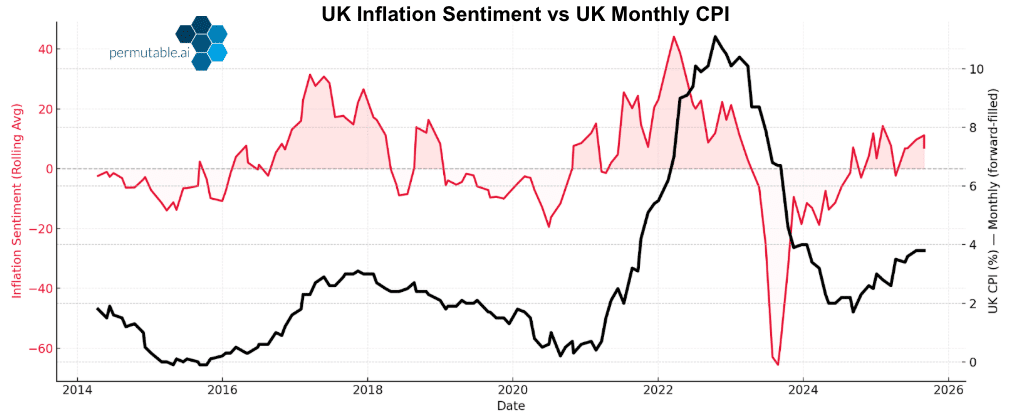

ToggleUnravelling the Market Narratives Driving UK Inflation

Markets no longer move solely on the data itself, they respond to the narratives that frame them. By tracking the market’s heartbeat through our macro indices, we measure both conviction, using the tone and intensity of commentary; but also the degree of coverage, capturing the breadth of circulation across the market discourse.

A clear example of this is evident in the recent movements in UK inflation sentiment, which began to pivot upwards ahead of July’s CPI release, a precursor signal to the subsequent upside surprise. As the print exceeded expectations, the move was swiftly transmitted into the long end, with gilt yields repricing higher. In this sequence, market sentiment did not merely echo events, it provided an early read on the market’s unease as the stir around policy credibility and risk premia built up.

From UK Inflation to Policy Credibility

The July CPI print at 3.8% y-o-y (up from 3.6% in June), the highest since January 2024. Transport costs spurred much of the price spike, with the release coming mere weeks after the BoE cut rates to 4% in a finely balanced 5-4 decision by the MPC. While CPI has eased from its 2022–23 highs, UK inflation sentiment has begun to turn positive again in 2025, indicating that the market is bracing for renewed inflationary pressure.

In this setting, the contrast is clear. Inflation is once again surprising to the upside, yet the policy path is already unwinding. For markets, that combination has all the characteristics of a credibility dilemma – the BoE appears to be loosening its stance just as price pressures re-emerge.

These factors are difficult to ignore, where investors had hoped for consistency, they now see policy drifting out of line. Such dissonance has unsettled market sentiment, reviving familiar questions surrounding the Bank’s stance, whether it is prepared to lean against inflation risks or whether political / growth concerns are taking precedence. As a result, the yield curve itself has become the register of doubt, with the long end bearing the imprint of a market that is no longer convinced the policy will deliver the discipline needed to anchor expectations.

Yield Stress at the Long End

The UK has broken away from its peers, standing out as the outlier in the G7. While lingering UK inflation pressures explain part of the move, the greater weight falls on a structural credibility gap that has pushed UK yields to the top of the pack. The cracks in policy credibility are widening, leaving a gap increasingly filled by risk premia and uncertainty.

Nowhere is this more visible than at the long end of the curve, where 30-year gilts trade above 5.6%, compared with 4.9% in the U.S., 4.2% in France, 3.3% in Germany and 3.2% in Japan. While peers face the same global pressures, their long ends remain anchored, the UK stands alone, having broken away as gilts carry the heaviest premium amongst the advanced economies.

For investors, the repricing goes well beyond the latest inflation surprise – it is a broader verdict on the UK’s policy stance. What is being priced is not just inflation itself but the persistence of a risk premia, the extra yield investors now demand for holding UK debt amid doubts about credibility. That shows up as a rise in the term premia, with markets requiring greater compensation to commit capital to long-dated gilts in the face of uncertainty over fiscal sustainability and the Bank of England’s reaction function.

This structural steepening at the long end leads to higher borrowing costs for the state, crowding out for corporates, and reduced relative value appeal of gilts in foreign portfolios. In other words, the long end has become the clearest register of that unease, with each rise in yield reflecting the extra premium demanded to hold UK debt in the face of eroding credibility and the growing shadow of fiscal drift. The message is clear, credibility lost becomes costly to reclaim, and nowhere is that more plainly written than in the long-end of the yield curve.

The Long-Term Implications

A prolonged period of long-end stress carries broader risks.

- Debt servicing costs rise for both government and corporates.

- Financial conditions tighten, curbing credit availability.

- Asset valuations weaken in sectors most sensitive to gilt yields.

With gilts at elevated levels, and underlying concerns simmering, the chain of causality is becoming clearer, UK inflation surprises erode policy credibility, long-end yields climb, and systemic risk edges higher.

Gaining the Edge

Market sentiment offers the early signal. It reveals how UK inflation narratives turn into credibility tests, and how those tests are priced into the gilt curve. Spotting this sequence early ahead of the curve transforms hindsight into foresight. That is the edge – connecting fundamentals with the market’s own heartbeat, and identifying stress before it breaks into the open.

At Permutable, we specialise in decoding these shifts in real time. Our macro sentiment indices capture the turning points in narrative and market essence before they appear in the broader consensus.

If you’d like to explore how are data can give your team a forward-looking edge, get in touch with us at enquiries@permutable.ai

Read our latest Permutable Perspective monthly publication here and sign up to our weekly Permutable Insights newsletter here.

FAQs

Q1: What does the UK Inflation Sentiment Index measure?

It captures the tone and intensity of financial media narratives around UK inflation, quantifying whether sentiment is becoming more hawkish, dovish, or credibility-focused.

Q2: How does this data act as a leading indicator?

Shifts in sentiment often appear before CPI releases or BoE moves. For example, in July 2025, inflation sentiment rose ahead of the CPI print, providing an early warning of gilt repricing.

Q3: Why focus on the long end of the gilt curve?

The 30-year gilt is now the market’s clearest register of policy credibility. Rising yields signal not only inflation expectations but also the risk premia investors demand to hold UK debt.

Q4: How can institutions use this dataset?

Risk managers, macro funds, and strategists can integrate the sentiment index into models to anticipate stress, guide hedging decisions, and refine allocation in fixed income.

Q5: What makes UK inflation sentiment unique in 2025?

Unlike peers, the UK faces a structural credibility gap. Even when inflation sentiment softens, yields remain elevated, showing markets are pricing persistent doubts in fiscal and monetary discipline.