This global macro sentiment briefing analyses easing US inflation and subdued UK growth entering 2026. Using Permutable AI’s real-time sentiment indices, it highlights how inflation expectations and domestic growth narratives are evolving before official data confirms them. Designed for institutional investors, macro strategists and systematic trading desks, it provides forward-looking cycle insight.

This week’s edition of Permutable AI’s Weekly Market Signals focuses on a developing inflection in global macro sentiment across the United States and the United Kingdom. By tracking rolling domestic and international narrative momentum, we examine how US inflation dynamics are evolving and why UK growth remains constrained as 2026 begins.

Our Regional Macro Sentiment Indices measure global macro sentiment in real time, capturing persistence rather than reacting to daily noise. The purpose is straightforward: identify the shift before it appears in official data. When global macro sentiment turns and sustains, hard economic prints typically follow with a lag.

At present, global macro sentiment points to continued moderation in US inflation, while signalling that UK growth remains in low gear.

Table of Contents

ToggleUSA: Global Macro Sentiment Continues to Lead CPI

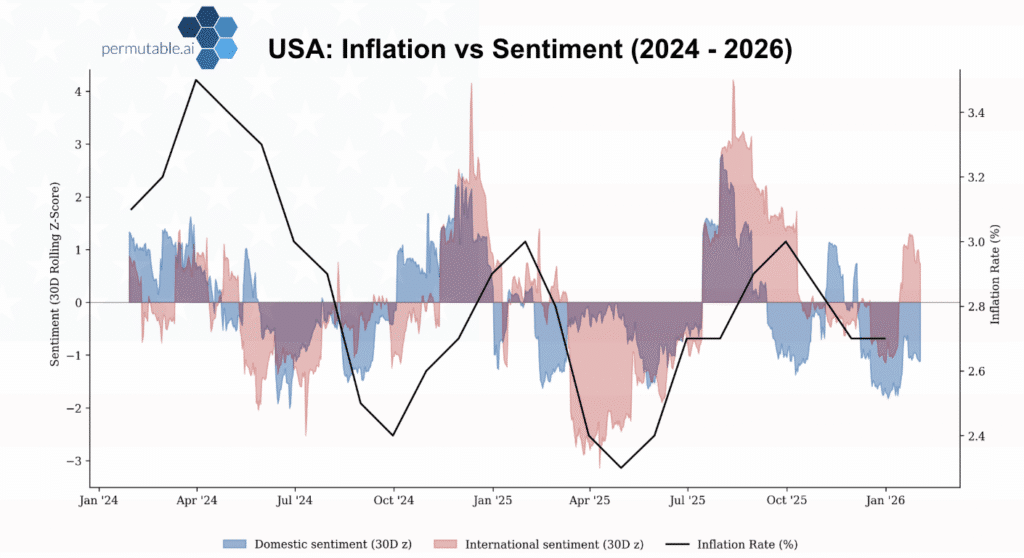

Inflation in the United States continues to ease, and global macro sentiment led that moderation. Rolling inflation sentiment softened well before CPI confirmed the slowdown, reflecting fading pricing pressure narratives across domestic reporting and international commentary.

Disinflation remains the base case within global macro sentiment signals. However, the pace of easing is slowing as monetary tightening continues to work through the system. Inflation sentiment has moderated, but it has not collapsed. The distribution of narratives suggests price pressures are cooling gradually rather than reversing abruptly.

The next phase of the cycle is likely to be shaped less by the next CPI print and more by inflation expectations embedded within global macro sentiment. If inflation tone begins to firm consistently across domestic and international lenses, that often marks the early stage of rate repricing before official data shifts materially.

For now, the balance of risks within global macro sentiment still favours easing pressures. But markets should watch closely for any sustained change in tone.

Above: US global macro sentiment led the moderation in inflation through 2024 and again signalled renewed firmness during mid-2025 before CPI stabilised. Domestic and international inflation sentiment shifts tend to precede turning points in the official rate. As 2026 begins, sentiment suggests easing pressures remain intact but expectations are becoming more sensitive.

UK: Global Macro Sentiment Signals Low-Gear Growth

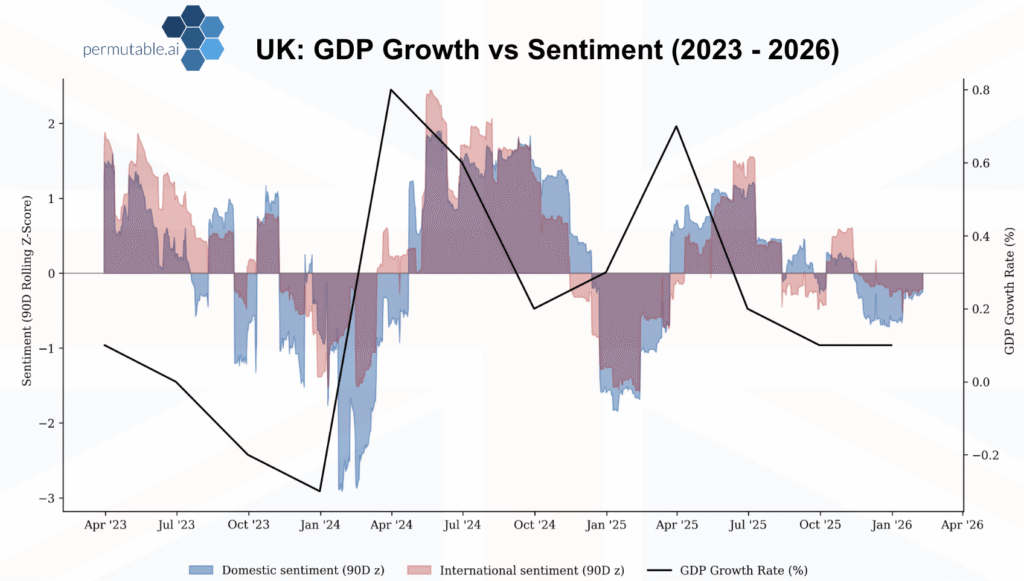

In the United Kingdom, GDP confirmed what global macro sentiment had already indicated. The 0.1% Q4 print formalised a slowdown that domestic growth narratives began reflecting in late 2025.

Rolling UK growth sentiment remains constrained entering Q1 2026. While not signalling outright contraction, global macro sentiment reflects an economy lacking acceleration. Domestic demand, hiring tone and investment narratives remain subdued.

Importantly, international narratives are not providing meaningful offset. In previous cycles, external demand or global tailwinds helped cushion domestic weakness. At present, global macro sentiment shows limited evidence of that dynamic, leaving domestic demand as the primary swing factor.

The edge lies in reading the live 2026 cycle through global macro sentiment while the hard data continues to catch up. If domestic growth tone stabilises and converges with international sentiment, modest lift may follow. If fragmentation persists, low-gear expansion remains the dominant regime.

Above: UK global macro sentiment rolled over ahead of each major slowdown in GDP growth, particularly in late-2023 and late-2025. Domestic sentiment moves earlier and more sharply than international tone, signalling shifts in underlying growth momentum before official data confirms the change. Entering 2026, sentiment remains subdued, consistent with a low-gear expansion rather than recovery.

How institutional teams use global macro sentiment

Institutional investors and macro desks use our global macro sentiment to detect narrative acceleration before markets reprice. By measuring persistence across domestic and international layers, they gain insight into whether a theme is transient or structural.

Global macro sentiment signals are deployed to:

Monitor inflation expectations before rate repricing

Detect shifts in growth momentum

Identify regime transitions across regions

Filter noise driven by short-lived headline flow

Because the data is structured and machine-readable, global macro sentiment integrates directly into systematic strategies and discretionary macro workflows alike.

See global macro sentiment in action

Our global macro sentiment indices stream live momentum and regime indicators across inflation, growth and policy dynamics. For institutions seeking a forward-looking macro lens, global macro sentiment provides an early read on cycle shifts before traditional indicators confirm them, request a personalised walkthrough below.