This bearish backdrop or market sentiment mirrors the current macro landscape. Q3 GDP contracted -1.8% annualised, the first decline in six quarters, pressured by weaker exports, subdued consumption and a sharp housing correction. At the same time, sentiment tied to China relations, travel flows and trade disruptions turned sharply negative after Beijing’s travel advisory and the sell-off in tourism-linked equities. Together, the data and news sentiment profile show a yen under pressure from both domestic fragility and external risk premia, with investors adopting a distinctly defensive stance.

GDP Breakdown: Temporary Weakness Meets Structural Friction

The Q3 figures confirm the loss of momentum across key components. External demand pulled -0.2% from GDP as exports fell -1.2% q-o-q, reversing the tariff-distorted frontloading in auto shipments. Domestic demand provided only modest support. Consumption remains constrained by a persistent cost-of-living squeeze and sticky food inflation, while residential investment dropped -32.5% annualised, the sharpest drag on the quarter.

Business investment rose 1% q-o-q, offering the only sign of resilience. Yet indicators around capex and hiring have cooled, pointing to increasing caution in Q4 and heading into 2026. Overall, the domestic base is flagging at a moment when Japan is increasingly exposed to external headwinds, a combination that leaves the yen sensitive to swings in global risk appetite.

Tourism and Tech Shock: The External Hit

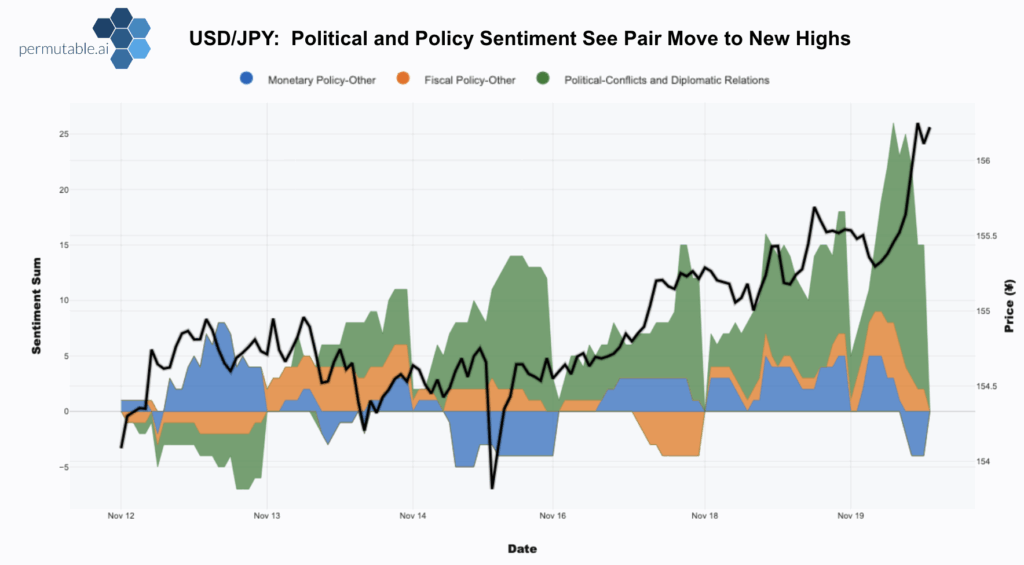

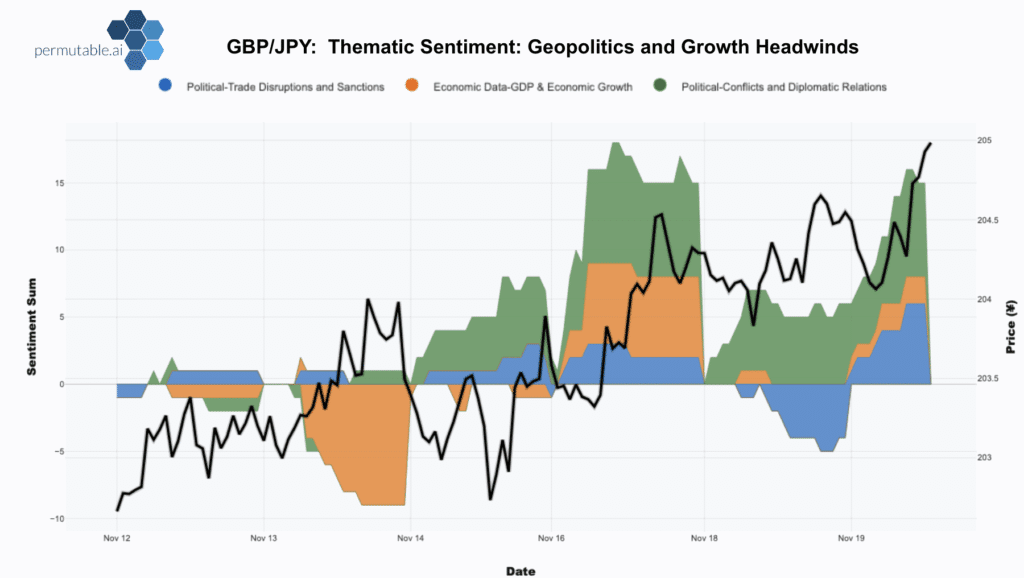

The more acute pressure originates abroad. China’s travel advisory and the deterioration of relations have hit tourism, retail and other consumer-facing sectors hard. Close to 80% of Chinese bookings to Japan have been cancelled, and major Chinese airlines have moved to refund tickets in response to the escalation. The result has been a broad sell-off in Japanese tourism and retail names, with market unease clearly on display as firms such as Shiseido and Isetan slid -10% to -12%. At the same time, the sentiment surrounding political and trade-related themes turned decisively bearish, reinforcing the impression that investors see this as a lasting drag rather than a passing diplomatic flare-up.

Chinese visitors to Japan account for about a quarter of inbound arrivals and close to ¥600bn in quarterly spending. If flows remain depressed, the economic hit could equate to 0.3% to 0.4% of annual GDP. Japan’s semiconductor and tech supply chains also sit near the fault lines of the broader US-China strategic environment, amplifying the external risk. This deterioration across China-linked sectors has become a central driver of the yen outlook.

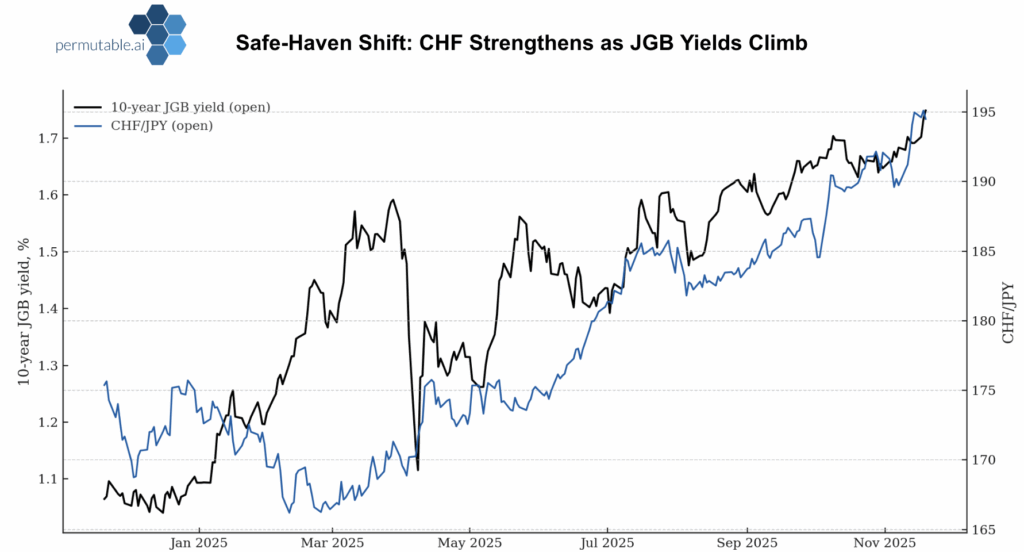

The Policy Backdrop: Domestic Fragility and External Risk Premiums

The yen remains constrained by the overlap of weak domestic demand, external shocks and rising fiscal concerns. The GDP setback reinforces expectations that the BoJ will normalise policy slowly. Tourism weakness and softer equity sentiment weigh on Japan’s external balance, while long-end JGB yields are rising for supply-driven reasons rather than stronger growth. Japan’s Finance Minister Satsuki Katayama has been clear that growth comes first and that the forthcoming stimulus will do the lifting, but offered no hint on its size, a line the bond market reads as more supply with few constraints and a heavier overhang at the long end.

With public debt above 200% of GDP and a ¥17tn-plus stimulus plan under discussion, concerns around fiscal sustainability have resurfaced. Uncertainty around fiscal stability, China exposure and policy clarity has softened in parallel. In turn, the yen continues to trade more on risk premia than on classical rate differentials.

Going forward policy communication now sits at the heart of the currency’s trajectory. Soft Q3 data and worsening inflation outlook strengthen the case for additional fiscal measures, but markets remain cautious about the heavier issuance profile that follows. Governor Ueda has stressed vigilance over FX and policy moves, yet the BoJ’s comment of a measured, data-dependent approach limits immediate influence over currency stabilisation.

A firmer alignment between fiscal and monetary policy or a more supportive external environment would help improve the yen outlook. Until then, rallies are likely to fade and sentiment will continue to guide short-term moves.

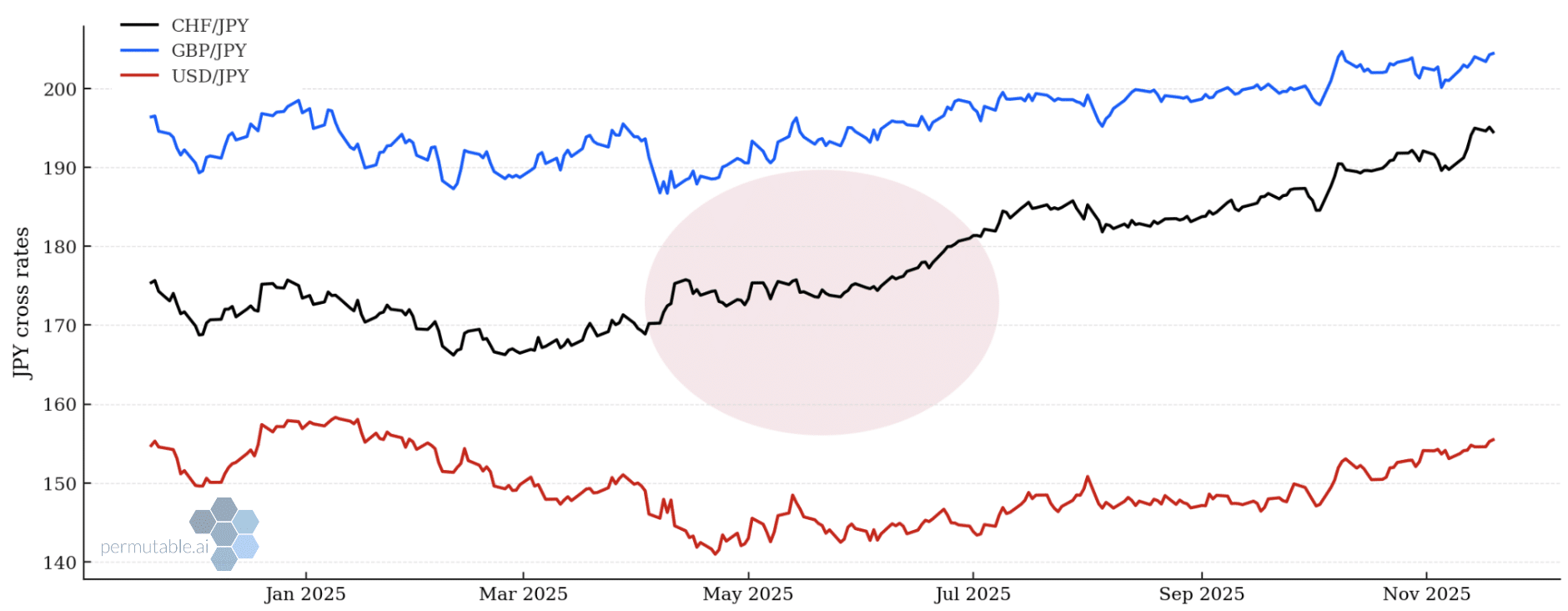

Japan’s growth setback may prove partly temporary, but the added pressure from China leaves the yen exposed in the near term. A Q4 rebound is possible if travel flows stabilise and exports gain traction, but USD/JPY and GBP/JPY remain upward-biased for now.

USD/JPY