How to turn news sentiment into strategy: A guide for institutional investors

14 Nov 2025

14 Nov 2025

This is a comprehensive guide for institutional investors, quants, and macro strategists on applying news sentiment to trading, risk management, and regime detection, with examples taken from Permutable AI’s market sentiment data.

We’re often asked how to apply our market sentiment insights in practice, how to turn the behavioural layer of markets into measurable, actionable intelligence. This guide brings together our best practices, use cases, and live results to show how news sentiment in trading can be harnessed across asset classes.

Markets move on perception before they move on data. Whether it is fear, optimism, or conviction, each leaves a measurable trace. The challenge has been turning those traces into something institutions can trust and use. That is where market sentiment adds edge: it quantifies the market narrative and converts it into a tradable, target-aware signal that leads the data and sharpens price discovery.

Our market sentiment intelligence does precisely that. We capture global financial, geopolitical, and policy news in real time, measure tone across millions of headlines, and translate the flow into structured, time-stamped data. The outcome is a continuous read of market perception, supported by more than ten years of history, providing a behavioural pulse that complements fundamentals and price action. Every observation is version controlled, time stamped, and traceable to source for full transparency and auditability.

Delivered via our Trading Co-Pilot and alert system, or directly through an API, our signals give economists, portfolio managers, and quants a faster view of shifting narratives and a practical way to turn that insight into strategy. In a world where policy rhetoric, supply shocks, and geopolitical risk shape expectations ahead of official releases, market sentiment supplies the missing layer of context. It shows not only what has happened, but what the market believes is happening, and belief often moves first.

The two charts below illustrate how this works in practice across both an asset and macro level. At the asset level, gold’s monetary-policy sentiment series captures how shifts in central-bank communication, liquidity expectations and policy risk premia accumulate into market positioning long before those dynamics are visible in price alone. At the macro level, Japan’s inflation sentiment provides a high-frequency reading of narrative pressure around prices and wages, often anticipating inflection points in core CPI.

Taken together, they show how sentiment functions as a real-time gauge of market interpretation, revealing investors are processing news flow, giving clients an earlier and more nuanced read on evolving regimes.

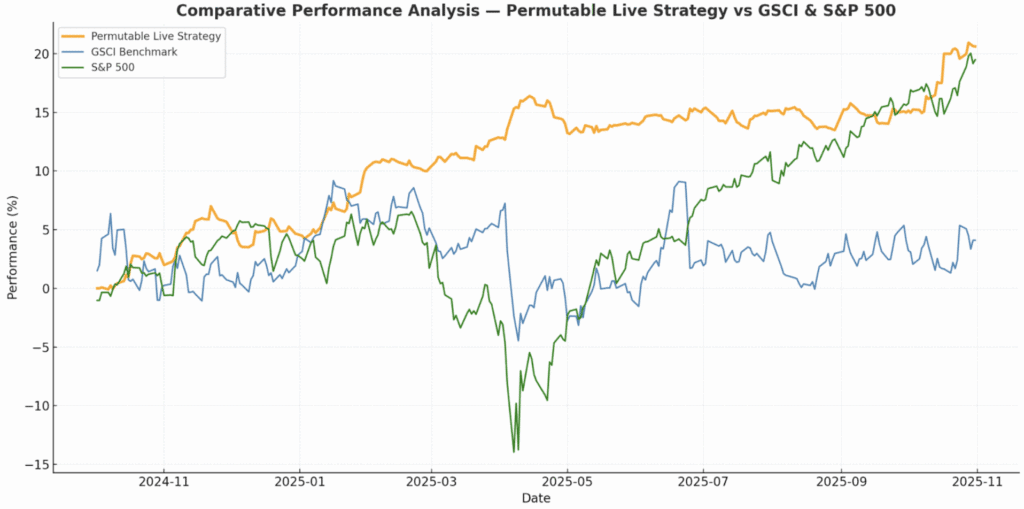

At Permutable, we don’t just provide market sentiment intelligence, we trade on it ourselves. For the past twelve months, we’ve run a fully audited systematic commodity strategy driven entirely by our sentiment signals. This wasn’t a backtest or simulation. It was real capital, real markets, and real risk.

Our systematic strategy runs a balanced long-short structure across six liquid front-month contracts in energy, agriculture, and precious metals, distributing risk evenly across sectors. Every position is driven by sentiment signals.

Because it proves sentiment-driven trading isn’t theoretical. When market narratives shift, whether due to sanctions, weather, or policy changes, our signals capture those shifts early and translate them into disciplined, profitable positions. The track record validates what we offer: intelligence that consistently outperforms the market.

In October 2024, our strategy generated a 13.6% return on Brent and 21.8% on natural gas by capturing narrative shifts before they appeared in pricing. When fresh sanctions on Russian producers shifted the risk position from production to logistics, longer routes, compliance costs, vessel uncertainty, our sentiment layers detected trade tensions and shipping disruption in the news flow early, initiating long exposure ahead of the rebound while earlier shorts cushioned drawdowns.

Similarly, when winter demand risk, record US exports, and volatile weather converged to flip natural gas sentiment sharply bullish, the model closed shorts ahead of the rally, held through the surge, then trimmed as momentum faded, preserving profits through disciplined regime adaptation. This is market sentiment in action, identifying not just what is moving, but why, and positioning accordingly before the rest of the market has a chance to catch up.

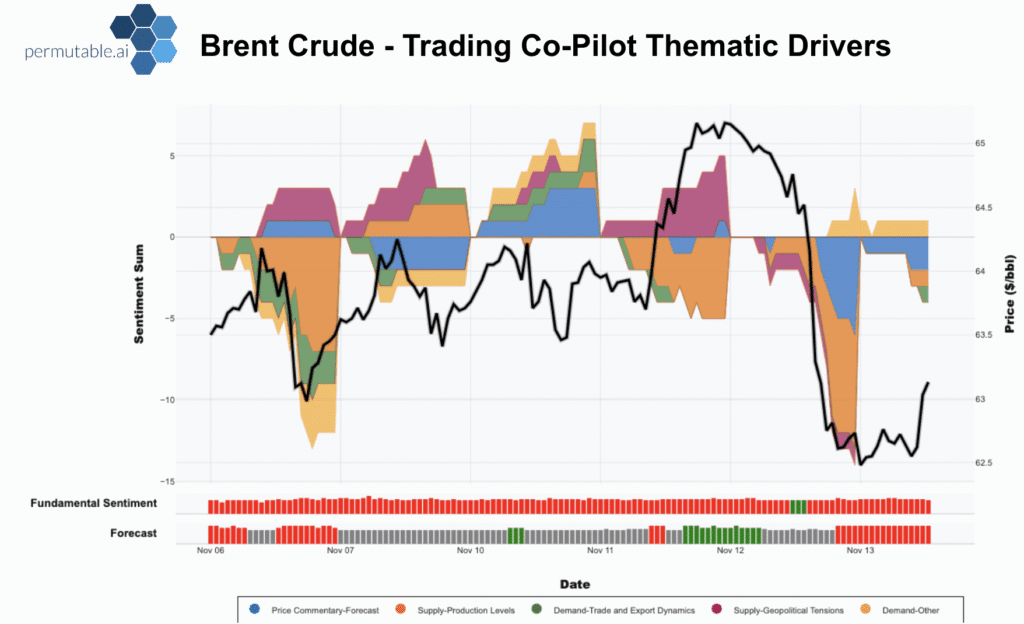

Traditional economics measures outcomes. Market sentiment measures perception. Each headline carries a measurable tone, expressed as a score between +1 and -1. We apply news sentiment analysis across more than 50 traded assets spanning energy, metals, agriculture, FX, crypto and equities. Each headline is scored and fed into 2,580 asset-level indices, refreshed with upwards of 500,000 new stories each day.

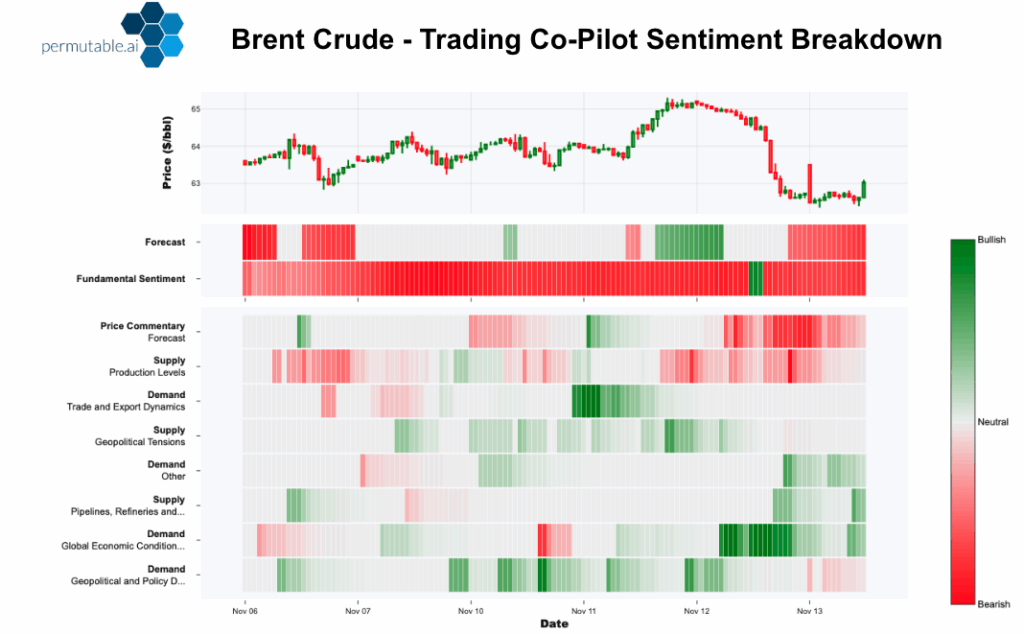

This turns the market narrative into structured, high-frequency signals that behave like traditional market indicators yet respond immediately to changes in news flow. In the Brent chart below, those same signals are decomposed into supply, demand, trade and geopolitical themes to show which narratives are driving prices.

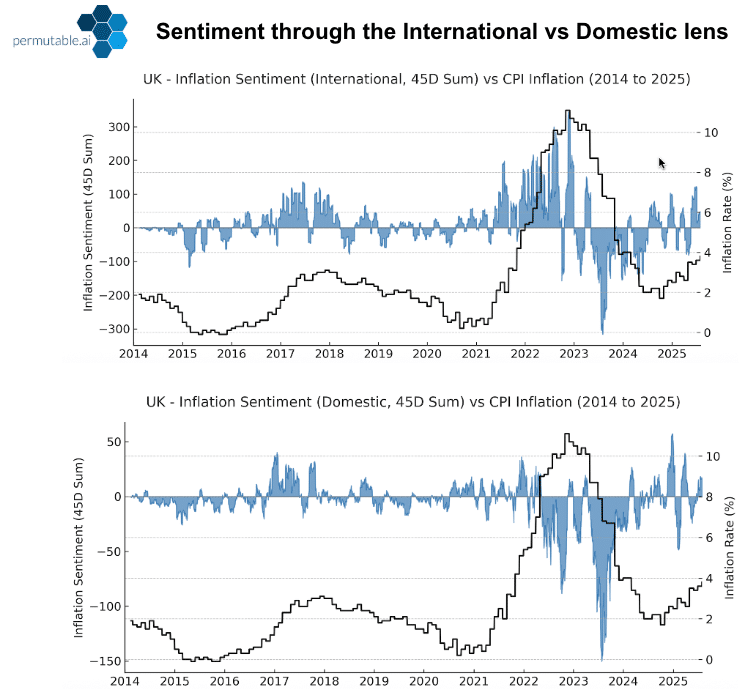

At the macro level we take the same approach, aggregating local-language news from global sources into 2,640 regional macro indices with more than a decade of history across over 30 regions. For each topic we split news sentiment into international and domestic lenses, separating how the story is told on the ground from how it is framed globally.

The chart below compares UK inflation sentiment from these two angles, international headlines and domestic news, against CPI, showing how global and local narratives can diverge or move together before the official data. Applied at scale, these indices behave like familiar economic time series but move at the speed of real-time news, flagging shifts in growth, inflation, labour markets, policy and political risk ahead of releases.

Unlike surveys, which are periodic, lagging and prone to response bias, market sentiment indices update continuously with the flow of information, providing an immediate map of collective perception. Structured into indices, these readings become early indicators of how economies and assets are evolving, and where pressure is building or fading.

The raw signal captures tone, rolling averages smooth short-term noise, z-scores can help place narratives today in historical context, and topic-level breakdowns show where attention is clustering, whether around inflation, labour markets, political tension, energy supply or policy risk, across both assets and macro.

Market sentiment does not replace traditional data, it refines it. It turns narrative into measurable evidence and connects perception with reality.

For systematic investors and quantitative teams, market sentiment is a live signal rather than a concept. Each score is a numerical input, time-stamped, replicable, and ready for testing, converting unstructured information into tradable behavioural factors.

Tuned market sentiment windows identify when optimism or pressure is building and how persistent that move is. Within systematic strategies, market sentiment plays three clear roles:

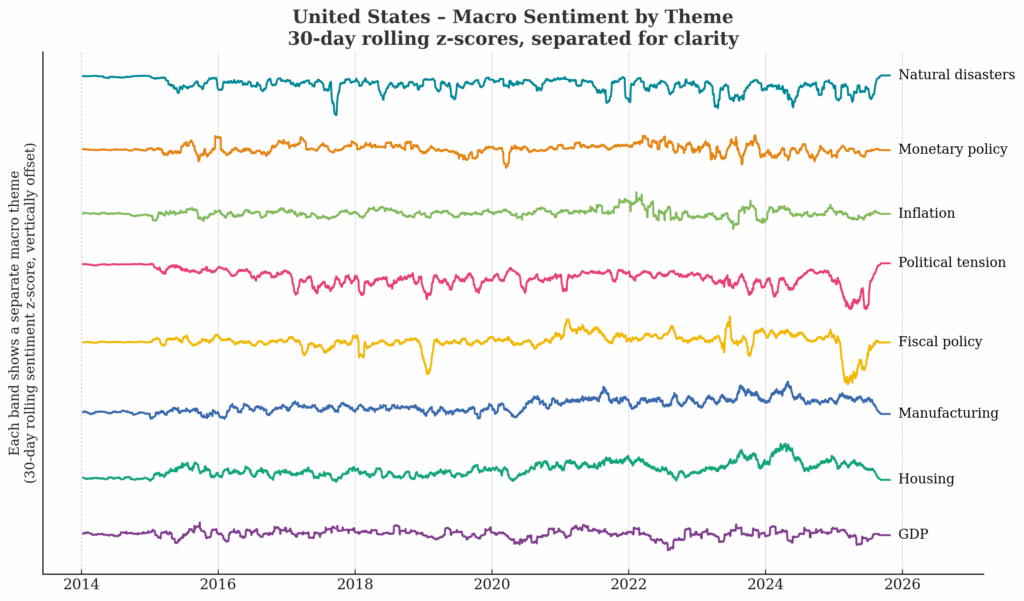

This chart tracks Permutable’s US macro sentiment indices, normalised and smoothed over 30 days so you can see the underlying regimes across growth, housing, manufacturing, policy and politics without getting lost in day-to-day noise.

Looking at the themes side by side lets a systematic user spot persistent patterns and turning points, then test them properly: which narratives tend to move first, which ones line up with future returns, spreads or macro surprises, and which are mostly noise. From there you can group themes into cleaner factors, build “policy pressure” or “growth risk” baskets, and drop weaker signals, giving you a more stable feature set and a better chance of keeping performance out of sample.

This framework extends naturally across energy, metals, and agriculture. By embedding market sentiment feeds into systematic workflows, traders capture not only what has moved but why, improving conviction, responsiveness, and drawdown control.

Our own trading strategy demonstrates this in practice: a 2.85 Sharpe ratio over twelve months shows what’s possible when sentiment signals are integrated systematically.

Markets are narratives in motion. Quantifying them requires objectivity, scale, and continuous monitoring.

Our framework translates headlines and policy commentary into structured evidence of how investors interpret change. When positive or negative market sentiment dominates coverage, liquidity adjusts and risk premia shifts. As news sentiment builds in one direction, positioning often changes before fundamentals do. These behavioural transitions, visible in tone, emphasis, and persistence, underpin market sentiment’s reflexive power.

Tracking how narratives cluster and evolve allows our indices to surface early signals of where attention, confidence, and stress are shifting, the same forces that drive asset repricing.

Track evolving narratives around supply, demand, regulation, and weather. Shifts in policy or disruption tone appear first in market sentiment data, often preceding volatility or curve steepening across oil, gas, metals, and agriculture. Our October Brent performance, capturing the sanctions-to-logistics narrative shift, illustrates this edge in practice.

Use market sentiment as a high-frequency complement to conventional indicators. Changes in tone around growth, inflation, and policy frequently precede data releases or surveys, sharpening scenario analysis and turning-point detection.

Treat market sentiment as a behavioural factor that can be tested directly within trend, carry, or volatility models, enriching alpha generation and regime classification. Our live 2.85 Sharpe demonstrates this isn’t theory, it’s repeatable performance.

Monitor divergences in growth, policy and news sentiment between economies. When tone splits meaningfully across regions, it can highlight curve misalignments or FX asymmetries before markets adjust.

Identify where stress is building and where complacency persists. Real-time news sentiment provides early signals of overheating or uncertainty, adding a behavioural lens to leverage, liquidity, and hedge calibration.

Our Trading Co-Pilot turns sentiment data into clear visual intelligence on market conditions. It highlights the headlines shaping each sentiment regime, maps bullish or bearish shifts across categories like supply, demand, and policy, and aligns these directly with asset-price behaviour.

From the bullish rotation in Brent to volatility spikes in metals or FX turbulence ahead of policy meetings, each chart combines sentiment and price action to provide an immediate, explainable view of the forces driving regime change.

For quant, systematic, and data-sourcing teams, the API delivers the same intelligence at scale: structured, transparent, and ready to integrate into dashboards, quantitative models, or automated trading systems.

The edge now lies not in spotting the fundamentals first, but in understanding how the market already feels about them, and news sentiment makes that visible.

At Permutable AI, we convert global news and policy narratives into real-time, explainable signals that strengthen timing, conviction, and risk control across asset classes. For economists, portfolio managers, and quants, our Trading Co-Pilot and API provide a structured bridge between perception and performance. Market sentiment becomes a live input to strategy, continuously testing house views against the information set and signalling where narratives are shifting before prices move.

Here, it is important to note that news sentiment does not replace expertise, it amplifies it. It gives investment teams a systematic read on market psychology, transforming perception into foresight and narrative into alpha.

We don’t just sell these signals. We trade them ourselves. And over the past twelve months, we’ve demonstrated they work: 20.6% returns, 2.85 Sharpe, and 4.4% maximum drawdown in live markets.

Reach out to our team at enquiries@permutable.ai to see how our real-time news sentiment intelligence can enhance your decision-making across markets, assets and strategies.

Analysis

30 Jul 2026

US growth and policy outlook Q2 2026: Q2 bought the Fed time. July may take it back

Read more >

Analysis

29 Jul 2026

South Korea economy: the chip windfall is outrunning domestic growth

Read more >

27 Jul 2026

The tide turns on Russia inflation outlook as drone strikes spread from refineries to warehouses

Read more >