In today’s financial landscape, economic growth forecasting requires more than analysing lagging data releases. Traditional models built on historical datasets often confirm trends after markets have already repriced. For institutional investors and macro desks, the challenge is identifying shifts before they appear in official GDP or CPI prints. This is where global macro sentiment becomes central to modern economic growth forecasting.

At Permutable AI, our Global Macro Sentiment Indices offer a forward-looking layer that captures real-time narrative shifts across economies, sectors and policy regimes. Rather than waiting for quarterly data, they measure how expectations, confidence and economic tone are evolving on the ground. For investors focused on economic growth forecasting, this provides an earlier read on momentum, regime shifts and potential inflection points.

We apply advanced natural language processing (NLP) and machine learning to convert millions of multilingual news articles, policy reports and market narratives into structured macro signals. These signals enhance economic growth forecasting by integrating qualitative shifts in sentiment with quantitative economic models.

Understanding Permutable AI’s Advanced Sentiment Indices

Our Global Macro Sentiment Indices are powered by a real-time intelligence architecture designed to support economic growth forecasting across developed and emerging markets.

The platform ingests millions of inputs daily and aggregates them into structured sentiment scores across inflation, growth, labour markets, investment and policy. These scores form rolling indices that track persistence and direction of narrative shifts, filtering noise while identifying meaningful regime changes.

A defining feature is transparency. Every sentiment score is source-traceable, allowing users to drill into the underlying narratives driving the signal. For institutions engaged in economic growth forecasting, this explainability strengthens compliance, governance and model validation processes.

Additionally, our hybrid multi-LLM infrastructure ensures rapid processing and continuous updates. This reduces latency and ensures economic growth forecasting models incorporate live macro developments rather than static historical snapshots.

Real-Time Data Intelligence and Economic Growth Forecasting

Real-time intelligence fundamentally reshapes economic growth forecasting. Traditional models rely heavily on scheduled releases – CPI, GDP, employment – all of which arrive with delay and revisions.

Global macro sentiment bridges this gap by measuring expectation shifts as they build. When sentiment changes direction and sustains, economic growth forecasting models gain early evidence of an emerging shift in trajectory.

For example:

-

A sustained improvement in inflation sentiment may precede moderation in CPI.

-

A rollover in domestic growth narratives can signal weakening GDP momentum before quarterly data confirms it.

By embedding our sentiment indices into forecasting frameworks, institutional investors improve responsiveness and reduce model blind spots.

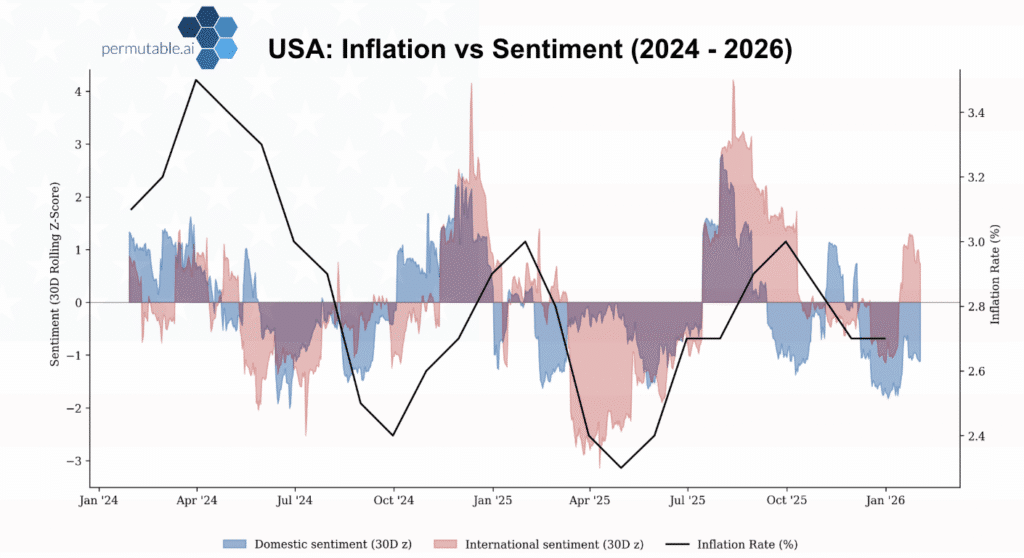

Case Study: US Inflation and Sentiment-Led Forecasting

US inflation dynamics illustrate how global macro sentiment strengthens economic growth forecasting.

Inflation is driven not only by realised price data but also by expectations, policy framing and confidence. During recent disinflation phases, sentiment indices signalled moderation before CPI data confirmed the slowdown.

Positive sentiment around easing supply constraints and moderating policy pressure indicated reduced inflation persistence. Conversely, when inflation sentiment began firming in isolated pockets, it flagged potential risks to the smooth disinflation path.

For economic growth forecasting models, this provides a leading indicator of rate expectations, yield curve shifts and macro repricing risk.