This article analyses industrial metals industry trends using Permutable AI’s sentiment intelligence, highlighting how supply risk, policy costs, China-led narratives and volatility are reshaping global metals markets in 2026. It is aimed at executives, analysts, strategists and procurement leaders seeking data-driven insight into market dynamics beyond traditional supply-demand models.

Industrial metals markets are entering 2026 with a familiar but intensified pattern: broadly constructive pricing, frequent volatility, and rapid re-pricing driven by headlines rather than slow-moving fundamentals. Using our sentiment intelligence across lead, aluminium, iron ore, steel, copper and tin, this article outlines the industrial metals industry trends shaping global markets – and what they reveal about risk, opportunity and market structure across sectors.

The core insight from our recent industrial metals sentiment signals is clear. Price direction alone is no longer the most important variable. Instead, how quickly markets react to new information – and how fast sentiment flips from risk-on to risk-off – defines current industrial metals industry trends.

A market shaped by risk narratives, not smooth cycles

One of the defining industrial metals industry trends is the dominance of event-driven pricing. Across nearly every major metal, sentiment has been repeatedly influenced by clustered disruption narratives: operational suspensions, permit reviews, export restrictions, weather impacts, logistics breakdowns and geopolitical escalation. These events do not need to permanently alter supply to move markets. The risk that supply could be disrupted is often enough to trigger aggressive buying, short covering and technical breakouts.

What follows is just as important. Once the immediate headline impulse fades, markets often shift rapidly into profit-taking and consolidation. This pattern – fast repricing, followed by retracement – has become structural. It reflects a market environment where market participants are highly sensitive to downside risk and reluctant to carry large unhedged exposure.

From a sentiment perspective, this tells us that volatility is not an anomaly within current industrial metals industry trends. It is the operating condition.

China’s role as a sentiment accelerator

Another recurring feature across iron ore, aluminium, copper and tin is the outsized influence of China-related narratives. Even when underlying demand indicators are mixed, sentiment often turns sharply more bullish when headlines reference stimulus, restocking, supportive policy signals or stronger onshore futures performance.

This does not always reflect immediate physical demand. Instead, it reflects expectation formation. Market participants price in future consumption, tighter balances or improved liquidity conditions long before those changes are visible in trade data.

Within current industrial metals industry trends, China functions less as a single demand centre and more as a sentiment transmission mechanism. Moves in Chinese futures or policy commentary can quickly ripple through global benchmarks, reinforcing rallies or stabilising pullbacks across the entire complex.

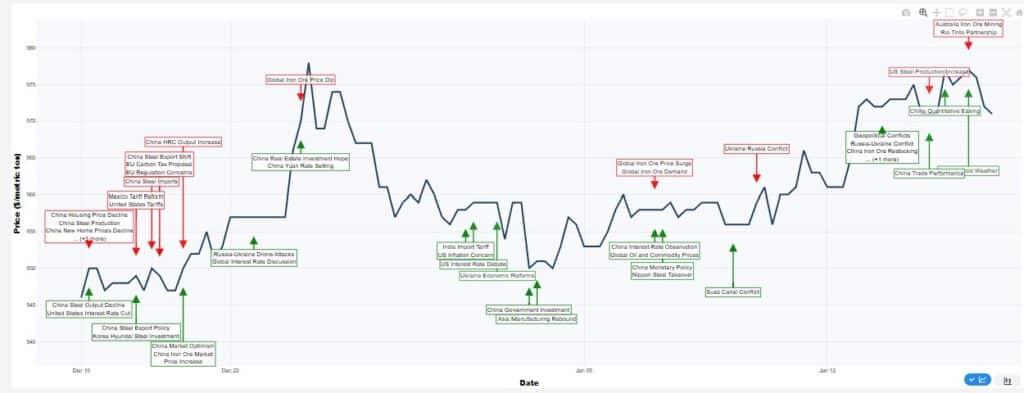

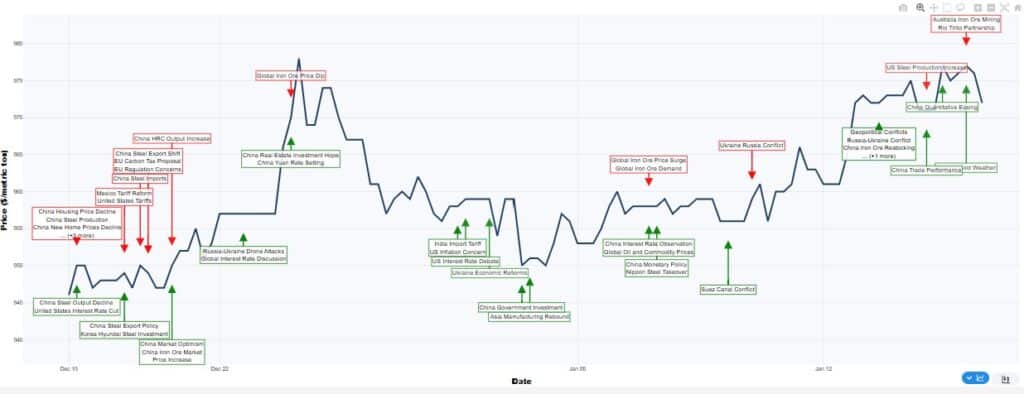

Steel and iron ore: cost floors and structural friction

Steel-related sentiment highlights the growing complexity of industrial metals pricing. While demand signals remain mixed, prices have been repeatedly supported by upstream input costs, regulatory uncertainty and energy dynamics. Iron ore sentiment has remained relatively balanced, but persistent restocking narratives and episodic supply risk have helped maintain a price floor.

A key industrial metals industry trends insight here is the decoupling between demand softness and price collapse. Even when end-market indicators weaken, structural cost pressures – energy pricing, emissions costs, logistics constraints and trade policy – can prevent rapid downside adjustment.

This suggests that industrial metals markets are increasingly cost-anchored rather than demand-led. For market participants, this changes how downside risk should be assessed: falling consumption does not automatically translate into falling prices if supply economics remain constrained.

Aluminium: policy premia meet supply uncertainty

Aluminium sentiment over the past month has reflected a persistent tension between near-term tightness and longer-term capacity expansion. Outages, geopolitical risk and compliance-related costs have repeatedly pushed sentiment higher, while announcements of rising output and regional demand softness have capped momentum.

This balance is emblematic of current industrial metals industry trends. Markets are simultaneously pricing scarcity risk and future abundance. The result is narrow but elevated trading ranges, with sharp intraday moves driven by news flow rather than structural rebalancing.

Importantly, aluminium highlights how policy and energy considerations are now embedded in metals pricing. Compliance costs, carbon frameworks and power market volatility are no longer peripheral – they are active sentiment drivers that influence how supply risk is perceived.

Copper: structural tightness and the scarcity narrative

Copper sentiment has increasingly coalesced around a structural tightness theme. Mine disruptions, labour actions, low visible inventories and constrained physical flows have reinforced a scarcity narrative that repeatedly attracts buying interest. While macro uncertainty and rate sensitivity still generate corrections, these pullbacks tend to be shallow when supply concerns remain unresolved.

Among current industrial metals industry trends, copper stands out as the clearest example of how long-term structural stories coexist with short-term volatility. Sentiment oscillates, but the underlying narrative of constrained supply and strategic importance remains intact.

This dynamic is instructive beyond copper itself. It shows how markets can tolerate near-term demand uncertainty when longer-term supply risk is perceived as credible and persistent.

Lead and tin: volatility at different scales

Lead and tin illustrate how industrial metals industry trends play out across both mature and niche markets.

Lead sentiment has been driven by supply disruption narratives and cross-metal momentum, while also carrying forward-looking concerns about potential oversupply from new projects. This creates a market that is constructive in the short term but cautious in its medium-term outlook – another example of sentiment balancing immediate risk against future supply responses.

Tin, by contrast, has been dominated by extreme volatility. Regulatory enforcement risk, permit uncertainty and sharp moves in Asian futures markets have repeatedly driven outsized price swings. While tin represents a smaller volume market, its behaviour underscores a broader industrial metals industry trends lesson: thin liquidity plus policy uncertainty equals amplified moves.

What these industrial metals industry trends reveal about market structure

Taken together, the sentiment signals across metals point to three structural characteristics shaping global markets:

Headline sensitivity is high. Markets react quickly to new information, even when the fundamental impact is uncertain.

Positioning matters more than conviction. Short covering, fund flows and futures dynamics amplify moves in both directions.

Policy and cost frameworks are structural drivers. Energy, carbon and trade regulation are now core components of price discovery.

These industrial metals industry trends suggest a shift away from slow, inventory-driven cycles toward a more reflexive market, where perception of risk often moves faster than physical balances.

Looking ahead: managing uncertainty, not predicting direction

The most important insight from Permutable AI’s sentiment intelligence is not a single price forecast. It is the recognition that volatility itself is the signal. Industrial metals industry trends in 2026 are defined by rapid sentiment shifts, layered risk premia and the constant interaction between supply narratives, policy frameworks and global macro signals.

For market participants across sectors, success will depend less on calling tops or bottoms, and more on understanding why markets move when they do—and how quickly sentiment can change. In a world where industrial metals industry trends are shaped by risk perception as much as reality, intelligence and adaptability have become the most valuable inputs of all.