In this article, we examine how a wave of geopolitical developments has reshaped the landscape across global energy markets. From renewed pressure on Russian energy to the unveiling of a US-EU energy pact, the past week has marked a decisive shift in the drivers of oil and gas prices.

Against this backdrop, our Trading Co-Pilot identified a build-up of bullish momentum signals across Brent, WTI, and TTF. These signals emerged alongside regime shifts, where accelerating sentiment and converging macro risks pushed markets into a new phase of price action. What we see is a market increasingly driven by political risk, regulation, and diplomatic shifts, rather than by supply-demand fundamentals alone.

Our Trading Co-Pilot surfaces a series of high-conviction entry points, each aligned with shifts in sentiment and structural market changes. These signals anticipated sharp rallies across all three benchmarks, revealing how pricing dynamics have evolved in response to rising policy pressure. We break down the political, structural, and market forces behind the moves and assess the themes likely to define the path forward for energy markets.

Table of Contents

ToggleBrent Crude: Geopolitical Risk Offsets Increased Supply

Brent futures rose to $72.70, touching a five-week high, as sanctions risk eclipsed optimism around OPEC+ output increases. While the markets showed signs of stabilisation, the growing uncertainty around Russian-linked barrels spurred the swift price ascent.

Sanctions Over Supply: A New Risk Premium Forms

Recent policy rhetoric revived the possibility of further sanctions targeting those involved in the transport and financing of Russian energy. Even in the absence of formal enforcement, the stern message alone introduced a reputational risk premium, increasing legal and financial exposure across energy markets.

Geopolitical Drivers: A Sharp Escalation in Policy Risk

In just a few days, the U.S. administration issued a series of high-impact policy threats:

- A 10-day ultimatum for Russia to come up with a ceasefire plan to end its invasion of Ukraine, paired with a warning of 100% secondary tariffs on Russian oil.

-

New export tariffs aimed at India and China, increasing pressure on their Russian energy imports.

-

Broader signals of enforcement against Iranian-linked crude shipments.

This sudden squeeze on trade through renewed sanction pressure, has introduced significant uncertainty across Asian energy trade routes. The market quickly repriced geopolitical risk in energy markets, as the shift from rhetoric to enforcement came into the spotlight.

Strategic Realignment: Transatlantic Energy Policy Takes Centre Stage

The US–EU energy pact formalised a structural shift away from Russian energy. While the strategic direction is now set, the timeline for execution remains constrained by infrastructure gaps, regulatory friction, and limited market coordination. Full implementation is expected by 2027, though delays remain likely.

Market views remain split. Some expect geopolitical tailwinds to keep prices elevated, driven by sustained policy risk. Others anticipate a correction as OPEC+ supply ramps up and macroeconomic pressures ease.

Our Trading Co-Pilot Tracks the Breakout

Our Trading Co-Pilot flagged the bullish momentum shift just as Brent cleared $71. The signal aligned with sanctions-driven sentiment, EU policy realignment, and OPEC+ output. Prices moved swiftly toward the $72–$73 range.

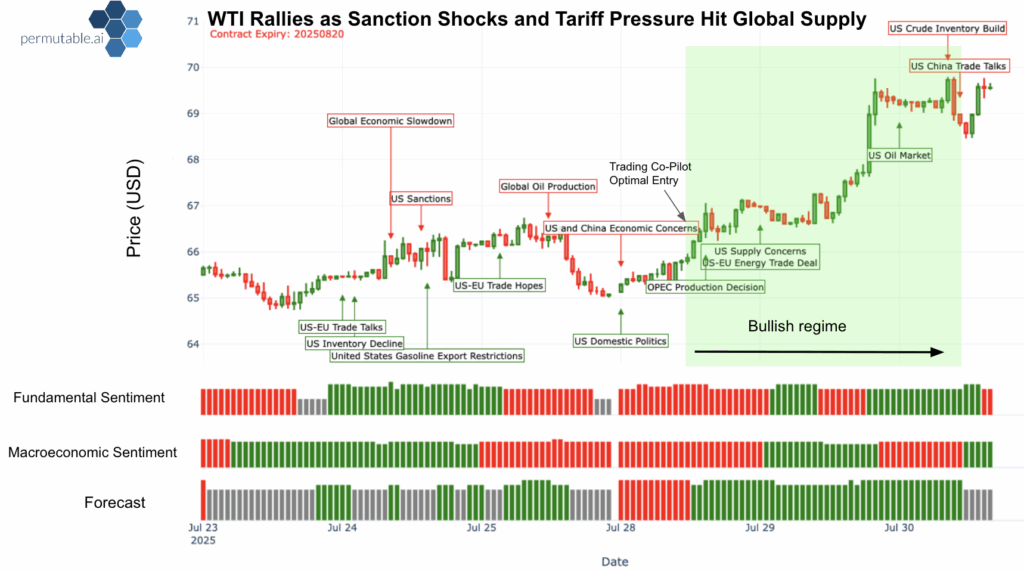

WTI Crude: Tariffs, Sanctions and Supply Signals Push Prices into Bullish Territory

WTI crude held firm near \$69 per barrel this week, as geopolitical risk in energy markets overshadowed a contradictory U.S. inventory picture. The rally was not driven solely by supply dynamics, but by a surge in regulatory pressure, including threats of secondary sanctions, renewed tariff pressure, and shifting trade alignments.

Our Trading Co-Pilot Captures the Regime Shift

Our Trading Co-Pilot identified a bullish regime shift in WTI, marking the point where escalating policy risk and rising sentiment momentum converged. The signal preceded a sharp upward move, offering clients a well-timed entry as the market transitioned into a sustained rally.

Key Movements

- 28–29 July: WTI rallied from $66 to $69 after U.S. inventory draws and the transatlantic energy pact announcement.

- 30–31 July: Prices dipped briefly on upside inventory surprises from EIA and API data.

While our Trading Co-Pilot’s bullish forecast reflects strong directional conviction, risks remain. Inventory build-ups and surging output confirmed by the EIA and API continue to place downward pressure on sentiment, and a proposed reintroduction of Venezuelan exports under Chevron waivers may temper further upside. Still, trade policy remains the dominant driver in the near term.

TTF Natural Gas: Heatwaves and Supply Friction Lift Prices Despite Structural Softness

Dutch TTF gas prices rose from €32.10 to €34.90, driven by a combination of heatwave-related demand, short-term supply constraints, and speculative positioning. However, the rally appears increasingly detached from underlying fundamentals, with structural weakness continuing to weigh on the broader European gas market.

Heatwave Impact: Cooling Demand Drives Short-Term Surge

Extreme heat across Europe boosted short-term gas consumption and triggered speculative activity in power markets. Prices opened at €34.72 on 30 July, buoyed by headlines highlighting U.S.–EU LNG cooperation. Still, recent EIA data showed a drop in Dutch spot prices earlier in the month, reinforcing the view that the rally is regionally concentrated and sentiment-driven.

Supply Strains

- Norwegian gas output declined for a fourth consecutive month.

- UK storage builds slowed, tightening near-term balances.

- Qatar signalled potential LNG disruptions due to maintenance risks.

- China increased Russian pipeline uptake

While these constraints triggered upward price pressure, they are cyclical rather than structural long-term supply weakness.

Demand Headwinds: Structural Softness Still Dominates

- Dutch gas-fired generation fell to multi-year lows.

- EU industrial demand remains weak.

- LNG import expansion is constrained by regulatory and infrastructure delays.

Our Trading Co-Pilot Captures the Rebound

Our Trading Co-Pilot issued a timely entry just under €32.5 mark, detecting upbeat sentiment around weather risks, LNG bottlenecks, and regional supply pressures. The decisive signal positioned clients well ahead of TTF’s rebound towards €35.

Global Energy Markets: The Road Ahead

Recent price action across Brent, WTI, and TTF reflects a market increasingly shaped by political risk, regulatory intervention, and shifting global alignments. As energy markets move further away from traditional fundamentals, traders must adapt to a more volatile, policy-sensitive environment.

Bullish Catalysts

- Enforcement of secondary sanctions on Russian or Iranian oil

- LNG disruptions from Qatar, Hormuz, and U.S. terminals.

- Continued weather driven demand surges in Europe or Asia.

Bearish Headwinds

- U.S. crude builds and refinery throughput spikes.

- Venezuelan supply returns and ramping up of OPEC+ deliveries.

- Further demand weakness from China and a slowdown in Eurozone industrial output.

Where Signal Meets Strategy

This week’s rally across Brent, WTI, and TTF reflects a market increasingly driven by geopolitical risk in energy markets. Traders are no longer reacting solely to supply and demand data, but to policy shifts, enforcement threats, and macroeconomic volatility.

Our Trading Co-Pilot identified these inflection points in real time, blending sentiment analytics, macroeconomic filters, and policy signals into clear, actionable trade calls. Rather than relying on hindsight, our Trading Co-Pilot tracks evolving conditions as they unfold, enabling well-timed entries and exits with conviction. The result is enhanced clarity and precision in trade execution, cutting through market noise and volatility across global energy markets.

To request a demo or speak to one of our team, simply email enquiries@permutable.ai