This article examines the key signals shaping global economic trends in Q4 2025 – from record-high gold prices and falling crude oil to weakening fundamentals across major economies. Aimed at institutional investors, traders, and analysts, it explores how Permutable’s Trading Co-Pilot empowers professionals to interpret market complexity and act decisively amid uncertainty in the global economy.

As we move deeper into Q4 2025, our market intelligence systems are detecting significant contrasts within the global economy. While risk assets such as gold and major equity indices continue to reach all-time highs, our sentiment analytics show persistent weakness across the world’s key G7 economies. This disconnect – rising asset valuations amid weakening fundamentals – is one of the defining global economic trends 2025 is likely to inherit.

Across our datasets, the same narrative emerges: caution, divergence, and regime transition. The global economy news cycle may still focus on growth resilience and policy optimism, but beneath the surface, the indicators point to structural fragility – weak employment data, subdued inflation momentum, and manufacturing stagnation in the United States, Europe, and Japan. By contrast, China remains the outlier, with sentiment reflecting relative strength across industrial production and government support policies.

Table of Contents

ToggleQ4 key global economic trends 2025

Crude oil below $62: The weight of oversupply

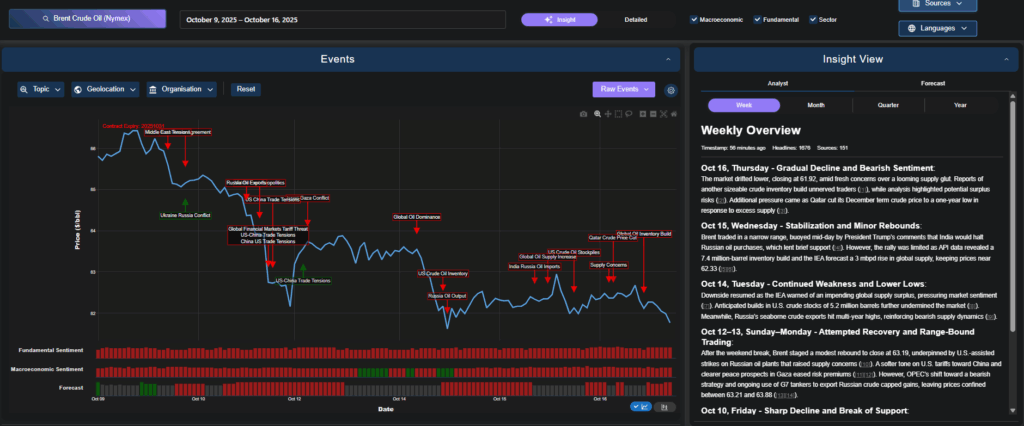

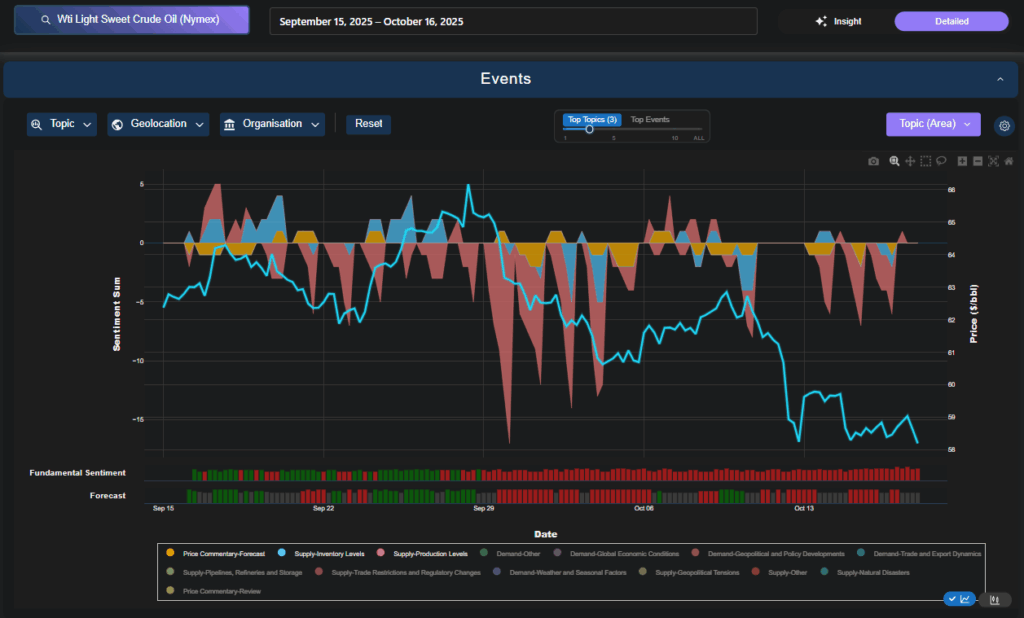

One of the clearest markers of global economic cooling has been the sustained weakness in crude oil prices. Brent crude recently slipped below $62 a barrel, driven by oversupply narratives and muted demand projections.

Our Trading Co-Pilot detected several key developments feeding into this downturn:

Qatar’s December crude price cut to a one-year low, signalling producer concerns over excess supply.

IEA forecasts projecting a 3 mbpd rise in global inventories, amplifying bearish sentiment.

Trade frictions and new restrictions on Russian oil flows, further distorting supply expectations.

The data flow shows that fundamental and macroeconomic sentiment on oil remains consistently negative across October, aligning with the broader caution surrounding global economic trends 2025. In essence, while geopolitical flashpoints continue to add volatility, the dominant narrative is one of oversupply meeting weak demand – a signal that the global economies are slowing collectively rather than cyclically.

Above: Image 1 – Brent crude prices fall below $62 as oversupply concerns intensify. Our Trading Co-Pilot highlights a continued bearish sentiment driven by weak global demand, IEA surplus forecasts, and reduced price targets across major producers; Image 2 – Our oil sentiment analytics show a sharp decline in positive momentum across Q4 2025, signalling persistent macroeconomic weakness and limited support drivers for crude prices amid ongoing trade and geopolitical tensions.

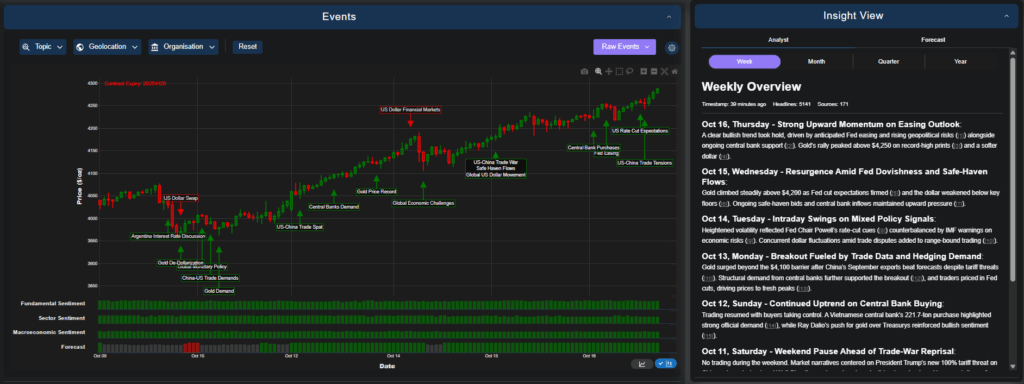

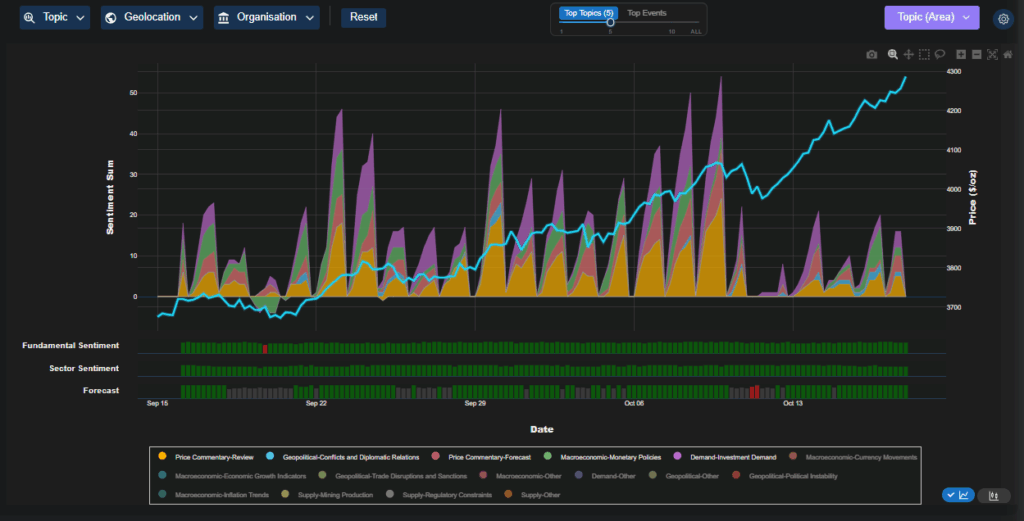

Gold’s unprecedented rally: A signal of caution, not confidence

In stark contrast, gold prices have surged to record highs above $4,250 per ounce, a move our analysts interpret not as exuberance but as a reflection of deep-seated caution within the global economy.

Our sentiment models show strong upward momentum fuelled by three converging forces:

US dollar debasement and growing expectations of rate cuts in early 2025.

Safe-haven flows from both institutional and sovereign buyers seeking refuge from policy uncertainty.

Diverging asset signals, with record highs in US equity indices (S&P 500 and Nasdaq) coinciding with increased volatility in macroeconomic sentiment.

Above: Image 1 – Gold prices reach record highs, reflecting a flight to safety amid expectations of US rate cuts and currency debasement. Our sentiment data captures sustained bullish positioning from institutional and sovereign investors. Image 2 – Our Trading Co-Pilot visualises gold’s sentiment breakdown – revealing elevated safe-haven inflows despite record equity market levels, pointing to deep market caution beneath headline optimism.

Macro indicators: Underlying weakness across regions

Our Trading Co-Pilot’s sectoral analysis dashboard highlights a clear synchronised slowdown across most developed markets.

-

Employment data across G7 economies continues to soften, with rising jobless claims in the US and stagnation in the Eurozone labour market.

-

Manufacturing and industrial production readings show contraction, with sentiment particularly negative in Japan and the UK.

-

Inflation momentum remains muted – a stark contrast to the rate-hiking pressures of 2023.

China remains the lone bright spot, showing resilience in both industrial production and consumer activity. However, even here, sentiment around trade policy and export demand is increasingly uncertain as global trade tensions rise.

The political layer adds further complexity. Our models capture heightened domestic political weakness across major economies – ranging from fiscal gridlocks to elections driving populist shifts. Political sentiment scores are now trending negative across all G7 countries, suggesting policy inertia could further dampen recovery prospects in early 2025.

Currencies and cross-market dynamics

Our heatmap visualisations reveal widening divergence among currencies. The US dollar shows moderate strength, driven by relative economic resilience, yet it faces growing headwinds from policy uncertainty and fiscal stress. The Japanese yen and British pound remain under pressure, reflecting domestic policy weakness, while the Australian dollar and Chinese yuan have emerged as relative outperformers amid stronger trade fundamentals.

This mixed currency landscape highlights a central point: global economies are increasingly desynchronised. The once-tight correlation between major currencies, commodities, and equities has weakened, introducing new challenges for global investors assessing global economic trends 2025. All of which is signalling that investors will likely continue to grapple with a more fragmented and sentiment-driven environment.

Above: Global macro indicators show widespread weakness across the G7 – from soft employment and manufacturing data to declining inflation momentum – while China remains the relative outperformer in an otherwise fragile global economy.

How our Trading Co-Pilot helps investors navigate this new landscape

At times like these 0 when markets are sending conflicting signals and traditional indicators offer little clarity – our Trading Co-Pilot comes into its own.

Built on advanced multi-entity sentiment analysis and real-time data intelligence, our Trading Co-Pilot helps traders, analysts, and asset managers make sense of global market complexity. The system processes millions of data points daily – from global economy news, central bank communications, trade data, and geopolitical reports – and distils them into actionable insights.

During periods of heightened uncertainty, such as we are witnessing now, the Trading Co-Pilot’s value proposition becomes clear:

Contextual intelligence: It links macro, sectoral, and asset-level sentiment to show why prices move, not just how.

Predictive forecasting: By analysing real-time shifts in sentiment across the global economy, it helps identify turning points before they appear in traditional data.

Confidence for decision-makers: Whether trading oil, gold, or indices, users can visualise how different market narratives – from rate cuts to supply shocks – are impacting price sentiment and forecast probability.

In the context of global economic trends 2025, where volatility, political risk, and information overload will define the landscape, the Trading Co-Pilot acts as an essential analytical co-pilot. It empowers professionals to navigate markets with clarity, precision, and foresight – all underpinned by data, not emotion.

Outlook: A turning point ahead

The convergence of weak growth, political uncertainty, and diverging asset signals suggests that global economic trends 2025 will be defined by transition. Gold’s strength and oil’s weakness are not contradictory – they represent two sides of the same macro narrative: capital preservation over risk expansion.

Our analysts interpret the data as signalling an impending shift in the macro regime. Central banks are likely nearing the end of their tightening cycles, and early signs of monetary easing — particularly from the Federal Reserve and European Central Bank – could set the stage for a temporary rebound in sentiment. However, structural headwinds remain: weak productivity, trade fragmentation, and political instability continue to weigh heavily on confidence.

For institutional traders and macro investors, this evolving landscape demands agility. Sentiment analysis and data-driven forecasting, like those surfaced clearly through our Trading Co-Pilot, are becoming indispensable for interpreting early signals hidden within market narratives.

Conclusion: Reading the Signals Beneath the Surface

Q4 2024 marks a critical juncture in the global economy. Despite surface-level strength in equities and gold, the underlying data reflects broad weakness across employment, production, and fiscal health. These patterns form the early contours of global economic trends 2025 — a year likely characterised by shifting monetary policy, rising political risk, and renewed focus on safe-haven assets.

Our Trading Co-Pilot’s continuous monitoring of sentiment and macro-data patterns highlights one message above all: beneath the optimism of record highs lies an economy preparing for change.

Prepare for what’s ahead

Request a demo of our Trading Co-Pilot intelligence suite to stay ahead of impending market shifts with real-time, data-driven intelligence designed for institutional investors navigating complex global conditions. Simply email us at enquiries@permutable.ai to request your demo at a time convenient to you.