What is multi entity sentiment code and do we use it to decode complex market narratives?

07 Jul 2025

07 Jul 2025

In today’s interconnected financial landscape, events rarely impact a single entity in isolation. Headlines often bundle together multiple assets, economies, and companies, each influenced in different ways and to varying degrees. Traditional sentiment analysis tools, while useful, tend to fall short in these nuanced scenarios – typically tagging sentiment to one main entity per text or event.

This is where our multi entity sentiment code comes into its own. Multi entity sentiment code is used to dissect complex narratives and extract sentiment directed at multiple entities simultaneously. By doing so, we surface valuable cross-asset signals that might otherwise be missed – empowering institutional investors with the clarity and context needed to act ahead of the market.

Multi entity sentiment code refers to the classification and quantification of sentiment as it relates to several entities within a single narrative. For example, consider a news story stating: “The Bank of England’s surprise rate hike lifted the pound but dampened FTSE-listed equities.” In this case, there are at least three distinct sentiment implications: a positive outlook for GBP, a negative signal for the UK equity market, and a potential shift in monetary policy sentiment. Most traditional sentiment engines would attach sentiment to only one dominant entity – missing the interplay that skilled analysts would naturally infer. Our approach mirrors that of a domain expert reading between the lines.

At Permutable, we’ve developed a proprietary framework that applies our multi entity sentiment code across thousands of data sources in real time. This includes global news, financial publications, earnings transcripts, regulatory announcements, and macroeconomic updates. Our models are trained not only to identify sentiment at the headline or article level but to assign directional sentiment to each referenced entity with high precision. This allows for the simultaneous tracking of multiple assets, sectors, and economic indicators as they react to evolving narratives.

One of the core strengths of this approach lies in its ability to detect correlated or cascading sentiment effects across markets. In a world where monetary policy decisions in Washington can move bond yields in Frankfurt or trigger a reaction in oil markets, capturing these linkages is essential. Our multi entity sentiment code identifies these interactions early – offering a powerful edge for macro and cross-asset traders seeking to understand the broader implications of fast-moving market events.

At Permutable, the power of multi entity sentiment code goes beyond concept 0 it’s already driving real-time decision-making for our clients across key commodity and macro sectors. Our systems process and apply sentiment to multiple interconnected entities, helping investors understand how individual narratives ripple across global markets. Here are several recent examples that illustrate its effectiveness in practice.

Our most compelling validation came during the Iran-Israel escalation in June 2025. On the evening of June 12th, our War Sentiment Index began detecting unusual patterns in media coverage surrounding Middle Eastern tensions. At 08:14, our algorithms detected the first signals of US-Israeli intent to strike Iran, with Brent crude trading at $69. By 08:30, as Iran defied warnings over uranium enrichment, our sentiment scores were already showing significant negative spikes, though oil prices remained unchanged.

The critical moment came at 21:00 when strike warnings escalated, pushing Brent to $70. By 00:07 the following day, as Israeli Air Force strike announcements broke simultaneously across major outlets, oil had spiked to $74 – a 7% surge our sentiment data had accurately predicted. This demonstrates precisely why we built these systems: by the time traditional intelligence reaches trading desks, market movements have often already occurred, but our multi-entity sentiment analysis captured the correlation between geopolitical tensions and oil pricing in real-time.

In the energy sector, our LNG Intelligence recently surfaced sentiment divergence during geopolitical disruption in major exporting regions. News flow tied to Middle East unrest and North African port disruptions created uncertainty over delivery timetables and pricing. Our sentiment engine assigned bearish sentiment to export capabilities and regional logistics operators, while simultaneously marking bullish sentiment toward Henry Hub and TTF gas benchmarks.

With these overlapping views surfaced in real time, clients could assess exposure across both origin and destination markets, helping them rebalance portfolios or hedge vulnerable positions with confidence. This multi-entity approach enables traders to understand how individual narratives ripple across interconnected global energy markets.

Across each of these scenarios, multi entity sentiment code offered a powerful edge: the ability to track and quantify how the market perceives multiple interconnected factors at once. By doing so, it empowers our clients to act early, to manage risk more holistically, and to understand the broader story shaping asset prices – not just the headline.

This level of granularity is particularly valuable for those who rely on systematic and data-driven approaches to investment. When used in tandem with our Trading Co-Pilot and macroeconomic data feeds multi entity sentiment code acts as a vital input into strategy design, risk modelling, and signal validation. Rather than relying solely on lagging indicators or single-variable datasets, clients can tap into a dynamic, real-time layer of market insight that reflects how the world is interpreting and reacting to economic and geopolitical developments.

We believe the future of market intelligence lies in capturing not only what is happening, but also how it is being perceived across different layers of the market ecosystem. Our use of multi entity sentiment code is a reflection of that belief: real-time newsflow intelligence designed to bring structure to narrative complexity and deliver actionable insights for those navigating high-stakes, high-volatility environments.

At Permutable , we continue to refine our models with human-in-the-loop supervision, domain-specific datasets, and collaborative feedback from our institutional clients. The result is a robust, adaptive system that mirrors the analytical thinking of a seasoned strategist – at machine speed and scale.

Ready to see how multi entity sentiment code can power your investment strategies? Request a demo by emailing enquiries@permutable.ai or explore our Trading Co-Pilot intelligence suite to experience the difference real-time narrative intelligence makes.

Analysis

15 Jul 2026

The Price of Passage: How Geopolitical Sentiment Led the Repricing of Gulf Crude-Flow Risk

Read more >

Analysis

08 Jul 2026

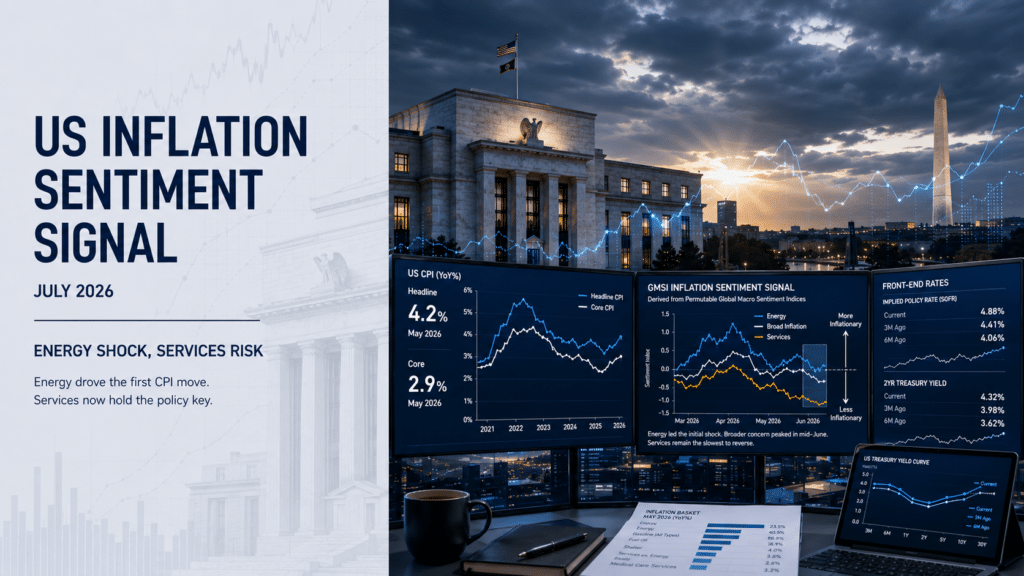

US inflation sentiment signal shows shift from energy shock to sticky services risk

Read more >

Analysis

07 Jul 2026

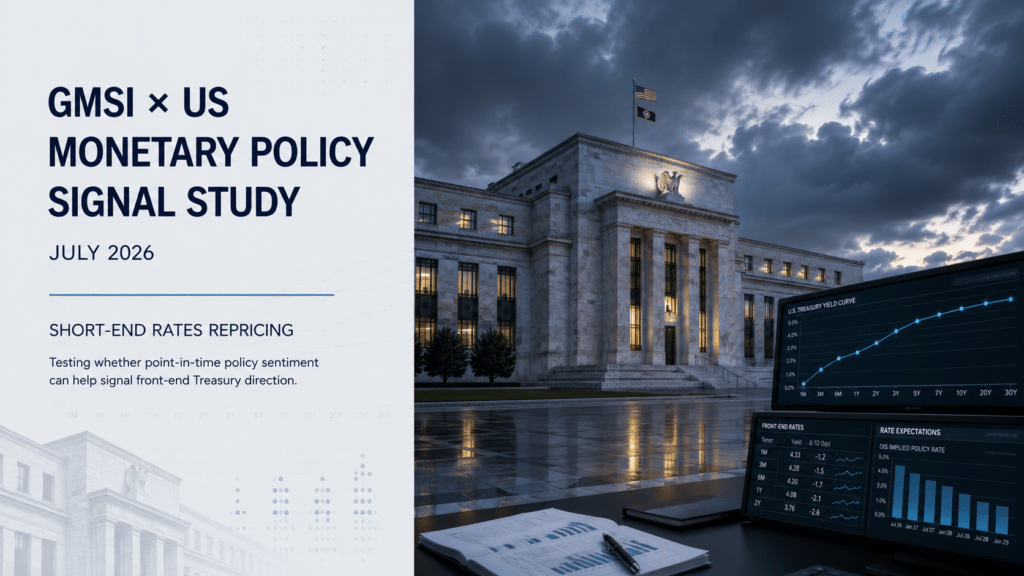

Testing GMSI US monetary policy sentiment as a short-end rates signal

Read more >