Market sentiment indicators September 2025: Regional fractures and commodity rallies define the month

25 Sep 2025

25 Sep 2025

This analysis examines key market sentiment indicators September 2025, focusing on regional market divergences, commodity rallies, and central bank policy shifts. Aimed at hedge funds, institutional investors, and financial professionals seeking advanced market intelligence and sentiment-driven insights for strategic positioning across global markets.

September 2025 delivered a masterclass in how market sentiment indicators can expose the underlying dynamics driving global markets long before traditional macroeconomic data confirms the shifts. Our comprehensive analysis of key market sentiment data this month reveals a landscape defined by regional divergences, commodity strength, and the persistent fragility beneath headline stability.

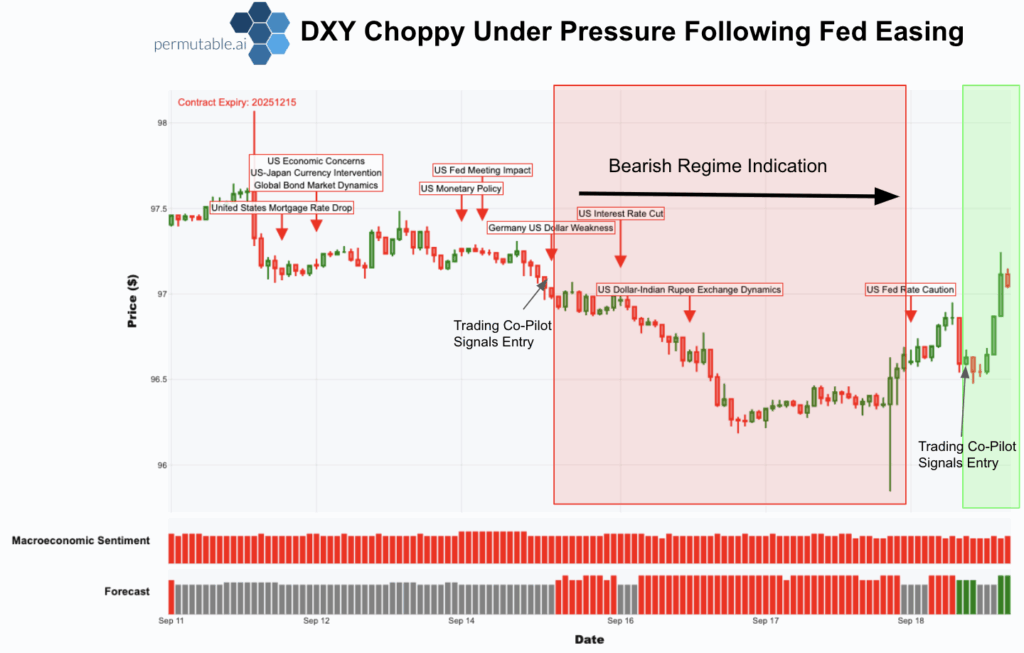

The Federal Reserve’s first rate cut since December 2024 reshaped market dynamics with surgical precision. Our US Monetary Policy Sentiment Index captured the dovish build-up weeks before the 25 basis point cut to 4.00-4.25%, providing hedge funds and institutional clients with early positioning signals that proved decisive.

The dollar’s reaction was swift and telling. The US Dollar Index plunged to 96.25, a three-year low, as our Trading Co-Pilot flagged the structural bearish skew that had been building throughout September. This wasn’t merely a policy response but a fundamental shift in market sentiment around dollar strength, with our commodities intelligence platform identifying the knock-on effects across energy and precious metals markets.

Our market sentiment indicators clearly showed that Powell’s measured tone and firmer inflation projections provided only temporary relief. By Thursday, the greenback had staged a modest recovery to 97.00, but our sentiment analysis revealed this as tactical rather than structural, with the broader trajectory tilted decisively lower.

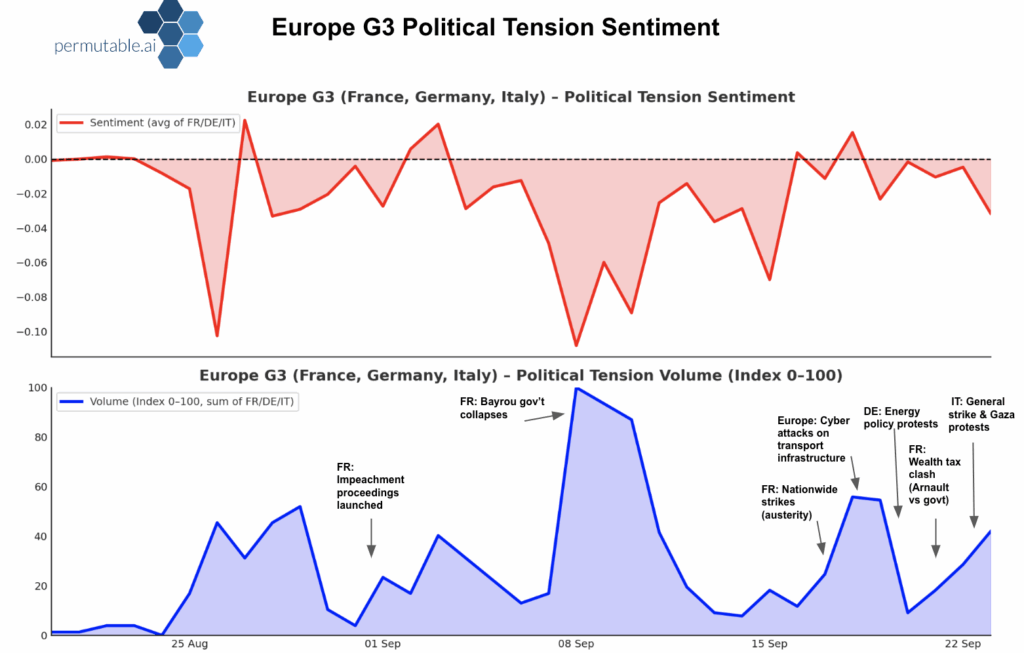

Whilst the US pivoted towards risk appetite, Europe remained mired in political uncertainty that our regional macro indices quantified with stark clarity. France’s wealth tax proposals unsettled luxury equities, whilst political turmoil across Germany and Italy created a persistent drag on market confidence.

Our Political Tension Indices for France, Germany, and Italy remained firmly negative throughout September, with France serving as the epicentre of volatility. The coordinated cyberattack disrupting airline systems across London, Berlin, and Brussels highlighted how infrastructure risks translate directly into market sentiment data, creating opportunities for sophisticated investors to position ahead of the crowd.

This regional divergence created clear relative value opportunities. Our macroeconomic data analysis showed European exporters and cyclicals under pressure, whilst resource-linked names benefited from safe-haven flows that our sentiment models captured in real-time.

September’s standout performer was gold, climbing to record highs of $3,780 per ounce, up 12% for the month. Our Trading Co-Pilot identified gold sentiment as uniquely positioned to absorb capital flows when regional market sentiment indicators diverge.

The precious metal’s rally reflected more than monetary policy expectations. Our commodities intelligence revealed gold functioning as the bridge between US dollar weakness and European political instability. Central bank accumulation continued, with emerging market reserves diversifying away from dollar dominance in a trend our macroeconomic data flagged months ahead of official statistics.

Silver’s accompanying surge past $41.50 reinforced the broader theme. Our analysis identified distinct drivers beyond gold’s coattails, including industrial scarcity and strategic reserve recognition that our commodity sentiment models weighted appropriately.

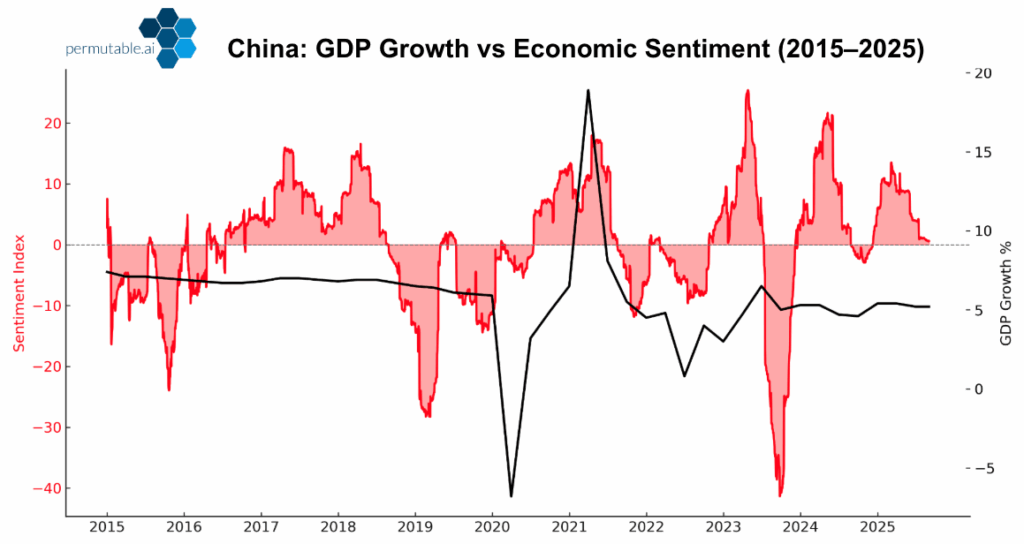

China’s economic narrative epitomised September’s theme of surface stability masking deeper strains. GDP growth held near 5%, yet our China macro sentiment indices revealed households, firms, and investors far more cautious than headline figures suggested.

The property market remained the central drag, with our China Housing Sentiment Index firmly negative since early 2024. Real estate investment fell 11% year-on-year, worse than 2024’s contraction, whilst residential prices continued sliding at -7% annually. Our sentiment analysis captured this persistent weakness with conviction, adding crucial context to official numbers.

Manufacturing presented a more complex picture. Output expanded 5.7% year-on-year, supported by strategic industries, yet our China Manufacturing Sentiment Index peaked in early 2024 and declined through 2025. This divergence between solid output growth and weakening sentiment highlighted markets’ view of current strength as brittle, reliant on subsidies rather than sustainable demand.

Energy markets approached Q4 in what our commodities intelligence described as fragile equilibrium. Supply abundance weighed on prices, with OPEC+ adding 137,000 barrels per day in October and US output hitting record levels at 13.4 million barrels daily.

Our energy market sentiment indicators captured the persistent geopolitical risk premium that provided support despite oversupply. Drone strikes on Russian infrastructure and Houthi Red Sea activity sparked price spikes, yet most rallies proved fleeting against structural supply weight.

Weather risk remained the wildcard, with La Niña probabilities at 55-71% for Q4. Our Trading Co-Pilot scenario analysis across 1-day to 6-month horizons provided weighted probabilistic outcomes, enabling institutional clients to position for convergence of multiple drivers.

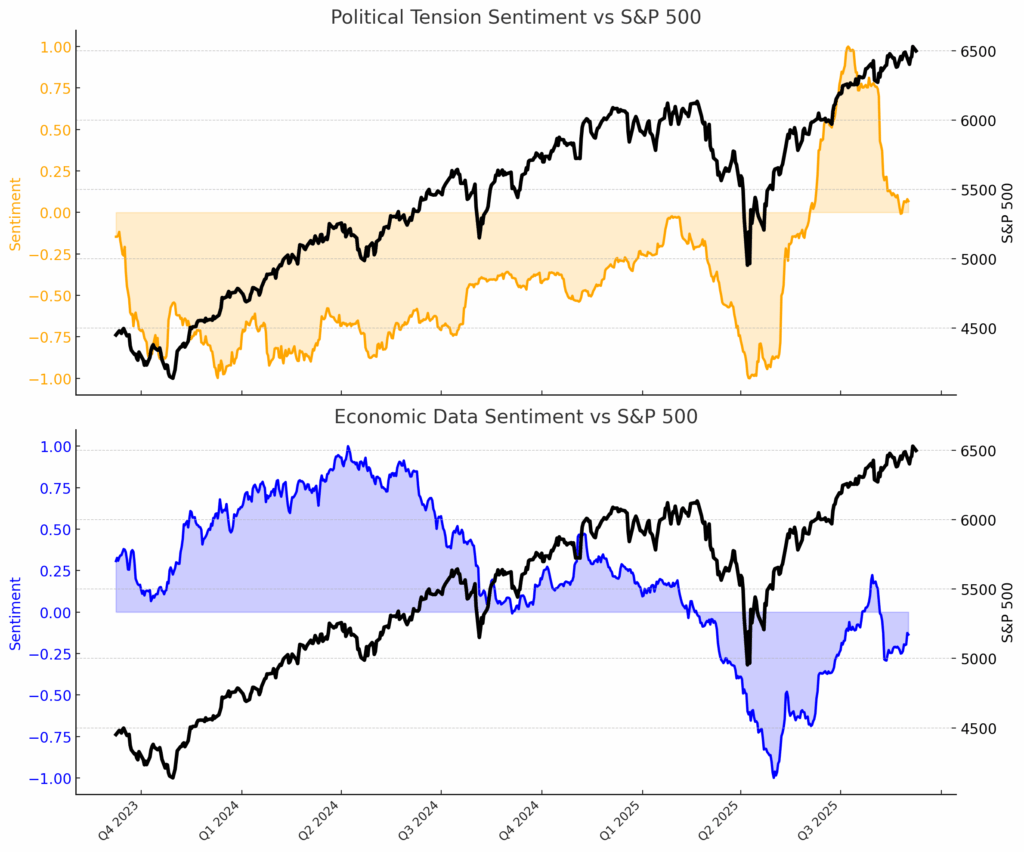

September’s equity performance presented a compelling case study in sentiment-driven markets. The S&P 500 rally persisted despite weakening economic fundamentals, with the Bureau of Labor Statistics’ historic downward revision halving job growth estimates yet equity markets powering to fresh record highs. Our Political Tension Index revealed the underlying dynamics driving this apparent disconnect, capturing how initial corporate anxiety around Trump’s tariff measures gave way to adaptation strategies as firms renegotiated supply chains and passed costs to consumers.

The key insight from our sentiment analysis lies in understanding that markets price expectations, not historical data. When job growth weakens, traders interpret potential Fed responses—looser policy, cheaper credit, and risk asset support – which our GDP Narrative Index and Policy Rate Index captured in real-time. This dynamic reinforces why market sentiment indicators serve as leading rather than lagging measures, with narratives about monetary policy, AI productivity gains, and dollar weakness driving positioning long before hard data could confirm directional changes.

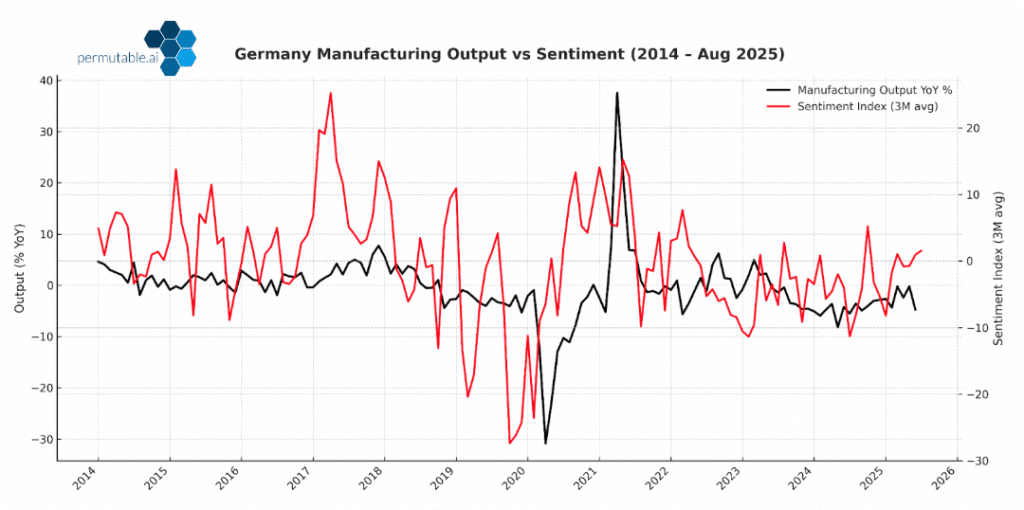

German manufacturing offered September’s most nuanced sentiment story. After 25 months of contraction, our German Manufacturing Sentiment Index began stabilising, with volatility easing and expectations no longer set on relentless decline.

This matters because market sentiment indicators often turn before hard data. Whilst output remained fragile, sentiment’s levelling suggested the contraction phase was ending. Our macroeconomic data analysis identified this as a potential turning point for eurozone recovery, given Germany’s role as the industrial hub.

September 2025 demonstrated why sophisticated investors rely on market sentiment indicators rather than lagging economic data. Our Trading Co-Pilot and regional macro indices provided early signals across multiple asset classes, from the Fed’s dovish pivot to gold’s safe-haven rally to China’s underlying fragility.

The month’s key lesson centres on divergence. When traditional correlations break down and regional sentiment fractures, opportunities emerge for those equipped with real-time sentiment analysis. Our commodities intelligence and macroeconomic data platforms transformed fragmented market developments into coherent signals for enhancing cross-asset strategies.

For hedge funds and institutional investors, September reinforced that market sentiment data functions as the economy’s heartbeat, capturing shifts in confidence that official statistics smooth away. In an environment where macro shocks move markets instantly, sentiment-driven intelligence delivers both risk resilience and early advantage in spotting opportunities before they become consensus trades.

September’s market dynamics demonstrate why leading institutional investors increasingly rely on sentiment-driven intelligence to navigate complex global markets. Our comprehensive suite of market sentiment indicators, commodities intelligence platforms, and macroeconomic data analysis transforms fragmented market narratives into actionable signals for hedge funds and sophisticated investment strategies.

Looking to access real-time sentiment analysis that captures market-moving dynamics before they appear in traditional data?

Contact our team at enquiries@permutable.ai to request a demonstration of our Trading Co-Pilot, regional macro indices, and commodities intelligence and discover how sentiment-led market intelligence can enhance your investment edge and risk management capabilities across global markets.

Analysis

22 Jul 2026

UK inflation fell to 2.6% after Permutable’s Global Macro Sentiment Indices saw it coming

Read more >

Analysis

21 Jul 2026

China growth: Q2 GDP lays bare the limits of industry-led expansion

Read more >

Analysis

15 Jul 2026

The Price of Passage: How Geopolitical Sentiment Led the Repricing of Gulf Crude-Flow Risk

Read more >