In this Energy Market Outlook 2026, we demonstrate how 2025 marked a clear shift in market dynamics and how this will continue into the year ahead. Fundamentals remained the bedrock, yet sentiment increasingly shaped positioning and the direction of trade. Even with stable supply, soft demand and well-stocked inventories, markets moved in ways that the physical data did not fully justify.

What the past year has shown is that sentiment swings, policy uncertainty and geopolitical tension often eclipsed fundamentals, pulling prices off course. On the surface, the global energy system appeared balanced: Brent averaged around $69/bbl, global inventories rose by almost 1.8 mb/d and Europe entered winter with gas storage levels that would have seemed extraordinary not long ago.

Energy traders now enter 2026 facing a market shaped by geopolitical instability, rapid information flow and increasingly complex cross-commodity dynamics. It is now clear that while traditional supply-demand analysis remains essential, it no longer captures the true impulse of price formation. Market-moving events now emerge with little warning, and their influence moves through Brent, WTI, LNG, TTF and Henry Hub long before fundamentals have time to adjust. In this environment, traders are increasingly turning to advanced market intelligence and AI-powered sentiment systems to interpret shifting political signals, sanctions risk, trade disruptions and regulatory changes in real time.

Why sentiment now sits at the centre of strategy

Throughout 2025, markets behaved as though the underlying structure were far more fragile than the fundamental data implied. Geopolitical tension, policy volatility, temporary refinery outages, LNG flow disruptions and shifting OPEC signals repeatedly became catalysts for rapid repricing. A single headline could move entire curves, particularly when weather-driven demand uncertainty made markets more sensitive to perception.

What defined the year, and will now define 2026, is the speed at which sentiment adjusts compared with the far slower cadence of physical balances and traditional data. Market psychology reacts first, barrels, cargoes and pipeline flows respond later. This timing gap has reshaped the informational hierarchy. Geopolitical awareness, real-time sentiment data and clean signal extraction have become core components of modern trading strategies.

It is against this backdrop that our Energy Market 2026 Outlook examines the five sentiment drivers now shaping energy prices. The analysis maps how geopolitics, trade and flows, supply dynamics, weather expectations and shifting demand patterns interact, and how sentiment around each channel emerges well before fundamentals shift. The aim is to illustrate why markets have become so reactive, why early signals matter and how traders can use our sentiment-driven intelligence to position ahead of the rest.

1. Geopolitics: The first spark and fastest market catalyst

Geopolitics remained the most powerful catalyst for sentiment shifts in 2025. Markets consistently responded to the probability of disruption rather than to disruption itself, with price action unfolding well in advance of any observable change in physical balances.

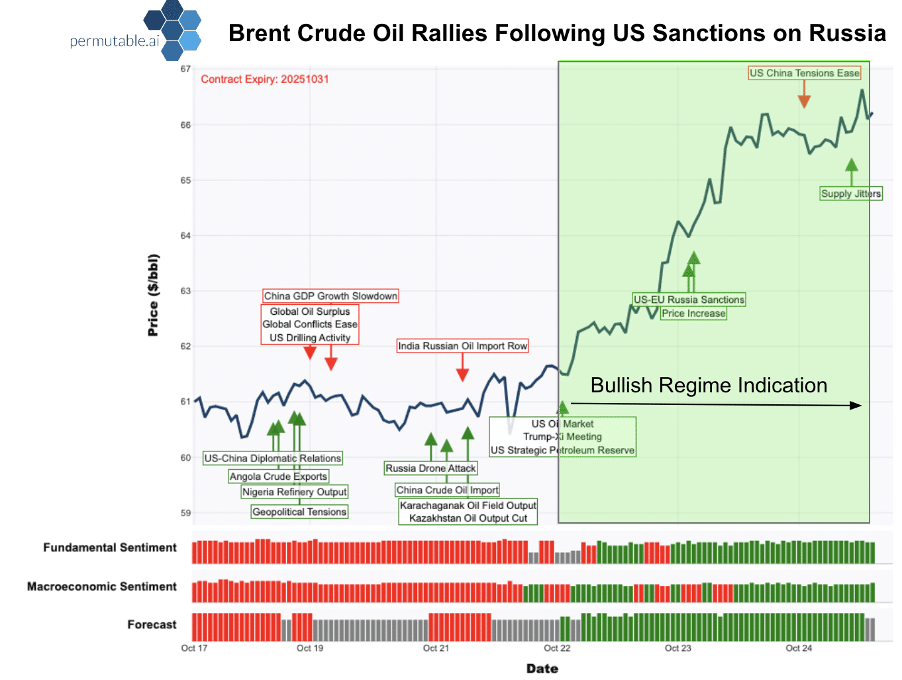

The Iran-Israel escalation in June offered a clear demonstration of this behaviour. As coverage intensified across major global outlets, our sentiment signal registered a rapid and uniform surge in negative sentiment. By the time the first official strike announcements appeared across major news outlets shortly after midnight, Brent had already risen from roughly $69 to $74.

For traders relying solely on fundamentals, this move appeared sudden. For those tracking real-time geopolitical sentiment, the build-up was visible hours earlier. The scale and consistency of the sentiment readings produced one of the highest-confidence signals observed in the past year, reflecting not only the volume of geo-political coverage but also its concentrated tone. Historically, such clusters precede sharp adjustments in crude, and the June episode followed this pattern precisely.

This reflexive behaviour repeated throughout 2025. Tighter US sanctions on Russian entities in October, intermittent strikes on refining infrastructure, drone activity around export terminals and renewed tensions in the Middle East all generated rapid swings in sentiment that markets priced immediately.

Volatility rose, crude benchmarks strengthened and defensive positioning increased even when physical flows were largely unaffected. The market consistently traded the perceived risk landscape rather than realised disruption.

The cooling phase was equally telling. Early indications of Russia-Ukraine peace discussions softened geopolitical sentiment before any formal diplomatic progress was confirmed. Gasoil prices retreated, crude benchmarks eased and timespreads compressed as markets unwound the conflict premium.

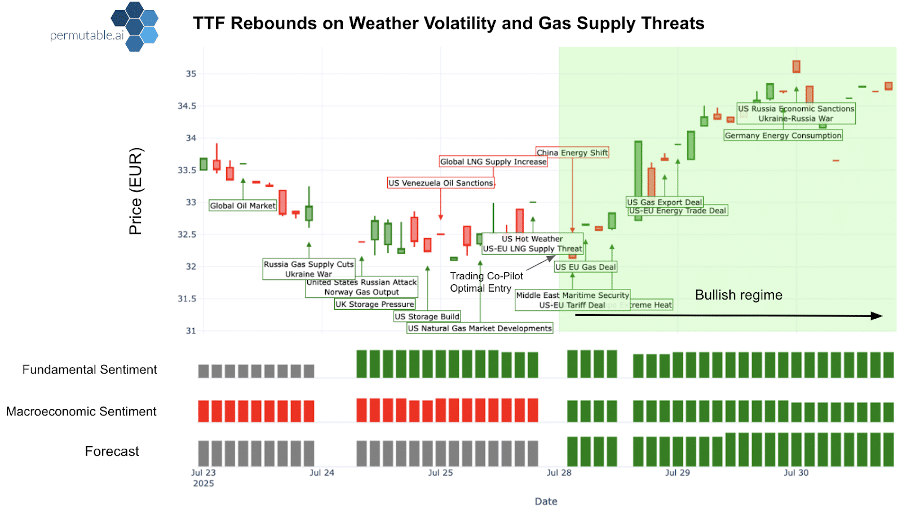

Similar dynamics were visible in gas markets, where TTF fell to an 18 month low amid more appeasing geopolitical rhetoric and benign weather expectations, despite no structural change to European supply fundamentals.

How sentiment feeds integrate directly into trading workflows

Across all these episodes, a clear sequence emerged. A prominent initial shift in geopolitical tone, followed by a rapid accumulation of sentiment, a reassessment of inflation and policy risk, and then decisive movement across futures curves and spreads. The timing repeatedly showed sentiment eclipsed fundamentals in attaining alpha.

Looking ahead to 2026, this sentiment channel remains the earliest and most reliable indicator of geopolitical risk transmission into energy markets. Trading desks treat geopolitical sentiment as a core input rather than an auxiliary overlay, using it to guide exposure, identify the durability of price moves and anticipate volatility clusters.

In a market environment where geopolitics acts as the first mover, the ability to quantify and interpret sentiment shifts is now essential for maintaining an edge.

2. Trade and Logistics: Turning friction into edge

If geopolitics sets the spark, trade and logistics determine the size of the flame. In 2025, the market was rarely short of crude or gas, it was short of energy that could be delivered quickly. This made logistics one of the most potent sentiment channels of the year.

The reordering of global flows, driven by sanctions and diplomatic realignment, reshaped shipping patterns. Asian refiners leaned more heavily on Middle Eastern grades, while European buyers accepted longer voyages from the Atlantic Basin. Freight costs mattered less than time. Delays, however minor, created actionable signals.

Crude on water volumes surged in October, deepening discounts in the physical market but tightening prompt crude spreads as delays built. Temporary loading issues at Primorsk, backlogs at Corpus Christi and slower Panama Canal transits created outsized moves when sentiment was already fragile. Even whispers of friction in the Strait of Hormuz generated measurable shifts in flat prices and spreads.

These signals were subtle at first a rise in chartering, slightly longer voyage estimates, quiet rumblings about reduced vessel availability. But together they marked the early slope of a sentiment turn. Once positioning acknowledged the friction, spreads moved sharply and the advantage shifted to desks that recognised the buildup early.

In 2026, trade and flows will become even more decisive. The ramp-up in US LNG export capacity, particularly Golden Pass Trains 1 and 2 and Corpus Christi Stage 3 heightens global sensitivity to Gulf Coast weather, pipeline constraints and shipping congestion.

With Russian barrels remaining on longer routes, bottlenecks persist both physically and psychologically. In this environment, logistics sentiment becomes a leading indicator for curve structure, WTI-Brent spreads and refining margins.

3. Supply Dynamics: Globally ample, perceptively fragile

Supply looked comfortable on paper in 2025. Global liquids output rose by nearly 2.8 mb/d, driven by Brazil, Guyana, the US and Canada. OPEC+ added modest supply. China built around 0.8 mb/d into its strategic reserves. On the surface, the world was well covered.

Yet markets traded as though supply were fragile. The distinction was between total supply and available supply. Refinery outages, adverse weather, sanctions-driven friction and longer shipping routes created pockets of tightness that the market treated with disproportionate urgency.

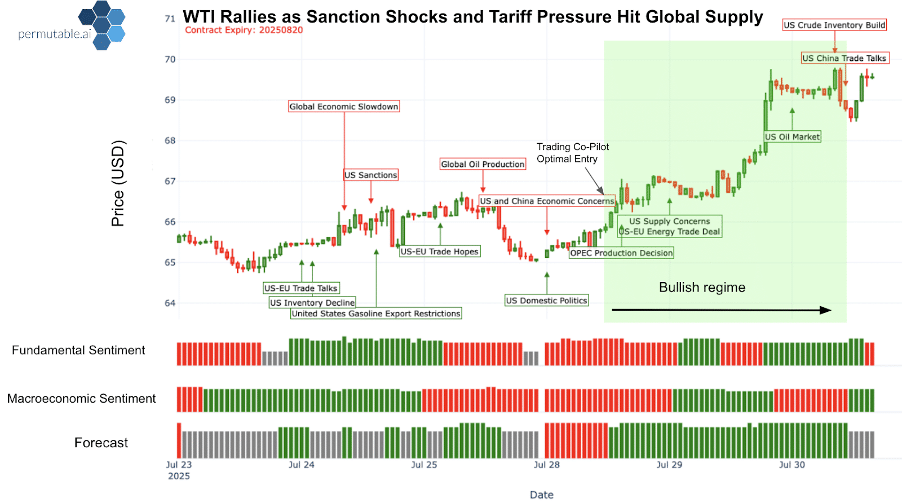

A late-September US draw approaching one million barrels triggered sharp WTI and Brent rallies, even as global supply remained ample. October’s large US inventory build reversed those gains with equal speed. These moves were driven by shifts in sentiment around marginal availability, not by the global balance itself.

Gas showed similar reflexive behaviour. Europe’s storage remained near the top of its historical range, yet temporary renewable shortfalls or mild cold snaps generated rapid tightening in regional spreads. The market priced the risk of tightness far more aggressively than tightness itself.

In 2026, supply is expected to remain structurally loose, but markets will continue to react most forcefully to disruptions at the margin. Temporary outages, refinery maintenance, Gulf Coast weather incidents or pipeline constraints will be priced quickly. Fundamentals set the backdrop; perceived availability sets the move.

4. Weather: The most immediate transmission channel

Weather became the fastest-moving sentiment channel in 2025, particularly for gas. Markets consistently traded the trajectory of forecasts rather than realised conditions. A mild-winter revision in November softened TTF ahead of any physical change. Small downgrades in Northern European wind output tightened LNG spreads within hours. Cold-blast revisions in the US reshaped Henry Hub positioning long before demand shifted.

These moves were psychological first, physical second. LNG flow expectations, storage assumptions and cross spreads all adjusted on model updates alone. Weather became a tradable narrative rather than a realised event.

With expanding US LNG exports, a volatile hurricane season and variable renewable output, weather sentiment will play an even larger role in 2026. Desks will continue to trade forecast volatility as a signal, adjusting risk around model changes rather than waiting for confirmation.

5. Demand: Supportive, but not in the driving seat

Demand remained the softest and most sentiment-elastic layer in 2025. Global liquids consumption rose modestly, driven by emerging markets. OECD demand was flat. Europe’s diesel consumption remained weak. China provided stability through refinery runs and strategic accumulation, yet industrial softness capped upside.

Markets traded the sentiment around demand far more than demand itself. Spikes in data, seasonal travel patterns, refinery margin improvements or headlines about potential Chinese stimulus generated bursts of price movement that often faded quickly. Demand became a reinforcement mechanism, capable of extending rallies when positive, but rarely powerful enough to initiate them.

In 2026, demand is likely to stabilise as the growth and industrial outlook is set to pick up. It will determine the durability of moves, not their direction. Positive demand sentiment supports positioning, while weak demand sentiment limits upside. Demand’s role is one of support but is unlikely to be the primary driver.

Sentiment sets direction, fundamentals validate

As we approach 2026, the global energy system is fundamentally well supplied. Inventories are rising, supply growth remains robust and demand is soft but stable. Yet if we have learnt anything from 2025 it is that it clearly and repeatedly showed that fundamentals alone do not govern price.

Market sentiment now precedes as the market mover, shaping energy market dynamics long before physical balances shift.

Each major market move followed the same pattern. Sentiment emerged across geopolitical, trade or weather channels, then gathered momentum and only later broke into price. Those relying on traditional indicators often entered late. Those monitoring sentiment analysis and alternative data feeds captured the move at its inception.

Sentiment in Practice: From early signal to executable insight

In practice, systematics use our sentiment layers as early signals. When macro, geopolitical or market fundamental sentiment begins to shift, traders take note and reassess positioning. They watch spreads more closely, adjust crude exposure if needed and tighten or loosen risk limits. This turns sentiment into a guide for day-to-day decisions in a clear and practical way.

This is why institutional desks and systematics are increasingly integrating our real-time data-intelligence feeds ready for 2026. Early signals on geopolitical stress, emerging flow congestion or developing weather risks provide visibility before consensus forms.

Turning volatility into alpha through real-time sentiment

Our data intelligence feeds have been developed for seamless integration through our API, clean, time-aligned and structured for model ingestion. They enhance predictive accuracy, support tighter risk controls and help desks recognise turning points earlier in increasingly sentiment driven markets. In a landscape where perception moves first and fundamentals follow, incorporating sentiment into forecasting, portfolio construction and execution is no longer optional.

Our data intelligence engine and live insights feed consistently captures these early inflection points. Our systematic trading performance this year reflects the edge, highlighting the power of sentiment when effectively placed inside a strategy.

Sentiment turning points have a clear edge, opening a window for traders to adjust risk, initiate positions or protect exposure far more efficiently than with fundamentals alone.

For data integration enquiries, or to explore how clients embed our energy sentiment layers into trading models, portfolio construction or risk systems, contact: enquiries@permutable.ai for a walk through.