Volatility is often framed as an aberration – something to be managed, reduced or hedged away. In practice, for institutional investors, volatility is better understood as the market’s mechanism for processing uncertainty about the world beyond prices. It reflects not only changes in supply and demand, but shifts in narratives, policy credibility, geopolitics and collective expectations.

Recent moves in precious metals have reinforced this point. Both silver and gold have experienced sharp repricing episodes that, on the surface, appear extreme. Yet beneath the price action, sentiment data shows these moves were not random. They were the result of narratives becoming more coherent, more persistent and more widely reinforced across macro, geopolitical and investment channels.

In commodities, FX and other macro-driven markets, price action is increasingly shaped by these forces. Single data points matter less than how markets interpret evolving stories: how sanctions alter energy flows, how governments respond to inflation, or how political risk reshapes confidence in currencies. In this environment, understanding volatility requires context as much as calculation.

This is where our macro sentiment indicators become valuable – not as trading signals, but as tools for interpreting why markets are behaving the way they are.

From raw information to macro intelligence

At Permutable AI, macro sentiment is treated as a form of intelligence rather than opinion. By analysing global news and policy communications in real time, our intelligence layer tracks how narratives emerge, gain momentum and fade, and how those shifts align with market behaviour.

The objective is not to predict outcomes, but to reduce ambiguity around what markets are responding to at any given moment. In volatile environments, clarity around causality is often more valuable than conviction about direction.

This distinction has been particularly important in recent precious metals markets, where sentiment-led regime shifts preceded some of the largest price moves seen in years.

Understanding volatility regimes

A recurring challenge in volatile markets is misidentifying the underlying regime. Not all volatility is created equal. Some episodes reflect structural macro change, while others are driven by positioning stress, liquidity constraints or microstructure effects. These regimes can look similar on a price chart, yet behave very differently over time.

Here, our macro sentiment indicators help distinguish between them by revealing whether market narratives are coherent, persistent and broadly reinforced, or fragmented and unstable. When sentiment builds consistently around structural themes – such as policy credibility, physical tightness or geopolitical risk – volatility tends to persist and propagate across related markets. When sentiment is contradictory or rapidly shifting, volatility is more likely to be noisy and self-correcting.

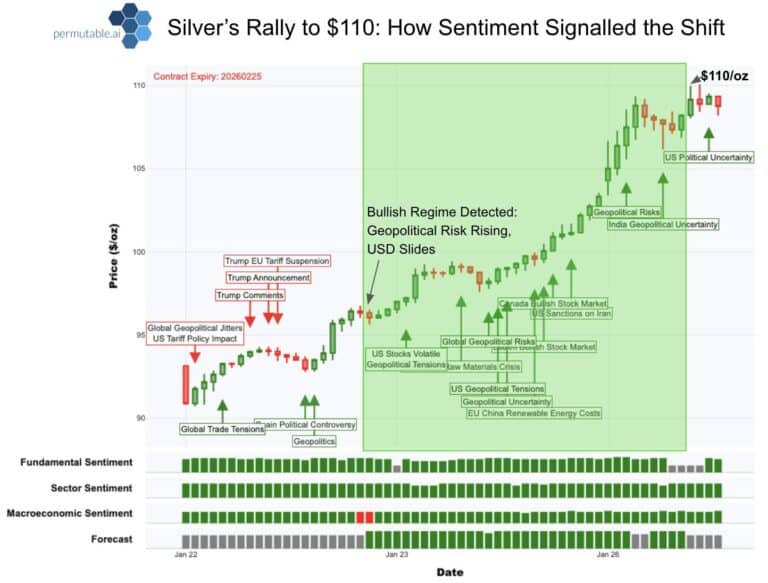

Recent silver market example

Recent developments in silver provide a clear illustration. As prices accelerated sharply higher, sentiment data identified the emergence of a bullish regime driven by rising geopolitical risk, a weakening US dollar and increasing concern around physical market tightness. Importantly, this regime was detected before the most aggressive phase of the rally.

Rather than fading volatility, sentiment coherence increased as prices rose. This signalled that the move was being reinforced by narrative momentum rather than undermined by it. The subsequent rally toward $110/oz reflected not just speculative demand, but a market repricing risk across macroeconomic, political and investment dimensions.

Above: Silver volatility regime in focus – chart illustrates how escalating geopolitical risk and macro uncertainty pushed silver into a bullish volatility regime. Coherent sentiment reinforced volatility, amplifying the move toward $110/oz as markets repriced risk.

Narrative momentum and market timing

Markets rarely move decisively on a single headline. Instead, they react as narratives gain acceptance across regions, institutions and asset-specific commentary. Tracking this narrative momentum allows investors to see when a story is transitioning from background noise into a dominant driver of price behaviour.

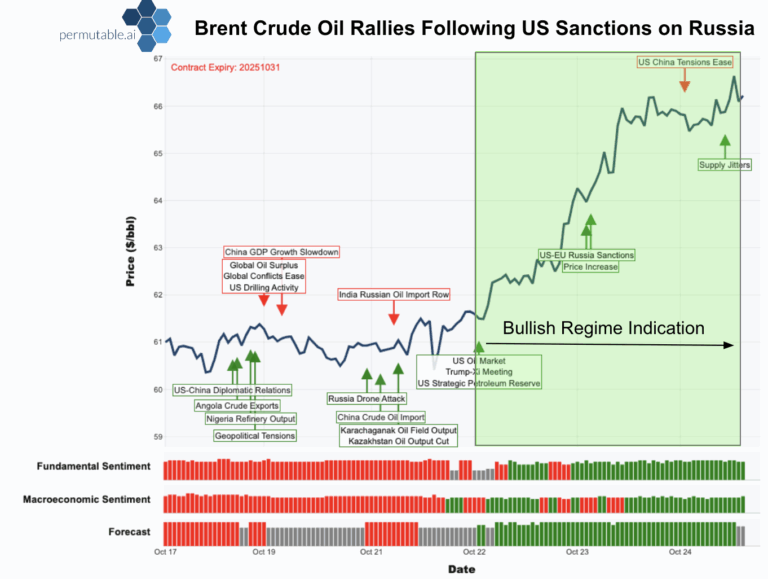

This dynamic has been visible in recent energy markets. During periods of heightened geopolitical tension, sentiment related to sanctions, shipping risk and supply disruption often begins to build gradually. By the time price action reflects a clear directional move, much of the repricing has already occurred.

Here, macro sentiment indicators do not function as predictors. They provide visibility into how the market’s collective interpretation is evolving beneath the surface, helping investors understand why volatility is emerging before it becomes obvious in price alone.

Above: Permutable AI’s macro intelligence captures a clear regime shift in Brent crude as sanctions-driven supply risk sentiment overtakes growth concerns, triggering a sustained price rally.

Volatility persistence versus volatility noise

Volatility presents a challenge not just for opportunity, but for interpretation. Elevated volatility can reflect genuine repricing, or it can reflect confusion. Distinguishing between the two is critical for institutional portfolios.

One of the less obvious applications of macro sentiment indicators is assessing whether volatility is likely to persist. When sentiment remains coherent and directional, volatility often reflects durable shifts in expectations. When sentiment oscillates rapidly or lacks a clear narrative anchor, volatility tends to be less durable.

This distinction matters most during periods of macro transition, when historical relationships become unreliable and traditional volatility metrics struggle to differentiate between risk and randomness.

Event-based frameworks and repeatability

Over time, institutional investors tend to internalise volatility patterns by building frameworks around event types rather than reacting to each development in isolation. Effective macro analysis treats sanctions, strikes, regulatory shifts and supply disruptions as repeatable categories with characteristic narrative arcs.

Anchored macro sentiment indicators support this approach by linking sentiment changes to specific event classes and tracking how markets have historically responded. This helps reduce reliance on ad-hoc interpretation and improves consistency in how volatility is assessed across cycles.

Widening distributions and policy credibility

Some of the most consequential volatility episodes are not directional, but characterised by widening outcome distributions. In these environments, markets are not converging on a single expectation, but reassessing the range of plausible futures.

FX markets provide a clear example, particularly when political or policy credibility comes into question. Macro sentiment indicators can reveal when a currency begins to trade less like a yield instrument and more like a risk instrument.

Recent yen dynamics reflected this shift clearly, with political narratives reshaping market behaviour before traditional macro indicators adjusted. The insight here is not about where price will settle, but about recognising when uncertainty itself is being repriced.

Above: Our sentiment heatmap reveals broad-based bearish pressure on the Japanese yen, with macro, political, and monetary policy narratives reinforcing downside price drift.

Macro sentiment indicators use case: sanctions and narrative momentum in energy markets

Consider a European-based commodities fund monitoring crude markets during a period of escalating geopolitical tension. In the early stages, headlines about potential sanctions appear sporadically, with limited immediate price reaction. Traditional indicators suggest minimal near-term impact, and positioning data shows no clear crowding.

However, macro sentiment indicators begin to show a different picture. References to sanctions increase in frequency, but more importantly, the tone and context evolve. Commentary increasingly links sanctions to physical supply routes, insurance risk and enforcement credibility. The narrative becomes more specific and more interconnected across regions.

Prices remain range-bound, but volatility begins to rise subtly. In this context, sentiment does not imply an immediate directional move. Instead, it signals that the market is transitioning into a regime where outcomes are becoming more asymmetric, meaning subsequent developments are likely to be absorbed more forcefully.

This mirrors patterns we have highlighted time and again, where narrative momentum preceded sharper repricing once formal policy actions or logistical disruptions materialised.

Narrative exhaustion and late-stage volatility

Sentiment is equally important at the other end of the volatility lifecycle. Trends often persist beyond their initial justification, but the narrative fuel that sustains them eventually weakens.

One of the more subtle signals available to institutional investors is the divergence between continued price movement and fading sentiment momentum. When sentiment flattens while prices continue to move, risk-reward dynamics often change. Our macro sentiment indicators are particularly useful here, as they track narrative exhaustion rather than price exhaustion.

This does not imply an imminent reversal, but it does suggest that volatility is becoming less asymmetric and more vulnerable to disappointment.

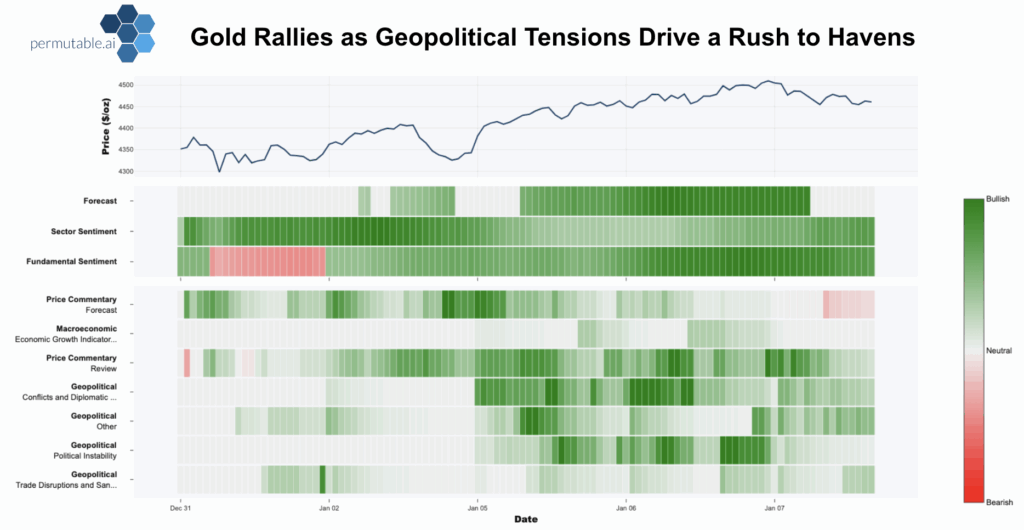

Geopolitical clustering and early warning

Geopolitical risk rarely arrives without warning. It is often preceded by clusters of related narratives that gradually coalesce into a dominant risk theme. Shipping advisories, diplomatic statements and regional developments may appear disconnected until viewed collectively.

By monitoring narrative clustering, our macro sentiment indicators can act as early warning systems for repricing risk premia. This is especially relevant in commodities, where markets often price the risk of disruption well before physical impacts appear in inventories or flow data.

Above: Our sentiment heatmap shows a broad-based shift toward bullish geopolitical and macro sentiment, reinforcing gold’s safe-haven bid during periods of rising global tension, this time in relation to the Venezuela crisis.

Making sense of macro-driven markets

Ultimately, the value of macro sentiment lies in its ability to transform volatility from noise into information. It provides a framework for interpreting market behaviour that complements quantitative models and fundamental analysis, rather than competing with them.

In a world where markets respond as much to narratives as to numbers, understanding how those narratives form and evolve is no longer optional. For institutional investors navigating persistent volatility, our macro sentiment indicators are becoming a foundational component of macro intelligence used by some of the world’s biggest hedge funds, asset managers and Tier 1 banks – helping them understand not just what markets are doing, but why.

At Permutable AI, our focus remains on delivering that clarity, enabling investors to see volatility not as chaos, but as a structured expression of global events working their way through markets.

Explore macro volatility with greater clarity

As geopolitical risk, policy uncertainty and shifting macro narratives continue to drive markets, understanding why volatility emerges is becoming increasingly critical for institutional investors. Discover how our macroeconomic and geopolitical datasets help interpret volatility regimes, narrative momentum and risk repricing across global markets.

Explore our datasets or request trial access to our real-time datafeeds by emailing enquiries@permutable.ai to see how macro sentiment becomes actionable intelligence.