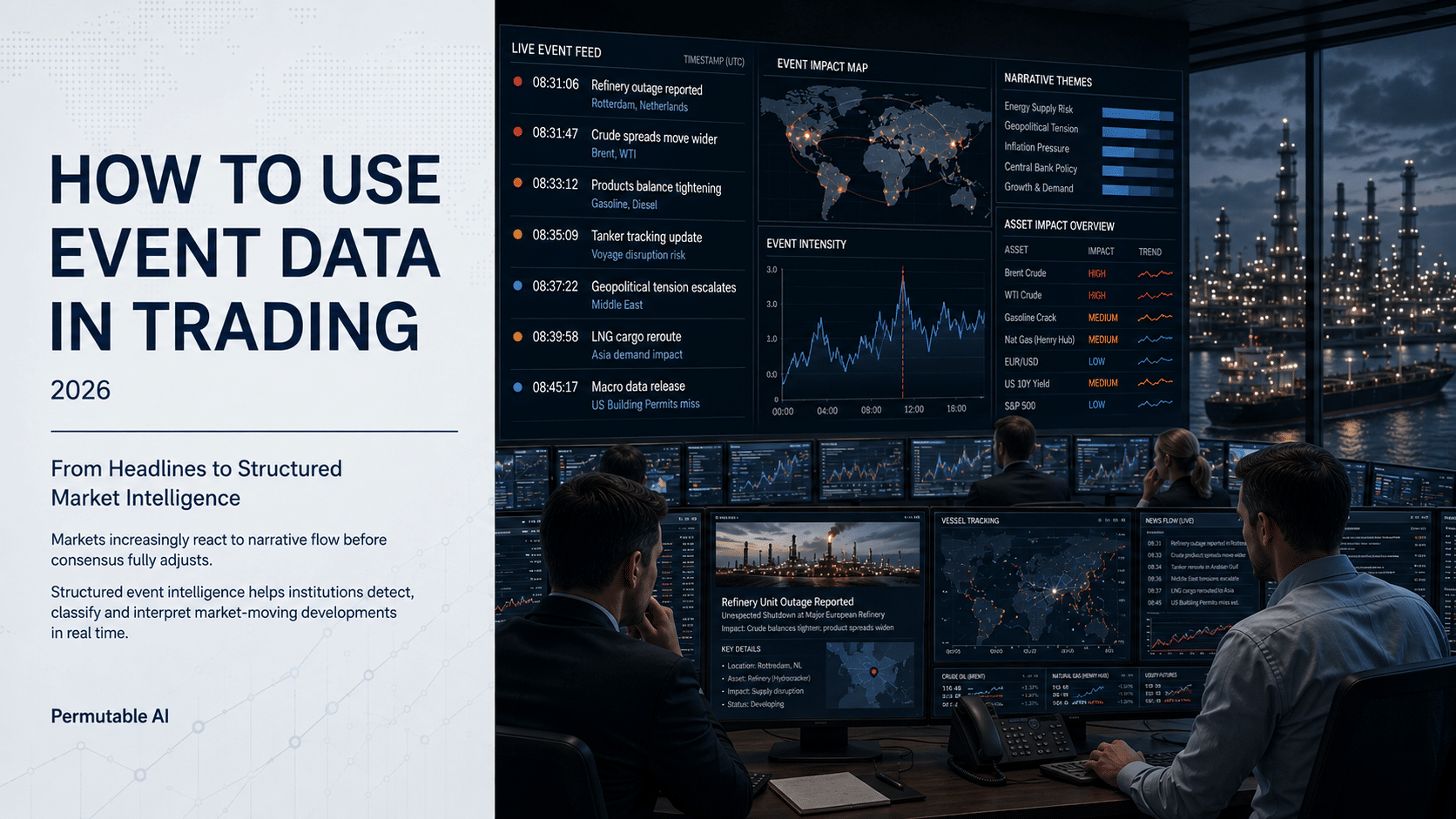

How to use event data in trading

This article explores how institutional investors, macro traders, researchers and risk teams can use structured event data to detect market-moving developments earlier, interpret narrative shifts across macro and commodities markets, and turn fragmented news flow into actionable market and research signals. It examines how event data, contextual AI and narrative intelligence are reshaping institutional workflows … Read more